Banking in 2020

The banking industry was already set for a lively year in 2020, but even so, the upheaval caused by the coronavirus pandemic came as a huge shock. The virus’ spread resulted in substantial economic damage across many markets, which will consequently have implications for the financial sector as a whole.

Thus far, a great deal of uncertainty remains around the long-term impacts of COVID-19, particularly with regard to how governments and businesses will react. Banks will be charged with providing some welcome stability among the turbulence, but they have challenges of their own to deal with.

Fortunately, technology is helping financial institutions to cope with the disruption, allowing them to maintain a large degree of business continuity while keeping their employees and customers safe. Nevertheless, making sure a limited number of in-person services remain available will be essential, as will ensuring that digital solutions are reliable, efficient and secure.

Aside from the virus, banking is due to face several other market shifts in 2020: a significant number of mergers and acquisitions are expected, building on a spate of similar activity in 2019, with many financial institutions still struggling for growth; the shadow banking market remains an issue (and not only in the developing world); and customers’ growing desire to have access to banking services that are more than just profit-driven shows no sign of abating. These factors, and many others, mean that financial institutions have plenty to grapple with as they move through 2020.

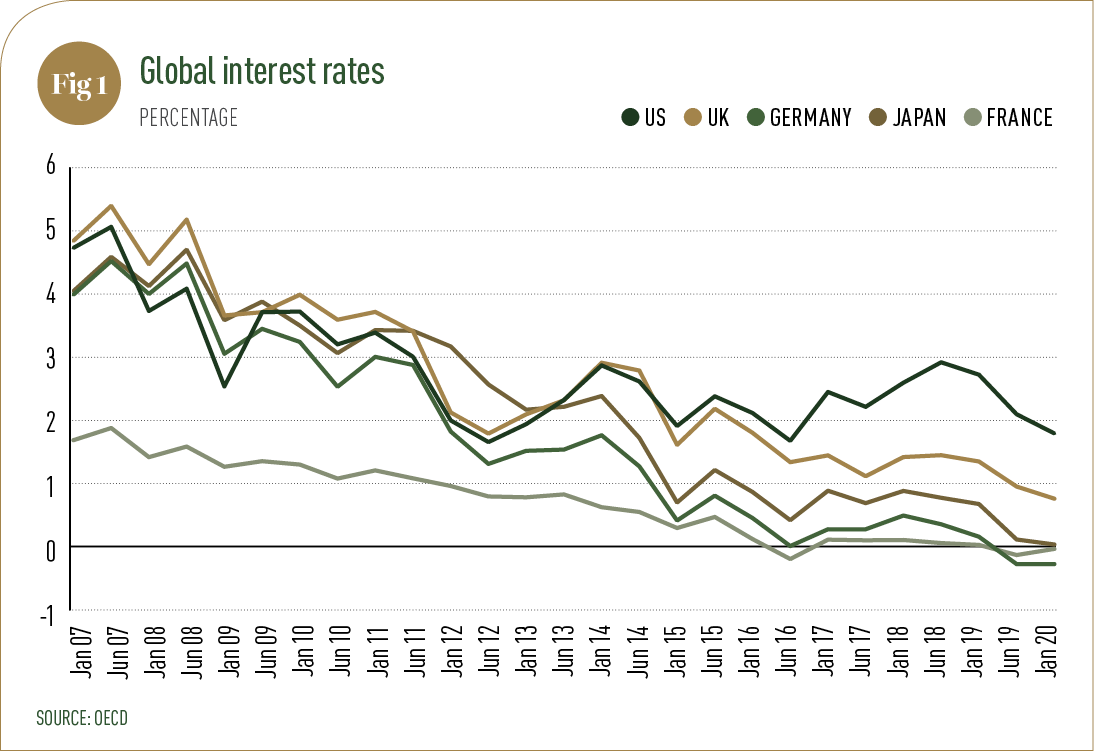

Time to rethink Once thought to be a temporary measure to inject short-term liquidity into the market, low interest rates are proving impossible to shift – for banks, they have already outstayed their welcome. Since the financial crisis, central banks around the world have slashed interest rates, tentatively raising them during periods of economic stability . However, the coronavirus crisis has meant that further cuts may be forthcoming – there has even been talk of negative interest rates being imposed by the US Federal Reserve for the first time in its history.

The problem for the finance sector is that banks make a significant proportion of their profits from charging interest on borrowing. With rates at rock-bottom levels, they have been forced to find new efficiencies in order to protect profit margins. Throughout 2020, this is likely to continue.

In the majority of cases, technology will provide the lifeline that banks are looking for. Digital solutions, from online banking to mobile apps, will allow financial institutions to better differentiate themselves from competitors and reduce their outgoings, all while providing customers with an improved service.

Artificial intelligence (AI) will also see increased adoption. An IHS Markit report from last year predicted that the value of AI in global banking will reach $300bn by 2030, with North America set to become the largest market over the next few years. Voice banking services – the kind that can be delivered by virtual personal assistants like Siri or Alexa – are also set to become more popular. According to a recent survey from Fiserv, more than half of Americans already perceive voice banking to be beneficial. If the coronavirus means that remote services continue to be encouraged by governments around the world, this figure could rise significantly.

Technology will result in other market shifts too, with the emergence of neobanks likely to gather pace over the coming months. They and other fintech operators have caused significant disruption for established banks, many of which failed to foresee the popularity of digital services. They have belatedly started to catch on, which meant that 2020 was initially set up to be a busy year for mergers and acquisitions activity. This was likely to involve the mergers between smaller and mid-sized banks or the acquisition of digital laggards by more innovative players. The COVID-19 pandemic has meant that predictions of such activity may now be out of date.

The spread of the virus calls for strong leadership – this will be just as vital in the banking sector as anywhere else. The right conditions for potential dealmaking may still exist, but stability is likely to be the first port of call – once the safety of employees and customers has been guaranteed, of course.

Finding a purpose Even if disruption from the coronavirus continues throughout the entirety of 2020 – or even beyond – there are some banking trends that are likely to continue unchanged. For a number of years now, customers have been demanding that their financial institutions adopt more sustainable and ethically sound policies. They want a bank driven by purpose, not profit.

The need to please this new breed of customer doesn’t necessarily mean upsetting investors: many banks are choosing to move away from supporting ethically questionable organisations, like fossil fuel companies, because it is financially prudent to do so. Earlier this year, research undertaken by asset manager BlackRock found that funds with high sustainability ratings performed better during a market sell-off.

In order to ensure banks consider the needs of all their stakeholders, relationship managers will become increasingly important. They will be tasked with accumulating important feedback from clients and customers about how the bank is performing, what services are operating satisfactorily and which ones are being badly received. Some banks struggled to maintain relationships during the height of the coronavirus pandemic as more of their staff worked remotely. As social distancing measures are eased globally, these relationship managers will be tasked with shoring up any damaged partnerships while also securing new ones.

Relationship managers – and, indeed, their colleagues in other roles – will also have to keep customers from leaving their traditional banks to access services from non-bank lenders or shadow banks. Although the number of these institutions has fallen this year, they remain widely available and have previously posed a significant risk for the finance sector in markets like India and China. The 2020 World Finance Banking Awards shine a spotlight on the organisations that have excelled across investment, private, retail and commercial banking during the year, helping to protect the industry’s long-term future in difficult circumstances. Congratulations to all our winners.