Investment Banks

Argentina

Columbus Merchant Bank

Columbus Merchant Bank differentiates itself from its competitors through its consultative approach. The boutique investment bank, which was founded just 15 years ago by Citigroup alumni, has rapidly cultivated a reputation as the go-to partner for small and large firms seeking to restructure debt, engage in M&A or debut on the stock market. The bank has facilitated $40bn of deals since its foundation.

www.columbusmb.comGermany

Berenberg Bank

Berenberg prides itself on being one of the top advisors on European stock markets, as well as for having close relationships with institutional investors around the world. The group remains one of Europe’s leading banks, with total assets under management of $46.5bn and around 1,600 staff members. Berenberg’s investment advisory services span equities, corporate finance and financial markets.

www.berenberg.deGreece

AXIA Ventured Group

Based in Cyprus, AXIA Ventured Group combines a global vision with expert local knowledge to produce a personal and customised service for each of its clients. With additional offices in Greece, Portugal and Italy, as well as in the UK and US, AXIA Ventured Group puts its clients first in everything it does, with the intention of building long-term relationships based on mutual trust.

www.axiavg.comFrance

BNP Paribas

With operations dating back nearly two centuries, BNP Paribas is one of Europe’s most prolific investment banking institutions. Its corporate and institutional banking unit, which serves 18,000 clients across 56 countries, offers financing, treasury and advisory solutions. BNP Paribas is now doubling down on its digital transformation in order to rebrand itself as a bank of the future.

group.bnpparibasDominican Republic

Banreservas

Banreservas provides credit solutions to companies across a wide variety of sectors, including energy, tourism, infrastructure and real estate. Some of the transactions processed by the bank in 2018 included a $585m syndicated loan in which 20 financial institutions participated, and a $65m syndicated loan for the development of a hotel in the eastern region of the country.

www.banreservas.comColombia

BTG Pactual

When BTG Pactual was founded in 1983, partnership and meritocracy were the bank’s underpinning values. These persist today, with the talent, dedication and outstanding performance of its employees considered integral to its success. BTG Pactual Colombia offers advisory services on wealth planning and mergers and acquisitions to a host of prestigious commercial and municipal clients.

www.btgpactual.comChile

BTG Pactual

Originally established as a brokerage firm, BTG Pactual has grown to become Latin America’s most prestigious investment bank. The Chilean firm’s extensive CSR policies and pioneering eco-efficiency programme set it apart from its competitors, while its governance adheres to the highest international standards. BTG Pactual is also renowned for its support for local cultural projects.

www.btgpactual.comBrazil

BTG Pactual

BTG Pactual has consistently impressed the international community with its expertise across the investment banking and asset management sectors. It currently stands as the biggest investment bank in Latin America and the Caribbean, and its Brazilian arm has won a series of World Finance accolades for its superior service, initiatives and dedication to clients.

www.btgpactual.comKazakhstan

Tengri Partners Investment Banking

Tengri Partners Investment Banking specializes in capital raising and M&A advisory services, managing all phases of a deal from origination to structuring to execution. Their continued commitment to providing clients with tailor made solutions based on a deep understanding of their goals and business strategy helps elevate them above the competition.

www.tengricap.comSaudi Arabia

GIB Capital

GIB Capital, the investment banking arm of Gulf International Bank, was established in 2008 and has spent the last decade sharpening its expertise in the sector. The bank offers a range of investment banking products and services throughout Saudi Arabia and the Gulf region. With a hands-on approach, GIB Capital provides financial advisory services in asset management, equity capital markets and more.

www.gibcapital.comSwitzerland

Credit Suisse

Switzerland is internationally recognised as a safe haven for markets during turbulent times, and its banks are no exception to the rule. With a history that dates back to 1856, Credit Suisse has become one of the biggest investment banks in both the country and the world. The bank has operations in around 50 countries and employs more than 46,000 members of staff.

www.credit-suisse.comThailand

Siam Commercial Bank

As the first bank in Thailand, Siam Commercial Bank has been responsible for driving the country’s financial sector since day one. Today, it provides commercial and investment banking services through an extensive branch network. It seeks to build on this through its strategic transformation plan, which will see the bank bolster its mobile payments portfolio and incorporate machine learning into customer processes.

www.scb.co.thRussia

Sberbank CIB

Sberbank CIB, the corporate and investment banking arm of Russia’s Sberbank, serves nearly 700 corporate customers and more than 1,600 financial institutions, including major corporations, sovereign states and government bodies. The company has positioned itself as a market leader for equity and fixed-income products in Russia, and boasts one of the top-ranking analytical teams in the country.

www.sberbank-cib.ruNorway

Carnegie

As a leading Nordic investment bank, Carnegie offers an array of professional advisory services in mergers and acquisitions and equity capital market transactions, as well as corporate bonds and fixed-income instruments. Since its founding more than two centuries ago, Carnegie has focused on developing its local expertise. Today, it describes itself as the place where knowledge and capital meet.

www.carnegie.seThe Netherlands

ABN AMRO

ABN AMRO’s leading investment banking division operates in a global network across 13 countries. The group is focused on making a positive contribution to society, including accelerating the shift to a circular, sustainable economy. To further this aim, it offers a range of responsible investment products, including green bonds, social impact bonds and the ABN AMRO Social Impact Fund.

www.abnamro.nlturkey

Akbank

From face recognition and chatbots to blockchain payments and robotic process automation, Akbank is harnessing technology to improve the banking experience for its customers. These state-of-the-art solutions are supplemented by a network of 780 branches across Turkey. Through its innovative approach, Akbank aims to become the bank that drives the country into the future.

www.akbank.comNigeria

Coronation Merchant Bank

Coronation Merchant Bank is on a mission to become Africa’s premier investment bank, having ample experience across the corporate and investment banking, global trade, wealth management and securities trading sectors. The institution is famous for its innovation and strong corporate governance: it engages in various research projects, and has recently released its 2019 Nigeria Economic Outlook report.

www.coronationmb.com

Trimming the fat

Mergers and acquisitions activity at both top and middle-market level has been a boon for investment banks this year. Many are now seeking to simplify their operations in order to maximise profits and prepare for upcoming market changesIf there were ever a word to describe 2019 both politically and economically, ‘volatile’ would surely be it. With trade tensions ongoing between the world’s two largest economies, grave concerns about recession in Europe and continued uncertainty concerning Federal Reserve rate cuts, the world has certainly been kept on its toes over the past 12 months.

Theoretically, such volatility should benefit investment banks, as traders can take advantage of market swings to drive profits. While those with large trading desks have seen some benefit, an industry-wide decline in risk appetite following the 2008 crash meant the majority of institutions have come to rely more heavily on mergers and acquisitions (M&A) advisory and underwriting fees to boost their top lines.

US banks are better placed to dominate in that regard, and have captured most IPO underwriting fees in the past 12 months. Goldman Sachs saw its net underwriting revenues rise by four percent to $4.36bn in 2018, while JPMorgan retained its crown as the top earner of investment banking fees for the 10th year in a row. Europe’s institutions, meanwhile, have steadily been losing market share, with plenty forced to scale back hiring and investment while they focus on streamlining their complex internal systems. Many have also found themselves bogged down with the implementation of regulatory frameworks such as MiFID II, the EU’s new transparency directive that came into force in January 2018.

While strong M&A activity is expected to continue boosting US investment banks’ fortunes in 2019, Europe’s institutions will face issues due to slow continental growth, cumbersome operational models and local competition from US firms. All investment banks will also come up against headwinds in the form of competition from both boutique advisory firms and fintech companies, as well as industry upheaval in the lead up to the shuttering of LIBOR in 2021.

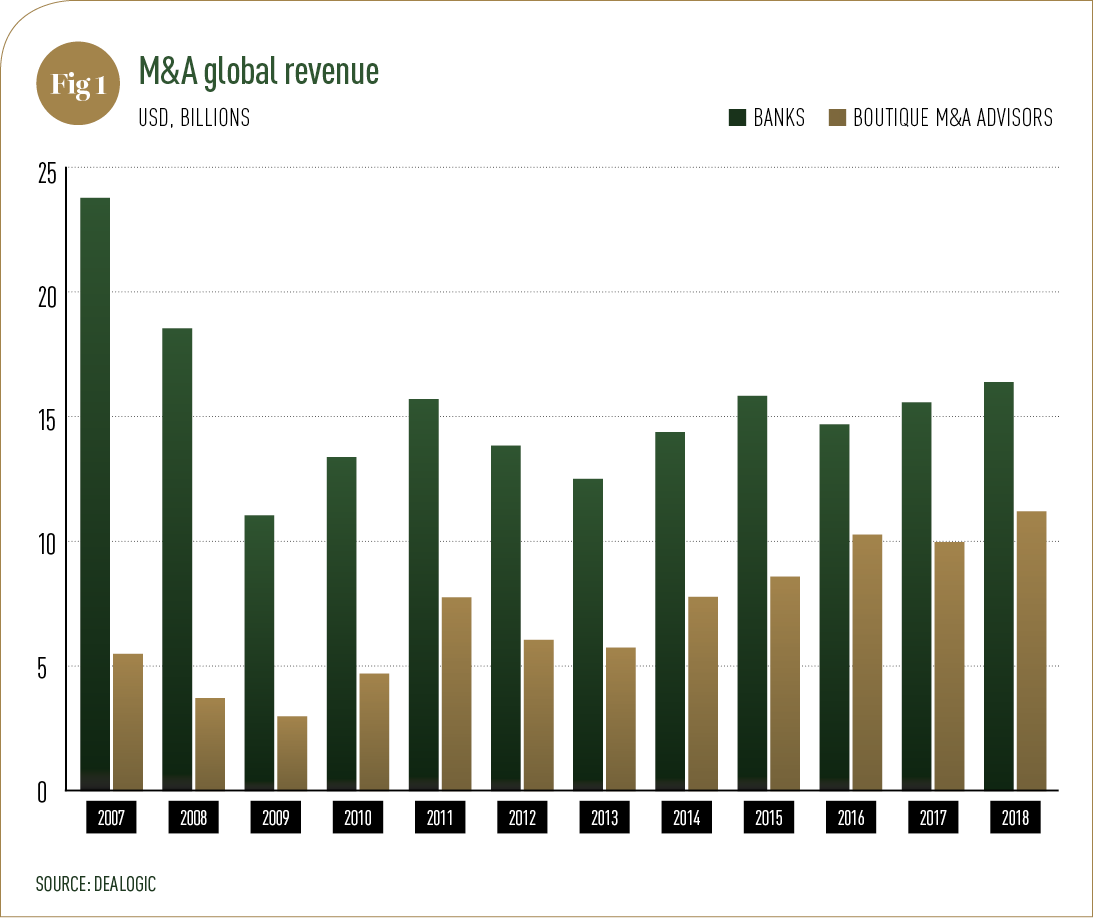

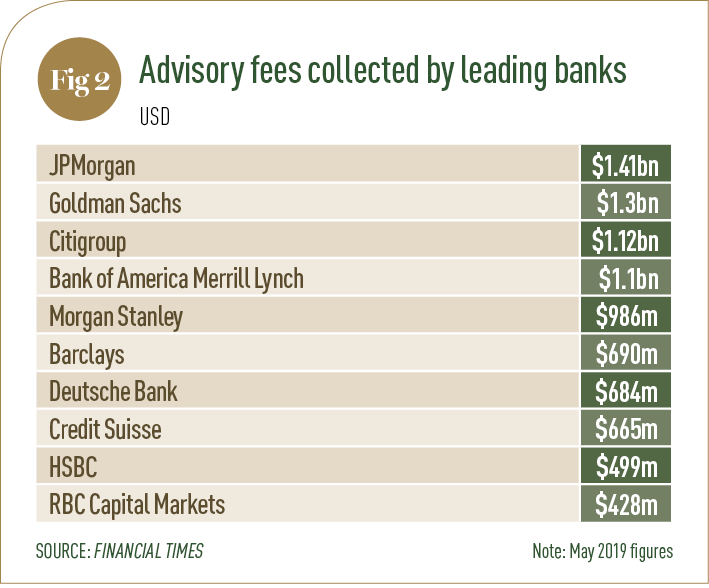

American advantage The past 12 months have seen a boom in global M&A activity, volumes of which reached $3.35trn in 2018 – the highest level since 2015 (see Fig 1). This has provided a boon for US investment banks, which have established themselves as go-to partners for companies considering M&A. As of May 2019, the leading US bank, JPMorgan, had made $1.4bn in advisory fees – more than twice the $690m taken by Barclays, the leading European institution (see Fig 2). Goldman Sachs, meanwhile, announced it is building a new 20-strong team that will focus on mid-market deals worth between $500m and $2bn: this is part of a larger strategy at the US lender to accrue 1,000 more investment banking clients over the coming months. This focus on the middle market comes as investment banks face increased pressure from boutique advisory firms, which expanded their market share to 40.9 percent in 2018, according to Dealogic – the highest percentage in history. By building out specialist teams to concentrate on smaller deal volumes, investment banks are hoping to regain some of that share, as well as to reinforce the base of their businesses in preparation for larger M&A deals. As Uber and Lyft’s 2019 IPOs demonstrated, multibillion-dollar public offerings present a high risk for both investors and underwriters, hence investment banks have recognised the need for robustness at lower levels of the businesses in order to mitigate those risks.

Technological innovation Investment banks recognise the importance of investing in new technologies in order to remain competitive, with many embracing automation in an unprecedented way. Credit Suisse’s CSLiveEx system allows the smallest trades in the US market to be carried out with no direct human involvement, while Morgan Stanley has begun exploring automated trading for small investment-grade corporate bonds as a way to handle the 10,000-odd electronic trade requests it receives every day. Goldman Sachs has taken the technology to even greater heights, building a bond-pricing engine that can handle transactions of up to $2m without a single human touch.

Automation has also proved to be an important tool for some in cutting costs and streamlining complex operational models. UBS, for example, has rolled out more than 1,000 algorithms that are able to autonomously complete back-office processes – a move it hopes will help it meet its target of cutting 22 percent of non-technology costs from its operations divisions over the next three years.

The great shake-up The most significant change to the investment banking industry is expected to arrive in 2021 with the axing of LIBOR. This key benchmark has been mired in scandal for the past decade, as numerous traders were found to have manipulated the rate for personal or institutional gain. Regulators in both the US and Europe continue to investigate banks and individuals alike for their role in the scandal – for example, at the end of April, a pension fund in Hawaii filed a claim accusing 18 investment banks of corrupting LIBOR by submitting artificially lowered figures.

As a result, the Financial Conduct Authority, which sanctions the panel of banks that set LIBOR, has said it will not continue to publish the rate beyond 2021. Some banks have begun preparing for this transition by testing new rates: the Federal Reserve Bank of New York has started publishing the Secured Overnight Funding Rate, which is currently the frontrunner in replacing LIBOR for US banks. Another possible alternative is the Euro Overnight Index Average in the EU.

The disappearance of a unified reference rate is likely to cause issues for banks operating across multiple markets and currencies by introducing a new level of complexity to institutions that are already grappling with byzantine operational systems. It is imperative, therefore, that investment banks take action in the next two years to simplify internal processes and ensure they are fully compliant with all existing regulations. By reducing operational cost burdens, they will also be able to maximise profits from the burgeoning M&A market, which is set to reach fever pitch in the coming months.