01 We investgate some of the most pertinent issues facing European firms when it comes to corporate reporting

The minefield of corporate disclosure

In the wake of the financial crisis has come a veritable avalanche of regulation, much of which is fundamentally changing how companies report on their dealings. this supplement, produced in collaboration with contributors from various financial backgrounds, explores the issues

In addition to increasing regulation, institutional and individual shareholders are putting pressure on boardrooms to manage their businesses against a much more complex and elusive set of sustainable measures taking in environmental, social and ethical dimensions. Increasingly, failure to adhere to sustainable criteria can sink a business.

As Raj Thamotheram, CEO of Preventable Surprises, notes (p10), in these circumstances it is no longer accurate to describe sustainable issues in annual reports as ‘non-financial’ when they are patently anything but. In this world of increased scrutiny, mere profits aren’t enough. The financial performance of a company is now viewed as inseparable from its wider obligations to society.

Ecological prejudice

In France, directors are hurriedly studying up on imminent new obligations under a principle known as ‘ecological prejudice’. With the support of green activists and members of the government, sustainability has become a particularly hot issue, and the principle is set to be enshrined in the civil code this year. In simple terms that means that an offending enterprise will face the full repair costs of any environmental damage. The business would also be exposed to legal action from the state, environmental authorities, local governments, environmental business groups and others. In effect, anybody with a stake in the particular case could sue the offender because of the law’s broad definition.

But what’s happening in France is also occurring to varying extents in most countries. In short, sustainable issues now go straight to the bottom line. And all this is happening alongside an economic downturn in much of mainland Europe that has triggered a wave of company collapses – about 200,000 companies right across the continent are likely to fail this year as the region struggles back from recession. Boardrooms of the survivors have had to deploy all their commercial and intellectual firepower to stay afloat.

As a result, the issue of corporate governance has never been more important. Rightly or wrongly, failures in corporate governance have been widely identified as the main contributing factors to the trouble that many financial institutions and companies have run into in the last few years. At the forefront of this debate has been the Organisation for Economic Cooperation and Development, which has embarked on a sustained campaign to highlight deficiencies in governance and to polish up boardroom skills.

Click to enlarge

Chasing tails But are we heading in the right direction? A growing number of critics argue that the plethora of regulation currently being laid out may actually work against companies’ interests – and those of the economy at large (see graph, p21) – and that the rights of shareholders and consumers have been strengthened to the point where boardrooms will end up chasing their tails.

“The last decade has seen more rapid change in the corporate governance legal regime than any period since the New Deal,” explains Professor Stephen Bainbridge, an American authority on commercial law. Although he was referring primarily to the US, the observation applies equally to Europe because of the growing transatlantic harmonisation of laws affecting boardrooms. “Virtually all of the reforms mandated after the crisis were designed to empower shareholders,” he adds.

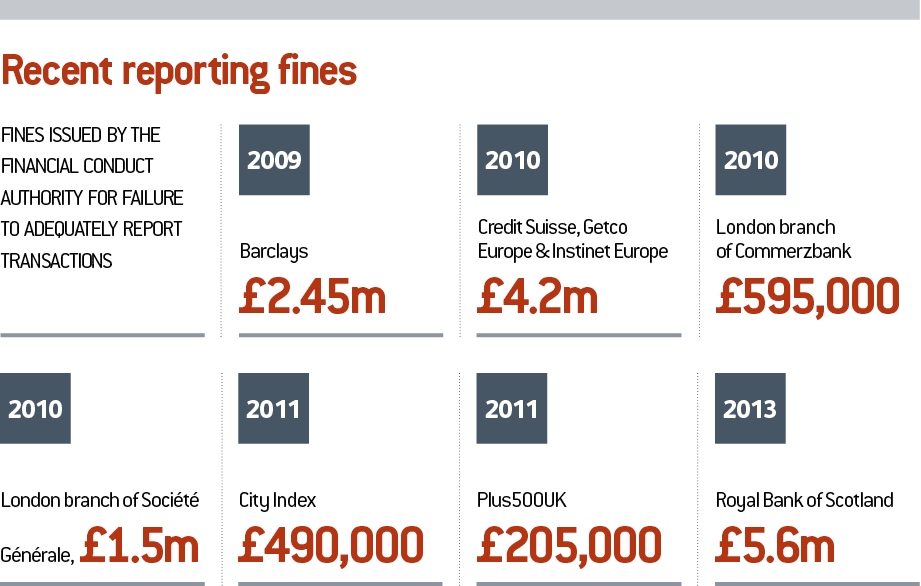

Backed by fatter budgets, regulators are becoming much more trigger-happy, handing out increasingly hefty fines for a wide range of offences. For instance, the companies in Germany’s famed Mittelstand sector – approximately 1.1 million medium-sized and generally family-owned companies – have long been able to operate in their own way as privately-owned enterprises. But now they are bearing the brunt of transparency laws that oblige them to file annual financial reports at the risk of being fined.

According to financial newspaper Handelsblatt, some 150,000 of these companies have refused to expose their profit-and-loss on a publicly accessible site, as required. Those companies footed combined penalties of $121m rather than make their affairs known to the wider world. Even Brussels, the fount of regulation, senses the danger. In a recent paper, the European Commission notes that SMEs are “disproportionately affected by regulation”. They certainly are – their costs of compliance per employee can be as much as 10 times those of larger companies.

Europe’s biggest boardrooms are also struggling. The EU’s increasingly dense thicket of aviation regulations, particularly in terms of safety, has become a bone of contention for flagship carriers such as Air France-KLM, Lufthansa, Iberia and British Airways. Operators say the paperwork is unnecessarily burdensome and often irrelevant. “We must simplify the bureaucratic nightmare that is slowly killing general aviation,” warned Jacques Callies, president of the industry body in France.

And how will directors cope with cyber attacks? Under proposed EU-wide laws designed to protect the integrity of consumer data, firms will soon have to disclose any breaches more or less immediately. A European Parliament report insists this is an important measure to provide “a coherent and robust data protection framework with strong and enforceable rights for individuals”.

Specialists in data security say this is a game changer that will place onerous obligations on boardrooms and require a fresh mindset. As John Yeo, Director at UK-based Trustwave, points out: “Businesses need to acknowledge the concept that they are the custodians of [their] customers’ data and have a duty of care to protect it.”

Easy business

Endless studies show that the most prosperous countries make it as easy as possible to launch and run a company. However, the latest ease-of-doing-business rankings from the International Financial Corporation show that much of Europe is heading in the wrong direction compared with the rest of the world, and Asia-Pacific in particular. Germany, the European leader in the rankings, stands at only 21st, while Spain lags at 52nd, Italy comes in at 65th and Greece is a lowly 72nd.

The fear of many industry bodies – and not just the financial sector – is that boardrooms are having to spend so much time responding to regulators, shareholders, non-governmental organisations and other outside entities that they won’t have the time or energy to actually grow the business.

In this supplement, World Finance investigates some of the most pertinent issues facing European firms when it comes to corporate reporting and dealing with the current wave of regulatory pressure

Nick Jeffrey of Grant Thornton explain his firm’s role in providing governance assistance, and discusses the growth of the idea of shareholder stewardship

Raj Thamotheram makes a call for greater focus on sustainability measures and integrated reporting

Pierre-Emmanuel Iseux argues that disclosure policies may have gone too far

We take a look at the importance of encouraging volatility

Matt Moscardi of MSCI ESG Research analyses the situation facing the banking industry in the wake of a number of penalties and non-disclosure settlements

World Finance looks into how financial reporting regulation could affect credit ratings

Supplementing this report, World Finance journalist Kumutha Ramanathan invited contributors Nick Jeffrey and Raj Thamotheram to elaborate on some of the points discussed here in a panel debate filmed at the London Stock Exchange studios, where they were joined by Marian Williams of the Financial Reporting Council (FRC). See the discussion on the World Finance website, YouTube channel, or simply search 'financial reporting debate'.

The future of corporate reporting

A fundamental fact of modern-day finance is that companies have multiple stakeholders, each demanding their individual interests are satisfied. Effective corporate reporting is key, writes Nick Jeffrey, Director of Public Policy at Grant Thornton

Companies spend a lot of time with customers and potential targets – the people they want to use their products in exchange for their cash. But stop and think for a second about how companies interact with their providers of finance – those investors that companies go to rarely, asking them to maintain belief in the business and the company’s management, and asking them for money in exchange for a share of ownership or a loan repayment arrangement. Do companies spend enough quality time with their providers of finance?

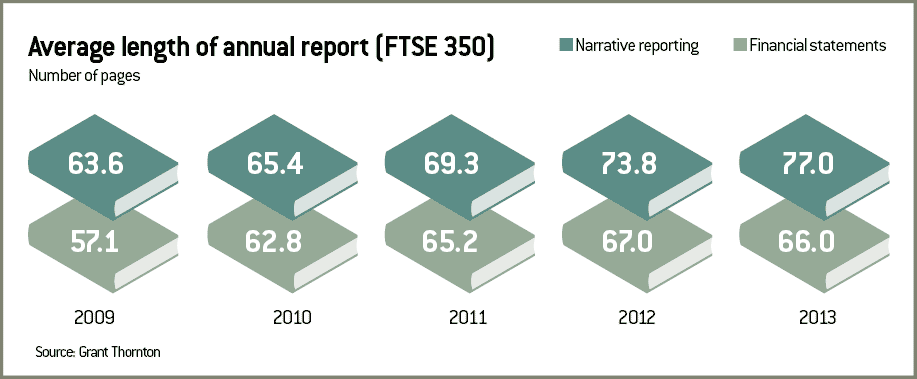

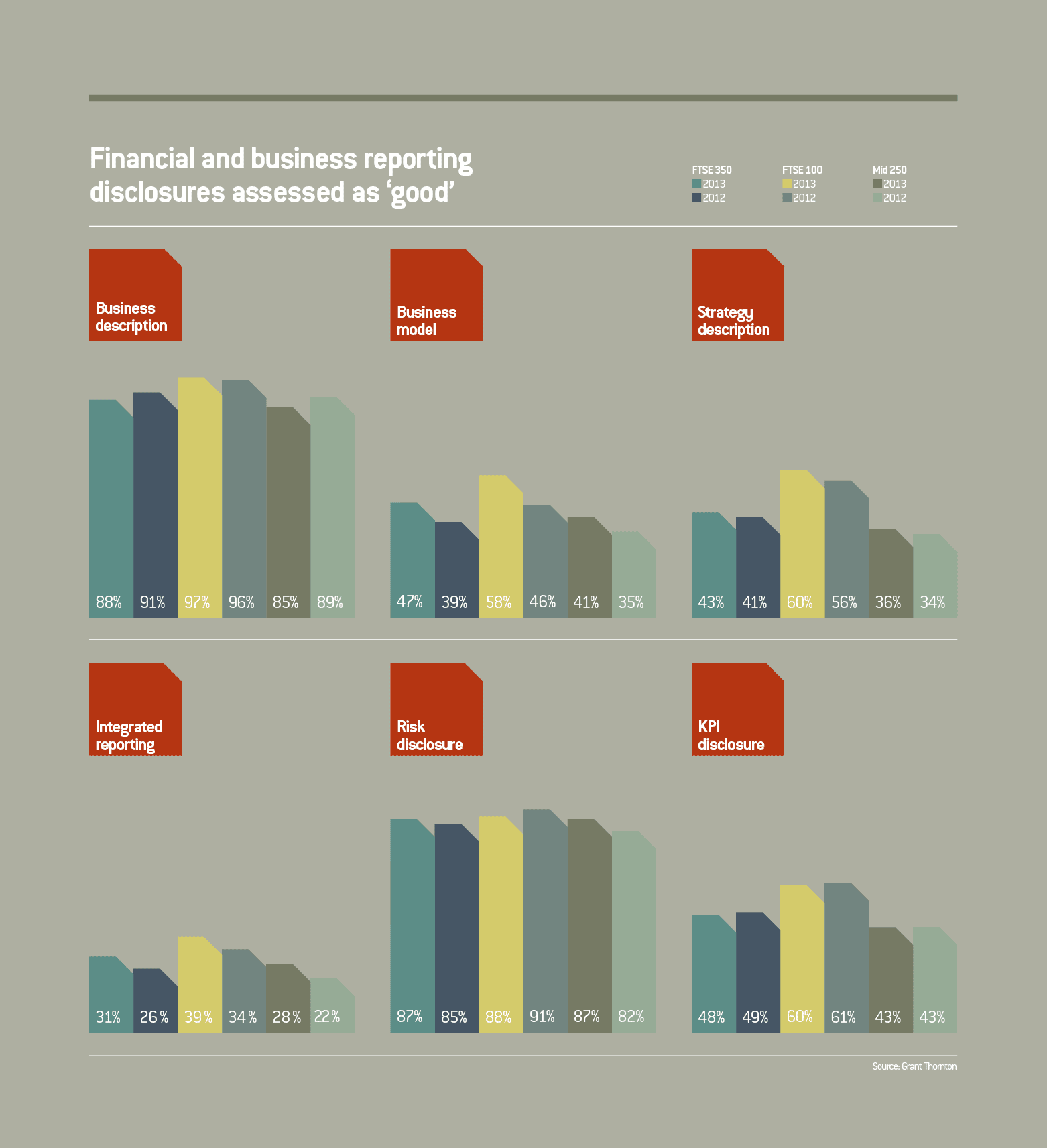

Grant Thornton research in the UK FTSE 350 market – an established benchmark of mid market to enormous global companies – shows that the average length of annual reports continues to grow – by a third over the last five years (see graphic, above right). Some annual reports are now more than 500 pages long, which is approximately 300,000 words. 500 pages of detailed information, produced once a year and made available as a block to all interested parties, is helpful to some but not to all of those interested parties.

Typically, about half that information is historical financial data. The rest is generally a corporate governance statement, a corporate and social responsibility statement, statements by the chairman and various board committees, and a description of how the company’s business segments have performed.

Effective reporting

Historical financial data is an absolute bedrock; a cornerstone; fundamental. But it is not enough, not on its own. And standalone statements about a company’s commitment to social responsibility convey the impression that societal contribution is an afterthought, rather than embedded within corporate values and the daily decision-making processes.

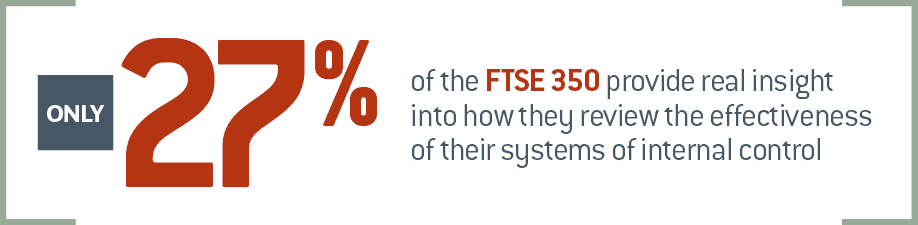

Grant Thornton research has found that large UK companies provide shareholders with limited information on risk management and internal control, while only 27 percent of the FTSE 350 provide real insight into how they review the effectiveness of their systems of internal control. This is a percentage that shows no improvement year-on-year. The report’s author, Simon Lowe, observed: “There remains a lot of room for improvement.” 84 percent of those companies surveyed failed to demonstrate the link between their business model, future plans, strategy to implement those plans, and key risks.”

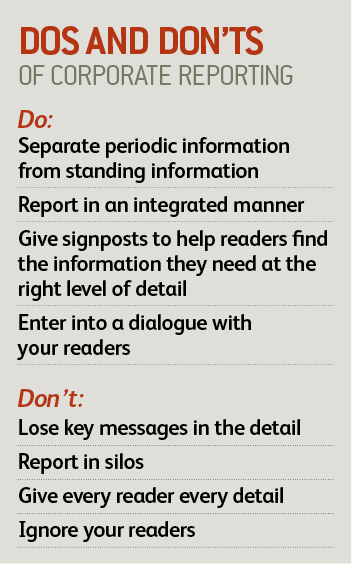

Reporting data in distinct sections of the annual report conveys the impression that the company is run in silos. It is generally undesirable for a company to be run in silos, but it is equally undesirable if bad reporting gives the inaccurate impression that it is run in silos.

Either way, the company should apply the principles of integrated reporting for internal and external reporting purposes. And thereby, internal and external decision making will be properly informed.

Click to enlarge

Quality, not quantity

Some things change from one year to the next, but many things do not. Once a company has a governance system in place it is unlikely to change significantly. The key risks to a business and its strategy will remain substantially the same unless the business environment changes or the company changes its strategy.

Information that rarely changes, known as standing information, should remain accessible for reference by those providers of finance who value it. It should also be publicly available for people who are new to a company.

However, most will not need this standing information every year, so don’t give it to them every year. Periodically report the updates, improvements, and progress. And tell others how and where to access the standing information if they need it. New improvements should be placed in the context of proven successes. Don’t allow high value or periodic information to become lost in a swamp of standing information

One size does not fit all. Providing one bank of data effectively says to your providers of finance: here is the data I am giving you, now get on with it. It is not an impression you would want to leave with your customers, so treat your providers of finance with the same respect.

Companies can and should be more helpful to their providers of finance. Companies should structure the way in which they provide information. Typically this is at three levels:

High-level key messages for all;

Mid-level information that puts some flesh on the bones and allows those readers who require it to dig a little deeper and gain greater understanding; and

Detailed data for those who want to drill right down, for example to populate their models.

Customers come to your business with specific needs, and you would strive to offer the highest quality customer service, especially if they were an important customer and if they had a specific request. Providers of finance are no different. People who want to know about your company come with different needs – both in the nature of the information they want, and the level of detail they need. Can your readers find what they want before they get frustrated? And if not, are you confident that their frustration does not taint their view of your company? The irony of damaging your valuable corporate reputation through the very channel that seeks to enhance that reputation should not be lost on any CEO.

It’s good to listen

In my experience as a customer, companies generally go out of their way to help, and generally deal with requests or complaints in a prompt and respectful manner. In my experience of corporate reporting, however, both in written and spoken forms, there is often a great deal of talking by the company, but very little in the way of listening to the needs of providers of finance. There is at times a real risk that companies and their providers of finance are talking past each other. Which is unhealthy for both the company and its investors.

The idea of shareholder stewardship is gaining traction across Europe. Broadly speaking, it is the notion that shareholders engage in dialogue with management about the issues that are important to them. If that dialogue is to be rich in content, foster mutual understanding, and ultimately help the capital markets become more efficient, then the willingness on the part of shareholders to engage must be matched by the company’s commitment to transparent and high-quality communications to form the basis of that dialogue.

Your corporate reporting is a reflection of your company. Give more thought to what you say publicly about your company, and how you say it. Show your providers of finance that you care. It is likely to improve your corporate relationships.

A new era of integrated reporting

Investors need considered financial reporting in order to make their decisions, not an endless flow of historic facts and figures. Raj Thamotheram, CEO of Preventable Surprises, explains why

The irony of the meeting couldn’t have been clearer: the world’s elite – Bill Clinton, Mark Carney, Christine Lagarde, Paul Polman and Prince Charles, to name just a few – had come together to talk about, yes, inclusive capitalism.

Actually, there has been an explosion of high-profile projects, supported by the ‘one percent’, to reform capitalism. Why? The Global Financial Crisis has clearly shaken the ‘business-as-usual’ assumption, but informed elite concern goes beyond just the banking crisis, given the growing signs of social instability and an eco-resources crunch.

As Co-Chair of the Inclusive Capitalism taskforce, McKinsey’s Managing Director, Dominic Barton, says: “There is growing concern that if the fundamental issues revealed in the crisis remain unaddressed and the system fails again, the social contract between the capitalist system and the citizenry may truly rupture, with unpredictable but severely damaging results.”

Click to enlarge

The arguments of anti-globalisation and environmental campaigners have been taken up – suitably modified of course – by some very unusual suspects. Inequality has been the number-one risk for the Davos participants for three years. And Oystein Dahle, ex-VP of Exxon Mobil, has warned that communism collapsed “because it didn’t allow prices to tell the economic truth. Capitalism will collapse because it doesn’t allow prices to show the ecological truth.” So what does this have to do with the day job of analysts and investors?

Informed decisions

Without relevant, timely and reliable information, investors are unable to make informed long-t erm investment decisions. And this is the transmission mechanism for how the legitimacy of capital markets is being undermined. Remember, markets have only one real purpose – to allocate capital efficiently. Without access to the right information, it is inevitable that money is going where it shouldn’t; economic growth is impaired; the market focus shifts to things that don’t matter in anything other than the short-term (such as total shareholder return growth and relative returns); and at worst, the market gets in the way of companies and governments investing in what society really needs. The legitimacy of democratic capitalism is ultimately at risk and the recent European elections are an early warning of how fast public sentiment can change.

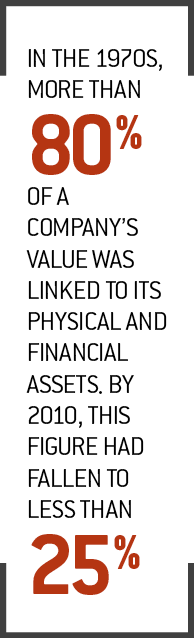

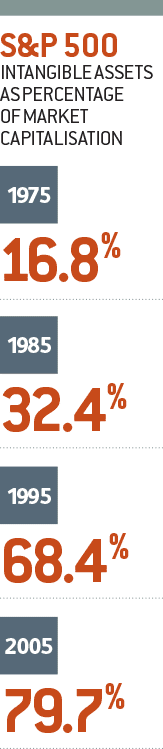

In the past, investors’ decisions have been based on historical financial statements. But such information gives an incomplete and at times dangerously misleading picture of a company’s health and future potential to create value over the longer term.

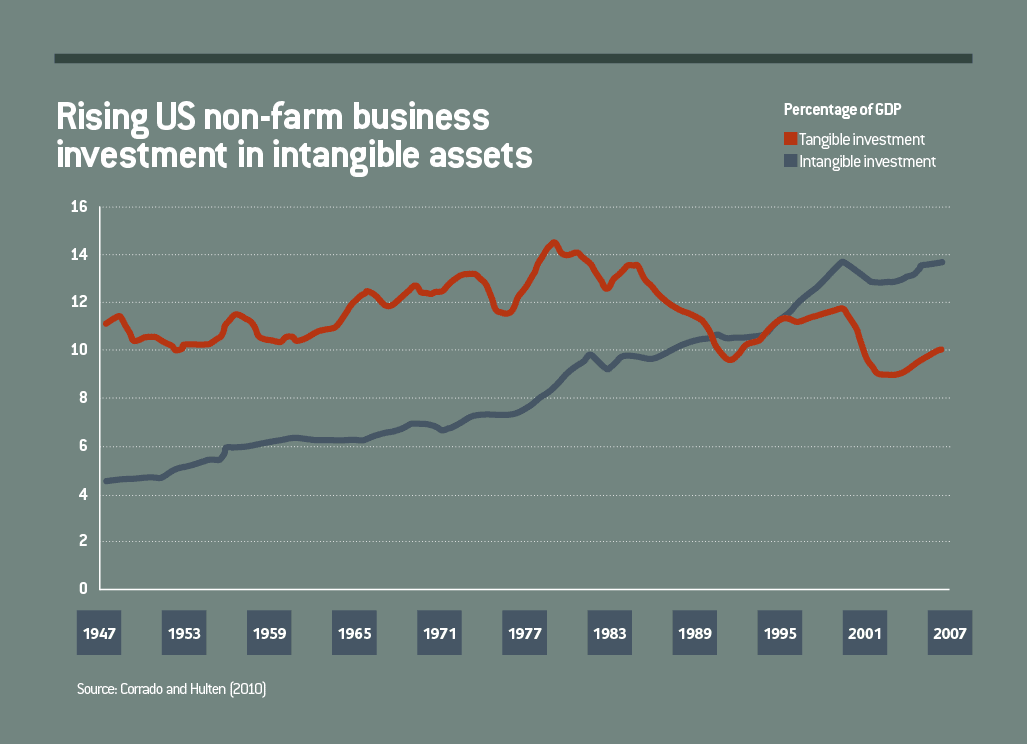

In the 1970s, more than 80 percent of a company’s value was linked to its physical and financial assets. By 2010, this figure had fallen to less than 25 percent, with ‘intangible’ assets – what are often termed environmental, social and governance (ESG) factors – playing an increasingly central role in driving market value (see graph above). These factors are often called, rather inaccurately, ‘non-financial’, when clearly they are anything but non-financial – as those who have examined ‘preventable surprises’ like Barclays, BP, Citibank, Enron, Lehman, Rentokil and WorldCom know only too well.

They include both internal intangible assets (such as innovation capacity, management structure design, human capital management and employee engagement) and external ones (such as constraints on natural resources, brand value, and social license to operate).

Investors sort of know this is important, having experienced the surprises and collapses, but today can still get away with claiming that such blow-ups are ‘exogenous risks’ when in fact the reality is that many are preventable surprises. For example, consider two high street retail companies. One has a change in management and starts to show a big drop in employee engagement and twice the staff turnover of its competitors. No loss of customer sales… yet. These feedback loops impact revenue, but with a delay. So shouldn’t a long-horizon investor want to know about these leading-versus-lagging indicators of risk to revenue and cash flow?

Comparable information

A big part of the problem is that investors don’t have ready access to comparable information about these ‘non-financial’ issues in the same way they have access to financial statement data, presented according to well-established measurement and disclosure standards, and then independently audited.

A 2014 Ernst & Young study found that two-thirds of global investors evaluate non-financial disclosures. However, only half of this group uses a structured process to make their assessments. We need a standardised way of getting this other information to investors in a user-friendly format that readily links it to data about longer-term financial performance, risk and company valuation.

Some companies have been reporting on environmental and social performance for a considerable time, but often for the benefit of stakeholders rather than investors, with too much focus on good news, photos of happy children, green flora and fauna, and so on. Similarly, there is some reporting on governance performance, but with a tendency toward box-ticking.

What investors need are reliable, measurable disclosures from which to create insights and recognise trends. The fact that so few companies disclose any decision-useful information on investment in R&D or human capital or capex should be of concern to long-horizon investors and their clients. And these disclosures need to be in accordance with global standards for global capital markets.

The good news is that it’s not an insignificant group of investors who should want this. More than 10 percent of mainstream institutional investors have signed up to the Principles of Responsible Investment (PRI), making a formal commitment to integrating ESG factors.

Moreover, there are good reporting initiatives underway. But sadly they are often regional: the Sustainability Accounting Standards Board (SASB) in the US; the European Federation of Financial Analysts Associations (EFFAS); or the EU’s new directive on ESG disclosures.

This is no way to manage global financial markets. Trying to do so repeats the same mistakes from the debate about financial reporting, where we have had so much trouble harmonising different standards. In the case of the SASB, while its intention is undoubtedly good, its standards are too disconnected from disclosures about core finance drivers such as return on invested capital (ROIC). Companies can’t really be sustainable if they are not financially viable.

Consider a company that has five years or more of net negative ROIC. Such a period of cumulative negative economic profit is clearly not a financially viable business model for long-horizon investors. Add in the known, likely or potential impacts of material ESG risk and performance factors, or a better, deeper understanding about the lack of R&D or capex investments (investing to maintain assets versus new investment in assets). Surely investors in this company would want to know about these additional dimensions of risk and performance?

There are many voluntary disclosure initiatives, but the bottom line is they haven’t delivered and, by themselves, can’t. Governments have to show they want these accounting and disclosure shifts to happen. Since government action on a global scale is unlikely any time soon, the Sustainable Stock Exchange Initiative (SSEI) could be a good interim step in coordinating disclosure requirements. The SSEI is global in reach, and engages key committed international institutions and a growing number of national exchanges to implement suitable disclosure rules.

Integrated business report

We certainly don’t need a complementary reporting system or additional reports. Rather, we need a new type of integrated business report that takes into account economic value creation, core innovation and core value creation metrics like revenue growth and ROIC as compared to the cost of capital – not to mention other ESG factors and impacts on other forms of capital (such as human, social and natural) that may be key value drivers but which never appear in financial statements. The IIRC’s December 2013 Integrated Reporting Framework is an important step in this direction, and is already being experimented with by several major corporations globally, including in the US.

The big question is: how soon will investors who say they are responsive to the true interests of clients and beneficiaries really demand the information they need, not only from the companies they invest in, but also from the capital markets and financial standards regulators?

As public scrutiny of fiduciary investors increases, we need better investment returns balanced by healthier corporate behaviour. An essential pre-requisite for this is to fix the reporting problem. This means action on two parallel tracks: fundamental financial metrics and ‘non-traditional’ risk and strategy issues. The choice is simple: inclusive capitalism, or something we really wouldn’t want to leave to the next generation.

Too much, too soon: the rise of regulation

Pierre-Emmanuel Iseux, Director of Investment Banking at Fox-Davies Capital, argues that disclosure policies may have gone too far for financial institutions, particularly when coupled with other recent regulations such as data reporting requirements

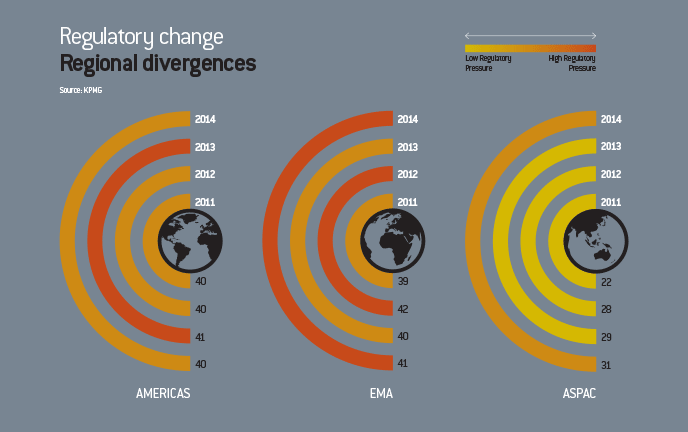

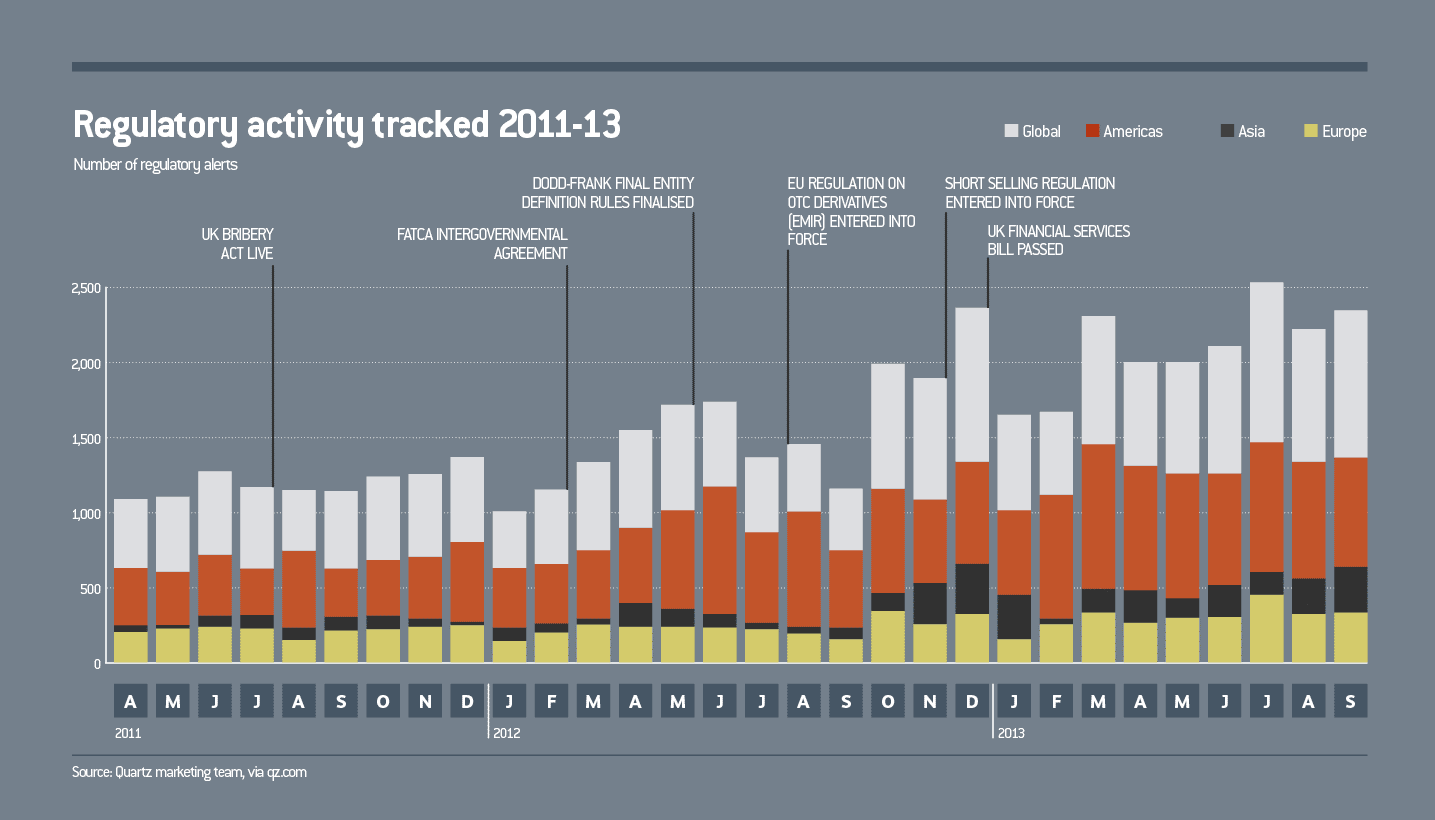

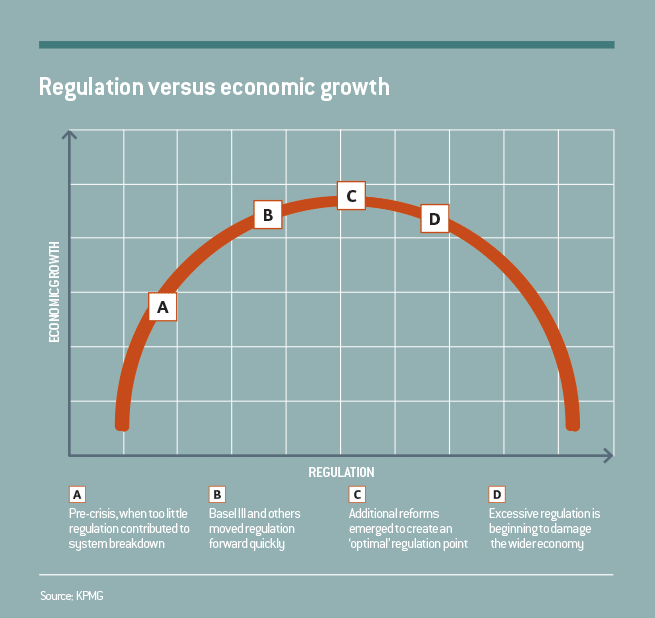

Following the financial crisis of 2008, most governments have recognised a need to prioritise stability in financial markets by imposing significant reforms. As such, European governing bodies have spent the last six years strengthening regulations and creating supervisory roles to mitigate the risk of another market fallout (see graph). Utilising the powers of the G20, an elaborate set of financial reforms will be implemented right across the EU.

Click to enlarge

How the rise of modern regulation is changing the finance industry (source: Quartz marketing team, via qz.com)

The challenge banks and other financial institutions have in complying with the plethora of new regulations is significant. Not only must the entire sector become compliant with a complex set of regulations within a comparatively short timeframe, it must also do so in an extremely difficult economic and business environment. Generally speaking, Europe is still experiencing low average growth rates, higher banking costs, lower margins, increased non-performing loans, and decreasing profitability.

There have been far too many new regulations put in place over the past few years to inspect each, but for the sake of brevity it can be useful to consider the groups affected by new and pending conventions.

Target audience

Consumers, of course, must be top of the list, as most regulations are set out to protect them. The target of increasing transparency and better disclosure policies must be regarded as paramount, particularly when inspecting payment services and retail banking.

One particular group that will be looking over its shoulder will be accountants and auditors, whose instinct and awareness must be finely tuned to new standards in respect of financial instruments. Perhaps it goes without saying that an added issue comes from working through the cross-sector ramifications of the new regulations.

Mainly though, and most immediately, financial institutions that interact with consumers through markets must – as mentioned – focus on bettering corporate governance and consider a more long-term outlook for performance metrics.

This means a direct and heavy-handed third party influence on a corporation’s financial situation, business models, operating structures, and ability and propensity for change.

Particularly looking at banking institutions, which I believe will be heaviest hit:

There will be a noteworthy impact on a company’s balance sheet, particularly in terms of liabilities and equity;

Significant impressions on a bank’s business model and ability to generate revenue and profit from operations;

Substantial bearing on a bank’s operating model efficiency, such as organisation and process, and IT infrastructure;

Impediments to a bank’s ability to change, adapt and search for a sustainable and competitive advantage.

As a matter of example, below is an observation of the cumulative impacts of some major new rules and directives likely to have a significant impact on the financial sector.

Basel III

The target of Basel III was quite clear: improve the stability of the banks through the quality and quantity of the capital required, to increase liquidity buffers, and to significantly reinforce risk management measures.

Much of the focus, however, has been placed on the impact of profitability. With common equity requirements more than tripling, it will be clear that there will be an effect on return on equity (ROE). However, the level of this impact and degree of exposure will depend on the individual operating models.

Meeting the liquidity target ratios will remain a major challenge for most banks. Increased demand for high quality liquid assets will constrain the return on these assets by adding to the pressures on banks’ profitability – especially in a period of low interest rates. In a highly competitive market, long-term deposits will be more expensive and more difficult to obtain, especially for smaller banks. Retail deposits will become less stable due to greater competition. Further, more reliance will be placed on rate-sensitive and internet funding, as switching between banks becomes quicker, easier and cheaper. The major impact here will be a shift in balance sheet planning from an asset-based approach to a liability-driven approach, and therefore reducing the probability of balance sheet expansion.

The new regulations will go far deeper than simply impacting profitability and ROE. The new requirements have been designed in such a way that they have a fundamental impact on the way banks do business. On top of that, meeting the requirements places enormous strain on an institution’s systems, liquidity contingency planning, stress tests, and liquidity key risk indicators.

A further imposition has been the conversion of certain types of debt into equity upon the occurrence of a ‘trigger event’. Put simply, some of the bank’s debt holders have to share the burden of any losses incurred by the organisation.

As such, banks must retain the amounts of possible bail-in liabilities required by new regulations. Such liabilities will be expensive for banks, because unsecured and uninsured creditors will demand a significantly higher return to reflect the removal of implicit state support or guarantee.

Banks are currently deciding whether part of the adaptation plan will include a structural shift in their operating models, changes in legal structure or sale of non-core business. In preparation, companies are developing recovery plans based on stress scenarios, with prospective actions linked to specific triggers.

Financial transaction tax

In February 2013, the European Commission published its proposals for a financial transaction tax to be imposed on a wide existing range of financial instruments, from capital markets services, money market products, derivatives, Undertakings for Collective Investment in Transferable Securities (UCITS funds) and other alternative investment funds.

Financial services providers will have to identify the affected financial instruments and review them to assess implications for strategy, distribution and pricing. According to research, and under the current proposals, the profitability of the entire European banking sector is likely to be hit significantly.

Trading volumes, liquidity and spread for these financial instruments are likely to be negatively affected. It is also expected that some lines of financial instruments may become unprofitable, while others will need to be significantly restructured to comply.

Markets in Financial Instruments Directive

The target of MiFID was to create increased competition in financial markets while harmonising different approaches to investor protection across the EU. On October 21, 2011, the European Commission issued its first proposals for an entire revision to MiFID. Since then, the proposals have evolved into a mixture of regulations for jurisdictions and directives subject to national requirements. Major implications of MiFID include:

Pre- and post-trade transparency requirements for equities and other asset classes;

Investment advisors face additional supervisory rules relating to their cross-selling and marketing practices;

Product suitability measures, including new controls of marketing processes and additional required disclosures about the financial product.

These additional regulations and directives will come at significant cost to the financial industry. For example, the operational costs of setting up the right technological infrastructures to comply with the additional data and reporting requirements alone are likely to be significant. Entire business models will be affected by MiFID – from the scope of products and services provided to wholesale, corporate and retail customers.

Prudential regulations have been designed to protect the financial services sector from potential crises – mainly because they have a knock-on effect on entire economies. Most reforms are in place to promote transparency and move disclosure higher up the list of priorities for financial establishments.

But these new European regulations and directives leave the financial sector with no other choice than to take quick corrective measures to keep solvency and liquidity ratios at acceptable levels while restoring or preserving profitability. Not only will time constraints be difficult to achieve, but also the necessary additional costs will significantly weigh on the profitability of many organisations. To illustrate: if the additional regulatory costs were fully transferred to consumers, a re-pricing of loans by over 200 basis points would be needed to reach the regulatory targets in time.

It appears that new regulations aiming to reduce risks – while simultaneously having a positive effect on the stability of the European financial services sector – will have adverse impacts on profitability and access to capital, with possible negative consequences for employment in the sector.

Moreover, with the large cumulative impacts of the different regulations and other directives, it is clear that these prudential measures will not only have a direct economic, financial and social effect, but also act as a significant deterrent to every bank’s capacity for change in order to adapt, develop and survive.

Mandate of the G20’s Financial Stability Board

Assess vulnerabilities affecting the global financial system and identify and review on a timely and ongoing basis within a macroprudential perspective, the regulatory, supervisory and related actions needed to address them, and their outcomes

Promote coordination and information exchange among authorities responsible for financial stability

Monitor and advise on market developments and their implications for regulatory policy

Advise on and monitor best practice in meeting regulatory standards

Undertake joint strategic reviews of and coordinate the policy development work of the international standard setting bodies to ensure their work is timely, coordinated, focused on priorities and addressing gaps

Set guidelines for and support the establishment of supervisory colleges

Support contingency planning for cross-border crisis management, particularly with respect to systemically important firms

Collaborate with the International Monetary Fund to conduct early warning exercises

Promote member jurisdictions’ implementation of agreed commitments, standards and policy recommendations through monitoring of implementation, peer review and disclosure

Undertake any other tasks agreed by its members in the course of its activities and within the framework of this charter

Driving growth through market volatility

Regulations should be under review continuously, but hitting market makers with so many changes in such a short period of time may prove costly

As outlined by Nick Jeffrey and the other contributors in this report, the trend in Europe over the last few years has been a determined and direct approach by regulators to create transparency in financial markets. A major concern for those in markets is how politically charged regulations – from MiFID to Solvency II – might work to the detriment of a healthy economy. On a macro level, the belief in a perfectly efficient market has long been a thing of theoretical finance and economic studies. On a practical level, much more is at risk.

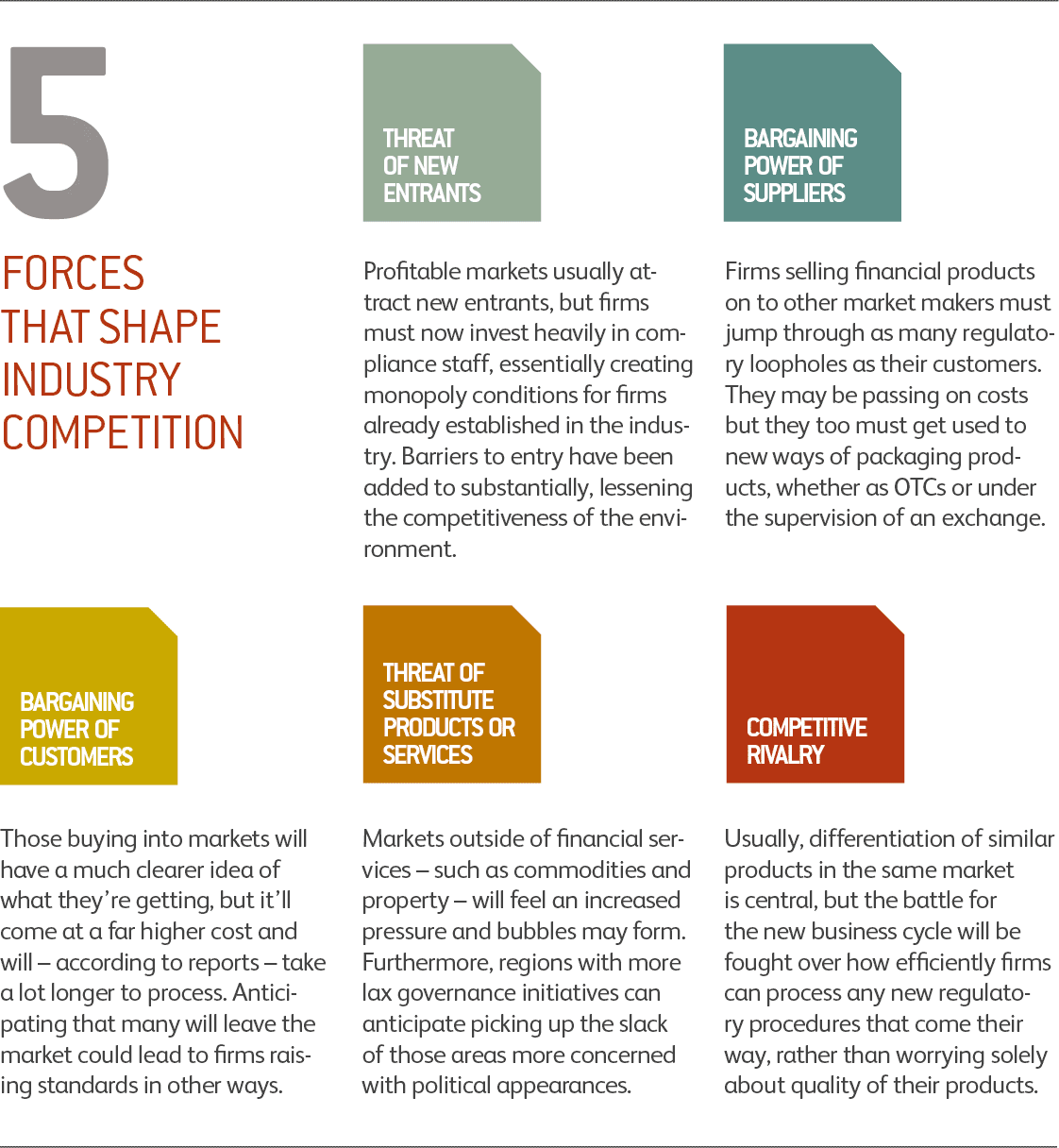

Organisations historically prefer to remain discreet about operations. With insight into what makes a company successful, it becomes all too clear why – and it’s got little to do with pushing ethical boundaries. The long term, sustainable advantage created by any successful firm is based on its core competencies. Those competencies come in the form of skills, strategy, costs and scale, resources, quality and a host of other things. But a truly successful firm defends its competitive position by maintaining a large degree of irreproducibility of those core competencies.

Performance forces

As supported by Michael Porter in his now roundly accepted five forces model (see graphic), the specific competencies that lead to greater performance must be unique to the firm in defence of a number of constant threats. Crucially, if competencies are easily reproduced, others will be able to replicate them, and the firm will suffer in many ways. Quickly looking through the five forces shows that while some stakeholders may be better satisfied with greater transparency in financial and governance documents, shareholders and others may not.

And, of course, the great fear among politicians is that markets will nosedive again some time in the future. But as economists of a growing number have started to point out, economic and market performance on a regional and global scale are cyclical. Bubbles, booms and busts are part of the foundations upon which modern economic models are based. There’s no avoiding any of them over the long term. So while governments attempt to fend off the inevitable bust, it may be more of a worthwhile cause to focus financial regulation towards what to do when busts come – and how to get out of them quicker.

The key to that – and to getting out of the current mess – is in encouraging volatility. By imposing more regulations and smoothing out market imperfections, regulators are creating less opportunity for arbitrage by decreasing margins and movements from equilibrium prices.

While attempting to eradicate lows, regulators have overlooked the fact that volatility produces returns and generates market growth.

On the demand side of finance markets, wealth managers and investors have observed an upsurge in transaction prices, creating a boundary that has stifled market opportunities.

The detrimental behaviour of many finance houses pre-crisis is something that, of course, requires inspection and review, and systems must be changed. But the problem with the current solution lies in the very fact that it spills into the systematic – rather than limiting itself to non-systematic elements.

Regulation: new costs, new approaches

Matt Moscardi, Senior Analyst and Head of Financial Sector Research at MSCI ESG Research, discusses the vital importance of reacting to regulation sensibly

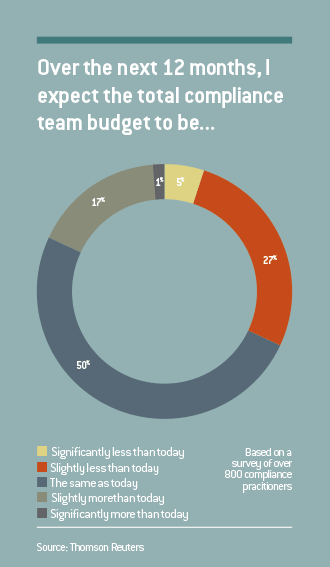

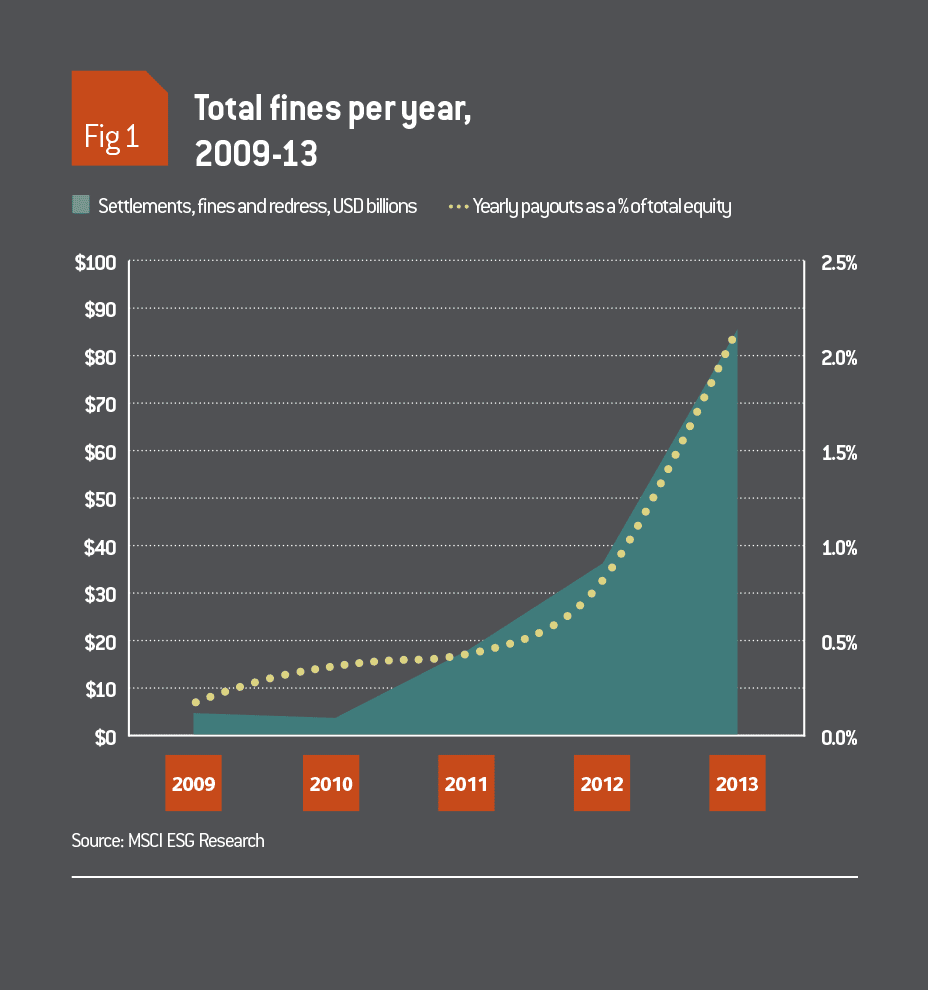

While greater rule certainty has allowed the global banking sector to move from planning to the implementation of compliance controls, reserving against regulatory enforcement costs has continued to be a challenge for these companies. Since the financial crisis, large multinational financial institutions have been fined, settled, or paid redress amounting to more than $166bn, with inflation in legal costs at nearly 12 percent per year when taken as a percentage of total equity.

Click to enlarge

In 2013 alone, the average payout costs of major banks averaged 2.25 percent of total equity (see Fig. 1) – and yet, reserves continue to be underestimated and readjusted, a process that comes at a cost to shareholders, which was highlighted in MSCI ESG Research’s 2014 Banks Industry Report. However, there are clear patterns to the regulations that are emerging, and clear correlations between certain bank profiles and stronger enforcement against controversial or illegal activities. Using our databases of major payouts since 2009 and controversial business activity, we estimated what banks should expect from regulators at home and abroad over the next year.

Who is regulating whom?

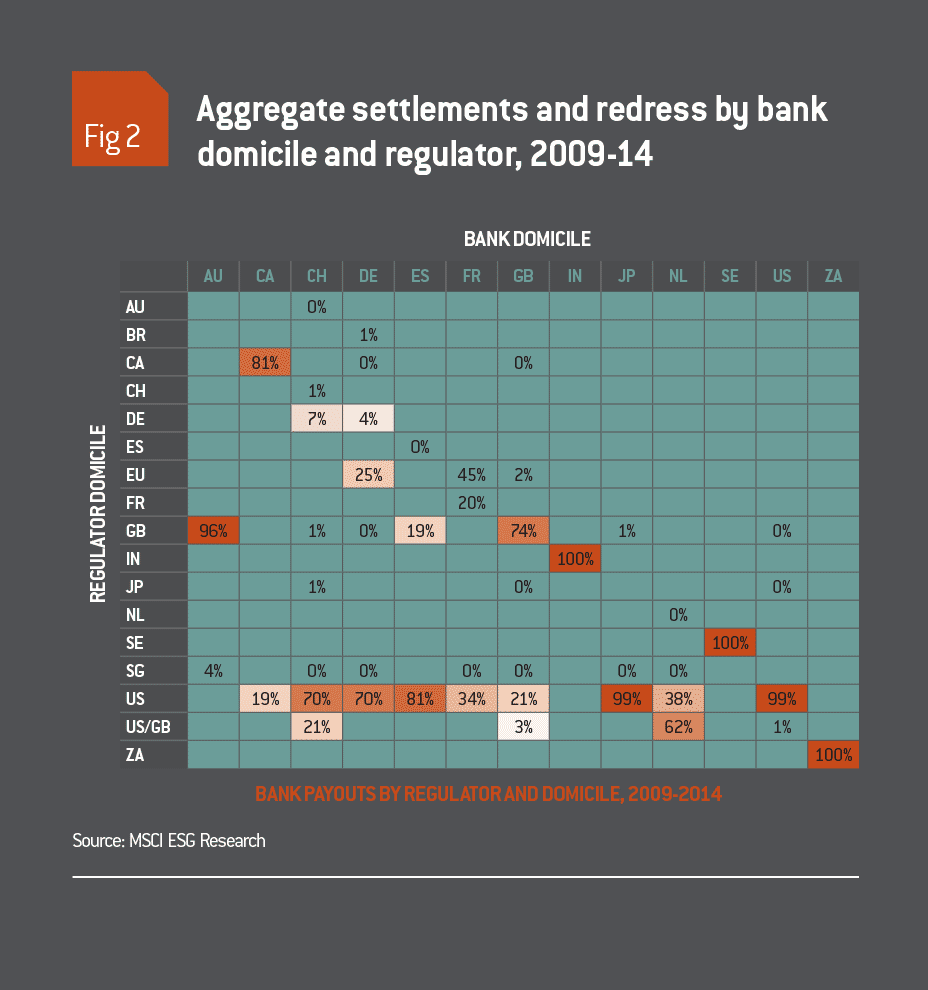

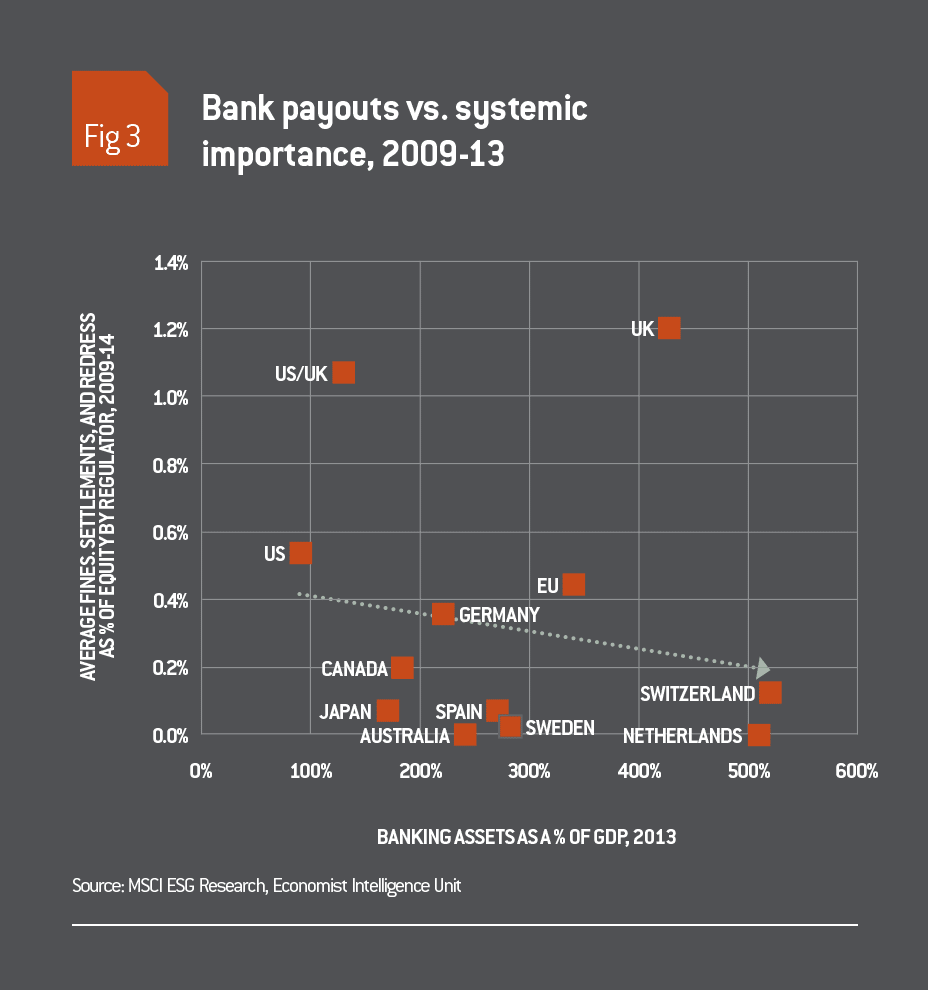

Any discourse of regulators would be remiss without pointing out exactly who is regulating whom. Fig. 2 highlights the cross-section between regulators and banks – the US accounts for at least 20 percent of payouts in almost every bank domicile in our data since 2008. When we reviewed payouts as a function of total equity, the UK stood out – particularly when juxtaposed to the size of the banking sector (see Fig. 3). We noted a trend that has so far confirmed the concept of ‘too big to jail’ – in the last five years, with the exception of the UK regulators, the larger the local economy’s reliance on the banking sector, the less willing regulators are to deal significant regulatory enforcement penalties.

In 2012, HSBC settled with US and UK regulators for more than $1.9bn for knowingly processing transactions for Mexican drug cartels. Attorney General Eric Holder explained the decision not to indict the firm in a judicial inquiry, saying: “I am concerned that the size of some of these institutions becomes so large that it does become difficult for us to prosecute them when we are hit with indications that if you do prosecute, if you do bring a criminal charge, it will have a negative impact on the national economy, perhaps even the world economy.”

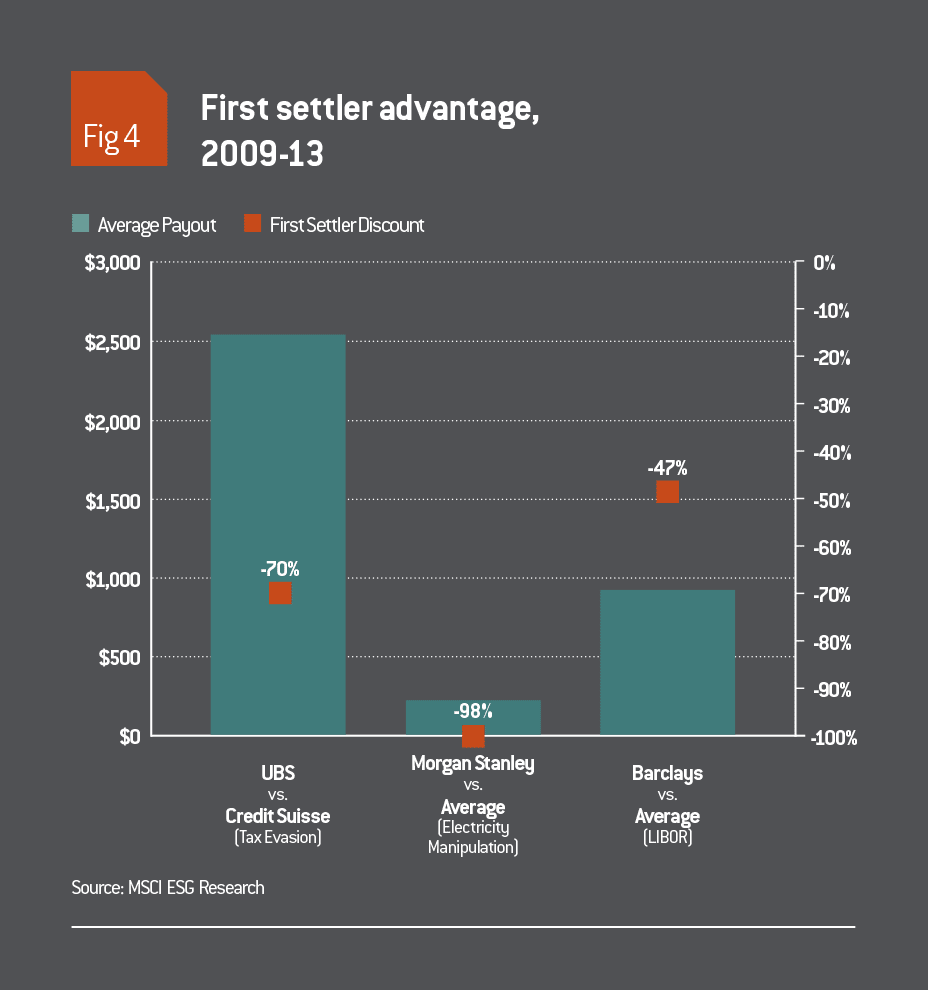

Even as US regulators seek stronger market signals by pushing Credit Suisse to admit criminal responsibility for aiding tax evasion, the ultimate penalty of disallowing market access has been totally off the table for regulators. Instead, the focus appears to be on increasing settlement costs through two distinct means of extraction: thematic, wide-net investigations giving a ‘first settler advantage’ as a metaphorical carrot, and idiosyncratic, aggressive investigations of all controversial activity within a single bank as a metaphorical stick.

Of carrots and sticks

Banks have increasingly found themselves under investigation for collusive behavior, with headlines around LIBOR, EURIBOR, Yen LIBOR, SIBOR, forex, and commodity market manipulations. The primary leverage point to entice settlements on these issues has been the ‘first settler’ advantage: limiting costs through early cooperation. This worked to Barclays’ advantage from a cost standpoint for LIBOR, as the firm paid 50 percent less than the average LIBOR settlement to date (see Fig. 4).

The same has been true of electricity market manipulation in the US – the average settlement ranks at $240m, but Morgan Stanley settled a full year earlier at two percent of the going average rate.

Click to enlarge

UBS already received a measure of immunity from the EU, avoiding costs of settling with EU regulators for ongoing forex investigations. There is some intuitive sense to this approach (similar to early plea bargains in other criminal matters), as regulators are aggressively pursuing and charging more to banks that continue to resist investigation. Ironically, the final payouts for these wide-ranging and potentially systemically destructive activities have actually been one third as much as when regulators choose to make an example in a full, post JPMorgan-style scrutiny.

Click to enlarge

Selective use of this ‘stick’ method of bank policing has usually been triggered by a controversial event which escalates quickly into a broader firm-wide investigation into all business activity. The 'London Whale' case triggered a vast exploration of other controversial activity at JPMorgan, with hiring practices in China, commodities pricing, unsettled legacy lending issues, and potentially forex manipulation all under ongoing investigation on top of the $37bn the firm has already paid in the last four years. In these cases, MSCI ESG Research has profiled banks by historical patterns of controversial activity, captured in our controversy database, against historical patterns of payouts, to see which firms have been ‘under enforced’. The results allow us to estimate a trend algorithm to profile what future fines could look like given ongoing controversies. A number of banks fit the profile of ‘under enforced’, having paid less than their level of controversy might suggest – these include HSBC and Citigroup.

Click to enlarge

The biggest gap by far belonged to Citigroup, with $12-17bn 'outstanding’, equal to as much as 10 percent of average total equity in the last three years when including estimates for forex settlements. Ultimately, for each of the companies highlighted, a single major event (like Citi’s Banamex scandal) could be the tipping point for a JPMorgan-style undressing, with payouts amassing into the tens of billions quickly.

Click to enlarge

BNP is currently facing perhaps its first major fine from US regulators, with estimates as high as $10bn. Determining how much of a legal buffer has been set aside by the banks to cover these costs is anecdotal at best; however, there is strong evidencethat the banks have historically underestimated the legal costs they face.

Examples include JPMorgan’s $23bn legal reserve set aside following the Bear Stearns acquisition, which has fallen well short of the more than $34bn paid since 2009 on various issues. Also, by Goldman Sachs’ CFO’s own admission, the firm may be under-provisioned by nearly $4bn, and Swiss regulators were requesting that Credit Suisse increase its provisions prior to settling with the US Department of Justice.

Ultimately, guessing regulatory approaches can be as much art as science, but the banks themselves have historically proven to both underestimate and misunderstand the potential costs involved. As regulators grow increasingly efficient at wielding carrots and sticks to reign in behavior, banks may need to consider how to anticipate regulatory zeal rather than react to it.

Ratings and reporting

For many firms, landing a positive credit rating can mean the difference between success and failure. As the international regulatory environment continues to shift towards standardisation, new rules on how a firm’s financials are reported may drastically affect ratings across Europe

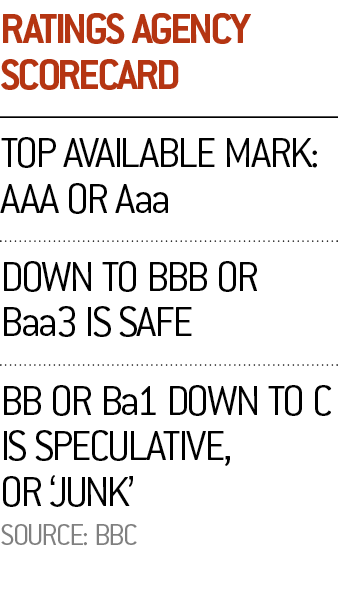

Maintaining a satisfactory credit rating is essential to the survival of most corporations. Because a vast majority of firms and investors lack the resources to conduct stringent background checks and forecasts on the long-term health of organisations and their financial products, potential stakeholders rely heavily on the rating services of industry giants like Standard & Poor’s, Fitch, and Moody’s.

The analysts at these agencies provide entities with standardised credit ratings based on different readings of their financial statements. Agencies follow quantitative models that particularly scrutinise a company’s annual statements, focusing on funding arrangements and financial instruments, debt structure and strategic attitude towards risk. From there, statisticians are able to assess a firm’s cashflow resilience and short-term risk profiles.

Other fundamental factors such as industrial competition, economic downturns and radical shifts in management, supply agencies with the means to rate an entity’s long-term market strength. Surviving this gauntlet of analysis can be arduous; however, the benefits are wide serving. The relatively standardised methodologies used by ratings agencies means opinions are recognised globally, giving firms broader access to international capital. It also creates added flexibility for issuing financial products and the potential to sell larger offerings at longer maturities. In short, credit rating agencies are instrumental in broadcasting a company’s reputation.

With that in mind, market makers that are given such ratings would do well to take into consideration the full implications of Europe’s evolving regulatory standards on financial reporting, and whether they will alter how rating agencies define a healthy corporate entity.

Reporting financials

When taking into consideration a firm’s financial position, agencies tend to start by looking at the way in which corporate funding is supplied and structured. Yet due to a number of amendments on international regulation that were voted in by the EU last year, analysts may now face complications in assessing a company’s funding arrangements. For example, both UK GAAP and IFRS (International Financial Reporting Standards) regulation now dictate that loans must be initially reported at fair value, even though that value may not match the actual amounts that are being loaned within a group of firms.

Last year, the EU voted in multiple amendments to IFRS 10 and 11, which control the ways that companies report annual joint statements. These regulations dictate whether an entity is reported as a large investment or a subsidiary.

At the start of 2014, the EU implemented a similar amendment to IFRS 11 that prevents firms from partially consolidating the reporting of some joint ventures. Although the accounting process remains largely unchanged, the adjustment will affect a firm’s balance sheet in that various assets and liabilities must be collapsed into a single-line item.

Instrumental products

European firms are now subject to far more scrutiny regarding the issuing of new financial instruments. Under IAS 32, or its UK GAAP equivalent, FRS 26, some options issued that would normally be considered equity may now be accounted for as derivatives. Because those derivatives will inevitably be considered a liability, this could lead to volatility in assessing a company’s financial position.

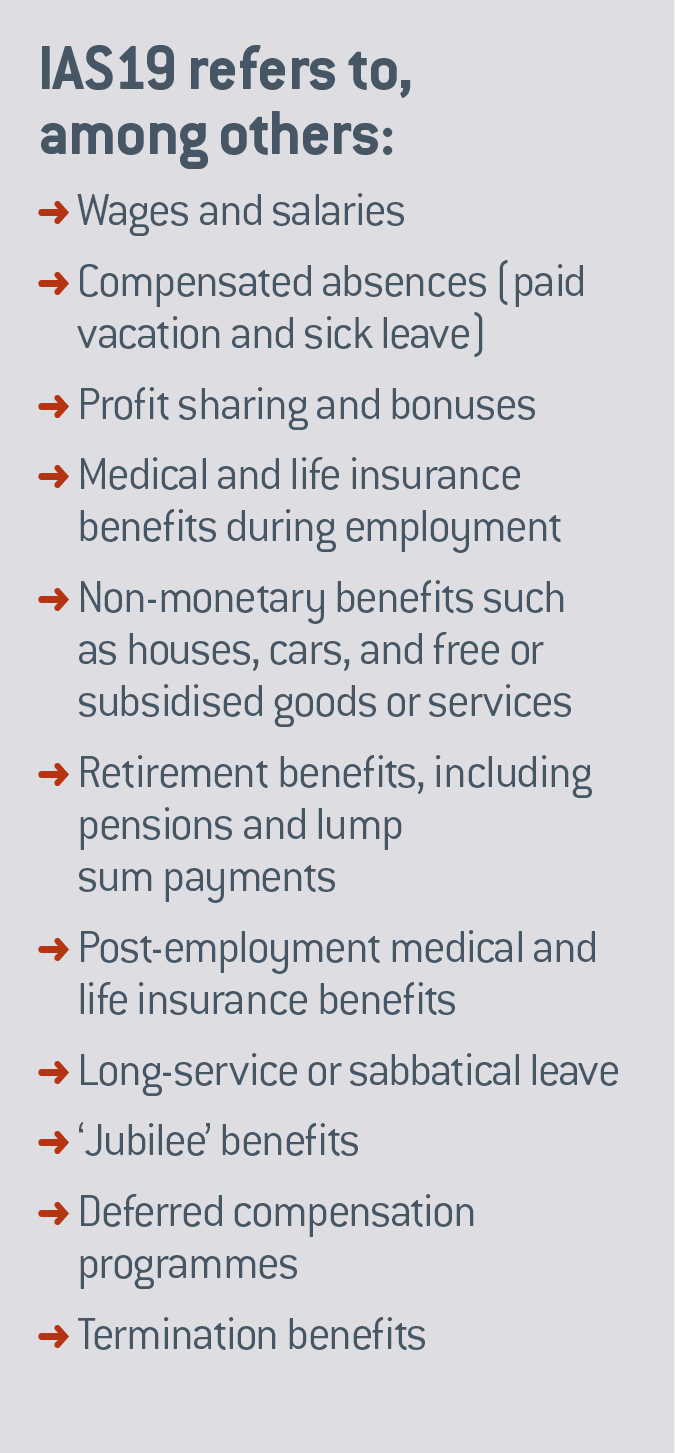

Non-derivatives aren’t immune to scrutiny, either. An EU-specific amendment to IAS 19 will alter a firm’s perceived financial performance, as it has banned the practice of so-called ‘corridor reporting’, which used to see actuarial gains or losses added gradually to income statements. Now, they will be added instantly. A ratings agency will need to take that into consideration when looking at a firm’s comprehensive income.

Risky business

Credit ratings must assess a firm’s attitude towards risk (and how that attitude has impacted its financials) as well as the way in which its financial instruments may be creating profit volatility.

IFRS regulation now dictates that all interest rate swaps must be classed as derivatives – with all changes immediately recognised through the profit and loss account. Even if a firm were to exit such an agreement before its maturity, those updates could drastically affect both its bottom line and its ability to borrow in the future.

Likewise, changes to the UK GAAP’s FRS 102 in 2015 are set to alter the way large firms disclose the value of such derivatives. Even if a given instrument isn’t recognised within financial statements, companies are now obligated to disclose its fair value. Shared risk agreements involving multiple currencies are already being hit by such changes.

Gains and losses

The last two years have seen a plethora of legislation coming into effect that more rigidly defines how those debt obligations are assessed. One of the most substantial changes has been to pension scheme obligations. Changes to the IAS 19 rules on employee benefits, for example, may impact upon the ways in which a firm presents the net interest cost of its pension obligations.

The net interest charged in income statements under the amended IAS 19 is bound to have an impact on profit and loss. Also, if a firm has previously deferred the recognition of actual gains or losses, this new immediate recognition may impact that company’s net defined benefit asset.

Other regulatory changes look at how debt is modified. IAS 39 contains guidance on whether alterations of debt obligations are substantial. If they are proven to be substantial, European regulation requires all fees to be expensed. Immaterial modifications still don’t require an immediate recognition of losses or gains.

Thanks to last year’s changes to IFRIC 19, the same can be said for the treatment of equity instruments that are issued in return for an extinguishment of debt. Now, any gain or loss surfacing from the difference between the amount of debt extinguished and the fair value of equity will be counted in a firm’s balance sheet.

World Finance speaks to a panel of experts – including Nick Jeffrey, Marian Williams and Raj Thamotheram – to discuss whether a harmonised approach to financial reporting in the EU can ever be achieved

World Finance: Now the move towards greater regulatory harmonisation has been shared by most, but do you think this is even a feasible plan?

Nick Jeffrey: Ideally we would like to see regulation harmonised across the world. Ideally. But that's a little bit of a nirvana that we're never really going to get. There's too many barriers in the way of that. You're never going to get international rules across the board.

We would like to see regulators continue to talk with each other, exchanging their views on the problems that they're facing, that investors want them to address, and to have consistency as far as possible across the world.

World Finance:Marian?

But that's a little bit of a nirvana that we're never really going to get

Marian Williams: I would completely agree with Nick: utopia isn't achievable, at least in our lifetime. I think what we do at the Financial Reporting Council, we work alongside the PRA, the FCA, obviously our counterparts both in the European Union and across the world, in terms of getting a better regulation.

As the regulator responsible for reporting and auditing in the UK, clearly our remit is quite wide. And also at the same time we set the codes and standards for our reporting in the UK. So trying to get cross-working, across all of those areas, is challenging. But it's something we seek to do.

World Finance: Okay. Raj?

Raj Thamotheram: With the best will in the world, regulators and indeed all of us, are a little bit like the generals fighting the last war. Back in the 70s something like 80 percent of a company's assets were due to the finances and the physical assets. Today that's probably down to 20 percent. The stuff that matters are the non-financial assets, and that's the key game in town. It's the human capital, it's the corporate culture, it's the governance, it's the behavioural governance, it's the R&D, it's the innovation.

The really big challenge today is how to get harmonisation of that kind of reporting. Because that's how we can look forward.

World Finance: Now looking at harmonisation, first let's talk about what needs to be disclosed in financial reports.

Let's consider the repatriation of funds. Do you think that information needs to be included in financial reports, when it's involving European companies? Marian.

Marian Williams: So essentially, in our Strategic Report - which was introduced at the beginning of this year - you would expect such challenges, or such information, to be part of what a company should disclose to its investors. Because clearly that is a part of what will help investors decide if they want to invest, or if they want to take their money from that company.

So I think if something is clearly material, then that should be disclosed in the financial statements.

World Finance:Okay, now let's talk about The Takeover Panel. For instance, you are tasked with looking out for the public's interest. Do you think that if there is a multinational takeover bid, that your organisation in any way should be involved in that process? Perhaps your remit might be too narrow in focus right now.

Marian Williams: At the moment the FRC does not have a role in takeovers as such, but we are responsible for the issuance of the Stewardship Code, which was issued two years ago, and we review it every two years. And that was really about promotion of the long-term interests of companies via the investors.

And so in a takeover situation, you've got a very delicate balance between who's investing for the long term, and who's investing for the short-term. And that's quite a challenge to understand how the Stewardship Codeshould apply.

World Finance: Nick, what do you think of the Stewardship Code?

Nick Jeffrey: I think the Stewardship Code came around as a reflection that companies and their owners were not talking together. In some ways they were talking past each other.

That in itself was a reflection that periodically a company would produce five or six hundred pages, as you were referring to. There'd be this whole raft of information appear, and investors were saying, 'What am I supposed to do with this?'

The Strategic Report that Marian was referring to, I'm a strong supporter of that. What that's intended to do is to kind of stratify the information, to give everybody the same amount of information if they want it, but to direct different users of financial reports and annual reports as Raj was referring to, to a different degree of granularity. Depending on what they want and what they need.

World Finance: In its current form then, do you think it's taking in all of those financial and non-financial factors that you've written about extensively, Raj?

Raj Thamotheram: The intent is absolutely right, and the encouragement from the FRC and government to greater stewardship is absolutely the way to go, but I think there's a little bit more box-ticking than substance at the moment, today. So if you look just at the issue of mergers and acquisitions, what we see is very low transparency on the part of investors on the reporting of how they actually deal with it.

I looked at four investors who are at the top of the field, and actually to get the data of how they were voting took my researcher the better part of one whole day to be able to compare just those four investors.

What we found was that actually, the vote against mergers and acquisitions went from 0.5 percent to 50 percent. There is some reason for this huge difference. And I think that actually part of it is that the system isn't working in terms of shining light on the key factors that investors should consider.

World Finance: Marian, will the system work better now that we have the ISB as well as the FASB working towards convergence in standards?

Marian Williams: The recent revenue recognition and standard that was issued by FASB and IASB was around getting one standard that could be implemented globally, which looks at reporting of how revenue should be reported.

I think that's a very positive move, and we feel there's something that we've worked closely with the IASB on all their projects, this one included.

So getting a standard that can allow consistency, comparability across the world, is very positive. However this has only really just been introduced, so you know, it's probably too early to tell whether we can raise the flag of success, if you like.

World Finance: But the sheer fact that we have these convergent standards demonstrates that at the international level there is coordination that's happening. Do we even need the government to be involved in financial regulation?

Nick Jeffrey: We definitely need the likes of the FRC! We definitely need audit regulators. And that was brought around at a time in the history of financial and corporate reporting when investor confidence had taken a knock.

Since the FRC and others have been cooperating at the international level, that has reinforced investor confidence in financial information. We're very close, in the next maybe five years, to approaching the point of diminishing returns.

The point that Raj is making about wider information about a business is not just the numbers, but wider information about intangibles. Think about Grant Thornton's business: our two main assets are our brand and our people.

World Finance:Raj? Do you think that we can trust companies to self-regulate?

Raj Thamotheram: You know, the thing is you can trust most people to do the right thing, but you can't trust the people who can't be trusted! And that's where the role of the regulator is important, to make sure that there is a policing mechanism.

I think that Ronald Reagan said "Trust but verify". We need that backstop in order for the voluntary system to work well. The bit that it's not working well on – and this is the challenge looking forward – is that the things that are really important to assess a company going forward - the Capex, the return on invested capital, the human capital, the staff engagement - these things are currently very badly reported. This is why we need government intervention, to just turn up the dial and make sure that we start to deliver on what we need to be delivering.

World Finance: Okay, speaking - oh, did you want to add a point?

Marian Williams: Yes, if I can just disagree on that point. I agree on the point about giving more information where it's relevant. I think the word relevance is really important to emphasise.

Human capital for instance, at the Financial Reporting Council, really wouldn't make very interesting reading, but it may do at another organisation. So I think it's really for... in my view and our view, it would be very difficult to police non-financial reporting.

However, I think what companies should be doing is liaising with their investors as to what is relevant. If it's British Airways and its carbon emissions, or hotels and its occupancy, then that's probably - it will stick more if investors really want it.

World Finance: Nick.

Nick Jeffrey: The Strategic Report. What that does really well, what the UK government's done really well, is it's given a framework or high level, minimum requirements, that allow companies that want or need to do this sort of reporting, in reacting to what their stakeholders want.

I think you've got to be very careful when you're talking about governments stepping in to start setting reporting requirements in the non-financial area. Because I think what we really need here is innovation. And to my mind, we haven't heard enough from investors and other stakeholders about why human capital is so important to them.

What I think is really exciting is the Sustainable Stock Exchange Initiative, which potentially allows many stock exchanges to move in the right direction

Marian Williams: Well we liaise with NGOs on what is important to them. And I think we have listened to them, and the value us listening to them. But I agree with Nick in terms of, it needs to be relevant. It should sit possibly in the Strategic Report, but if companies want to give more information because their investors want it, it should probably sit on their website.

So there is opportunity for companies to give more, but it may not sit on the annual report.

World Finance: I had a chance to speak with a small firm that was fined for falling under national accounting standards. Here's what they had to say about the current state of financial regulation in the UK.

"The number of high profile cases coming to light is not resulting in the level of sanction that the public might expect. This is partly because big firms have deep pockets, and audit work requires judgement to be exercised by human beings."

FRC, let me first pose a question to you. How do you expect these various groups to be able to keep up with the ever-changing nature of financial regulation?

Marian Williams: I think it is more challenging clearly for the smaller firms to keep up with financial regulation. But if you're in the business of giving accounting, or being an audit firm, there are some requirements that you must comply with in order to meet those standards. And the FRC's role is to make sure that they are behaving appropriately.

Just in terms of the cases, and I suppose specifically the larger firms, at the moment we're looking at about 20 investigations. Of those 20, about half of them are in reference to larger firms. You've probably heard most recently of the Rover case, which, although it's subject to appeal, the tribunal came up with the figure of £14m against Deloitte.

So the land has probably changed here. I think we're looking through our processes to make them more efficient, post-reform.

World Finance:Nick.

Nick Jeffrey: I think the complexity issue, I'm afraid I'm not terribly impressed by that argument. If that's the field we're playing in, you've got to deal with that issue. And you've got to be prepared, if you want to work for large corporates, you've got to be prepared to deal with it.

World Finance:Now there are other means of policing of course. The European Parliament voted to force companies to hire new auditors at 10-24 year intervals to reduce the excessive familiarity between statutory auditors. What do you make of that, Nick? Do you think that is actually going to be achieved through this rotation process?

Nick Jeffrey: I think the environment that we're now living in, audit is no longer a job for life. And by the same token you don't give loads of other services to a big company's auditor.

The idea of changing your auditor every two or three years would be harmful to quality. But changing them periodically, I think really as a market we ought to be able to cope with that. And I think it's a good development. The package of measures that's come out of Europe is well balanced. It's not focused on one particular issue. And it reflects the investor sentiment that's been happening in the market.

They don't like lots of non-audit services going to the auditor. They don't like audit being a job for life. They want periodic challenge.

World Finance: Okay, Raj?

Raj Thamotheram: The connection which Nick made I think is terribly important. The purpose of the audit is primarily for the investors. It is a mechanism to reassure the investors that the financial accounts and the other statements are true and fair. A due process of renewal of that contract allows for the prevention of capture of interest by personal relationships and other factors. And so it's the connection with the trust that we spoke about.

We know we need to reestablish why that's so important today, I think.

World Finance: What does that do to the monopoly that maybe the big four currently have in the industry? Nick, what does that do when you have audit rotation? Does this level out the playing field?

Nick Jeffrey: There are things that the FRC and other audit regulators can do to make sure that there is a level playing field. They can make sure that where appropriate they're comparing audit firms that do similar sorts of work: they're not comparing apples with oranges.

They can publish named reports on individual firms, which the FRC has done for a while now, and that's extremely helpful for investor confidence.

When they publish those reports they can publish them at the same time. So we're not comparing one firm's recent report with another firm's old report.

There's a bit that the regulators can do. I have to say that the FRC is probably one of the better in the world at doing these sorts of things. I think the FRC can still be better though.

Marian Williams: So just on that point, I think Nick's point is fair around... we publish the audit quality reports for each of the big four on an annual basis. In fact it was released last week. And on Grant Thornton's BDO we publish those every two years. Now we'd look to publish that annually. So I think the point is well made.

World Finance: Raj, do you think that's enough?

Raj Thamotheram: The ecosystem of players is I think the critical issue. And I think it's not just auditors who can keep companies on the true path. It's also investors.

This is where the regulatory bodies, not just the FRC, could perhaps step up. For example, let's go back to the mergers and acquisitions example again. We know that all the data suggest that something like only 13 percent or 17 percent of mergers and acquisitions deliver the value that they're stated to deliver.

Today there is no requirement for investors to report on why they voted in the way they did. Now the FRC could in fact ask investors to explain how they're tracking that reporting, what they're learning from it. This wouldn't be micro-managing, it would just be asking another aspect of the value-adding function.

Now that then creates space for the auditors to do their job better. Because there's another player in the game, having some insight. It's very hard for auditors to challenge their sort of fee-paying client on some very sensitive issues. So I think it's an ecosystem.

World Finance: Do you think that we have seen a maturation of the financial reporting community in terms of... I mean even if we look back to the 1970s where we had the Nestle babymilk scandal, which everyone is aware of. In the aftermath of that scandal, we saw many indices that came to birth, including the FTSE4Good Index, reporting on what people wanted to know in terms of those investors who were looking for that additional information as you mentioned. But how does an organisation such as the FSC, or another one, then say, 'let's look at this index versus another'? How do you measure the merits? Raj?

Raj Thamotheram: I fully agree that regulators can't micro-manage companies and tell companies what to report. But I think there are some areas where the gaps have been so consistent and so long-lasting. I can go back to human capital, for example.

Say for example we're invested in two retail companies, and a retail company changes its management and starts to lose the engagement of its staff, and starts to have a staff turnover. We know that that's a lead indicator of risk. But currently there's no requirement to report on that.

So unless investors have consistent reporting on some standards, the system won't take it into account. It's not possible for passive investors to take a little bit of data here, but if there's no data here, kind of compare it.

So I think there's a levelling that regulators need to do around material issues. And it's happening, but it's happening a little bit too slowly.

World Finance: Nick, you have an intimate understanding of course, being on the front lines of auditing accounting standards, and where your clients are willing to apply them. Corporate governance: how important really is it to them?

Nick Jeffrey: It's part of the mosaic that helps to bring the whole thing together. Just to go back on something that Raj was saying, I think we're arguing about shades of grey. I think Raj seems to be towards the end of the spectrum where he wants more impetus, because companies aren't doing what investors need now. I'm slightly the other way; I would say that it's for investors to drive their informational needs, and not to rely on governments too much.

For me, it's for investors to be more vocal about what they want to know about sales per square metre, or staff turnover. It's for them to be more vocal about the things that drive their investment decisions.

World Finance: What do you make of this criticism? Do you think that the FRC and other regulatory bodies have shouldered enough of a burden, and taken action as a result?

Marian Williams: I think the Strategic Report is a good example where companies have to give details of their principle risks, and therefore in this situation companies should be providing the information that is important for shareholders, that is relevant.

We just need to watch the amount of information. A project that launched this morning actually was our Clear and Concise project, where we're looking at what is relevant to stakeholders and investors.

I think we're all saying the same thing, I think really, is what is really relevant to investors? And two retailers, for instance, clearly if one starts giving profit per square foot, then that might make the other provide that information too. So I think if you see some leadership in that particular topic, or in that area, then you might find others follow. But I don't think really it is for the regulator in this instance, for non-financial reporting, because as I said it's a very deep ocean. I think we'd be drowning.

World Finance: I think you would get a faster reaction if you leave regulation to one side and let the market innovate. And if you let the market react to what investors are asking, or to what competitors are giving.

The challenge there is we're going to fall back again into that FASB, IASB divergence. And then we're going to have to knit this thing together.

So the trick I think is to do the learning from the last experience ahead of time, and try and create a convergence standard.

What I think is really exciting is the Sustainable Stock Exchange Initiative, which potentially allows many stock exchanges to move in the right direction.

We are definitely arguing about gradations, but for me it's not an either/or situation. Everyone needs to be in the game.

World Finance: In terms of financial reporting, where would you say you would add more information relating to how to enhance investor relationships, or pull back?

Marian Williams: I suppose I would look at the characteristics really. So I think materiality, clearly. If it's material to a user of a financial statement, that must be in. It must be relevant. But at the same time it must be concise. So you're trying to balance the two, which is really challenging.

World Finance: But when we're looking at 400, 500 pages of reporting, while the intention might be right. Do you think that the European shareholder is going to sit and read through every single page of that report? Or only focus on what's key? And should the rules and regulations as to what's being reported in the basic report, should that be changed faster?

Marian Williams: You know, your challenge is fair. And I think there's probably something to think about in innovation that Nick mentioned earlier, around how can companies get smarter with where they put their information. There may be something to think about there.

For instance we're looking at a new project on reporting in a digital world. So maybe there's something there, around how companies - not what their report is, but where they report it and how they report it.

Raj Thamotheram: I think that's where the potential of, kind of, collaborative action between regulators and investors could be really potent.

Because the great thing about investors is, by consensus, they can define a set of standards and criteria with companies on what's most material. And that being not regulated can evolve every two or three years as understanding evolves. And I think there's a real potential here, between what regulators can do, and what investors can do.

I just want to challenge this though. We keep... we used your phrase, 'non-financial'. But you know, when you look at Lehman's, or BP, or Rentokill, or Parmalat, or Avendi, or WorldCom. To call these things non-financial misses the strategic importance of them. And I think that's what we're continuing to do sometimes, to miss the strategic importance of these superfinancial, or extrafinancial - whatever we call these things!

Because the great thing about investors is, by consensus, they can define a set of standards and criteria with companies on what’s most material

Now how to capture that I think is the challenge for both regulators and investors, supported by auditors. So I think you've framed the discussion extremely well.

World Finance: But I think what we also need to consider is that there are people, companies rather, that are doing this well. You work with some of them. Can you tell me who is doing this well, who is incorporating this kind of information, if you want to use a term other than non-financial?

Raj Thamotheram: You know, a company like Unilever is well experienced - and not just for PR reasons, but over a long period of time - at integrating into all aspects of its strategic planning and its remuneration design, long-term incentives to take into account these sustainability factors.

So the current CEO came in with a desire to double his financial targets and halve his carbon footprint.

Not a trade-off either, a win-win.

That's not yet the norm, and I think that's our challenge. Because that's what society needs us to do, we need to rapidly move to greater resources efficiency, better organisational governance, behavioural governance cultures, and a more empowered and engaged workforce.

Now that examples exist, we need to move it into the norm of practice.

World Finance: Grant Thornton must work with some big names out there; is there an appetite for change similar to what Raj has been discussing?

Nick Jeffrey: We react to the pressures that are in that environment. And I think we as a profession could be smarter and stronger in advising the companies that we work with, and the investors that we work for, to help them understand what is really material to the users of their information, if I can put it like that: the information that goes out there.

Not to just put everything out there in reaction to what they think a regulator might react to. We've got to be stronger in saying to the companies that we audit, 'You don't need that bit of information, it's not material to users.' And we need to be stronger in saying to regulators when they come in and rightly challenge us on that, 'It's not material'.

World Finance: Well it sounds like the innovations really have to take place at various levels, not just at the regulatory level, but even in the way that companies perceive their role in this world and their long-term interests.

Well Nick, Marian, Raj, thank you so much for joining us today, now, have financial regulators and governments done enough in policing this industry? Tweet us your thoughts @worldfinance and remember to include #FinancialReporting.

Can your readers find what they want before they get frustrated? And if not, are you confident that their frustration does not taint their view of your company? The irony of damaging your valuable corporate reputation through the very channel that seeks to enhance that reputation should not be lost on any CEO.

Can your readers find what they want before they get frustrated? And if not, are you confident that their frustration does not taint their view of your company? The irony of damaging your valuable corporate reputation through the very channel that seeks to enhance that reputation should not be lost on any CEO.