Banking Groups

Germany

BNP Paribas

In recent years, Germany has become a core market for the BNP Paribas Group. Having been active in the eurozone’s largest economy since 1947, it is now one of the biggest non-German banks in the country, with more than 5,300 staff and 3,000 corporate clients. Capitalising on this position, BNP Paribas aims to develop a strong digital and mobile banking network in Germany.

group.bnpparibasFrance

Crédit Mutuel

Crédit Mutuel provides a range of services, including asset management, bancassurance and investment solutions, to its 34 million customers. Its technological expertise has received a great deal of praise, as have its corporate social responsibility policies, which take into consideration environmental issues, governance factors and employee wellbeing to ensure all stakeholders are prioritised.

www.creditmutuel.frGhana

Zenith Bank (Ghana)

Zenith Bank has taken a leading role in terms of digitalisation, becoming synonymous with cutting-edge IT solutions, including its ZMobile app. Zenith continues to support its network of physical branches to ensure customers have a variety of ways to meet their banking needs: online or in person, the bank is committed to delivering the highest standards of customer service.

www.zenithbank.com.ghCyprus

Eurobank Cyprus

With 653 branches internationally and total assets in excess of $62.7bn, Eurobank has grown significantly since it was first established in 1990. The group is one of four systemic banks in Greece, holds a strategic position for both retail and business banking in Bulgaria and Serbia, and offers wealth management services in Luxembourg, London and Cyprus.

www.eurobank.com.cyChile

Banco Internacional

Whether it is delivering personal or business banking services, Banco Internacional’s values remain the same: a commitment to flexibility, transparency, quick and timely responses, and a highly personalised service. Cash management is just one solution the bank offers its business clients and includes a 24-hour service, a corporate credit card and consultations with a personal account executive.

www.bancointernacional.clFinland

Nordea

With a group history stretching back to 1820, Nordea certainly does not lack experience in the banking sector. Over its two centuries of operations, it has continually strived to grow and develop, and now boasts a customer base of around 9.3 million. It is also one of the top 10 financial services companies in Europe based on market capitalisation.

www.nordea.comDominican Republic

Banreservas

As the leading banking group in the Dominican Republic, Banreservas understands that its role in society is not limited to providing banking solutions. The firm promotes financial education and other social initiatives, with its Prospera programme facilitating the growth and competitiveness of the Dominican Republic’s productive sectors.

www.banreservas.comBrunei

Baiduri Bank

Over the past year, consumers across Brunei have embraced digital banking solutions with increased fervour. Baiduri Bank has been one of the main drivers of this, having invested heavily in new technologies, including contactless payments and digital wallets. One of the largest banks in the country, Baiduri Bank now has several years of strong growth under its belt.

www.baiduri.com.bnMost sustainable Bank, Jordan

Jordan Islamic Bank

One of Jordan Islamic Bank’s primary aims is to finance a green future for its customers. It was the first bank in the country to offer a 30 percent subsidy for domestic solar-powered heaters and, in the future, it plans to use its renewable energy fund to stimulate the local economy and drive further investment for renewable energy solutions.

www.jordanislamicbank.comNigeria

Guaranty Trust Bank

Headquartered in Lagos, Guaranty Trust Bank has consistently delivered innovative financial solutions and exceptional customer service since it was founded in 1990. It has also received praise for its policies supporting local communities through social responsibility initiatives. Proudly African and truly international, the bank believes finance can play a fundamental role in enriching lives.

www.gtbank.comIndonesia

OCBC NISP

Established in 1941 in Bandung, the capital of Indonesia’s West Java province, OCBC NISP has stayed true to its values of transparency, prudence and reliability since its founding. After withstanding several national economic crises, the bank has not only survived but prospered, and today is proud to supply customers with a host of traditional and digital banking services.

www.ocbcnisp.comSpain

Banco Santander

Multinational bank Banco Santander operates predominantly across 10 main markets, including its native Spain. The group has become one of the eurozone’s largest banks by taking a customer-centric approach and accelerating digitalisation so the shifting needs of the modern consumer can be met. Its corporate culture is the foundation underpinning all its operations.

www.santander.comTurkey

Akbank

With a strong domestic network of 758 branches, Akbank is one of the largest presences in the Turkish banking sector. With its reliable, dynamic and people-orientated approach, Akbank is able to offer technological advances to its customers through investing heavily in key digital innovations. The bank aims to deliver a comprehensible, user-friendly experience at every point of contact.

www.akbank.comMacau

ICBC (Macau)

By tailoring its offering to each individual customer, ICBC (Macau) is able to offer unparalleled service and value for its clients. In particular, it actively participates in Macau’s strategy to develop the Greater Bay Area by promoting the development of the region’s specialised financial system, while also playing a leading role in China’s One Belt, One Road initiative.

www.icbc.com.moJordan

Jordan Islamic Bank

Jordan Islamic Bank’s primary aim is to improve financial inclusion across Jordan, in particular by targeting young people, women and SMEs on their first steps towards financial literacy. This is especially important in a country where only 42.5 percent of adults have a bank account, according to the World Bank’s most recent data.

www.jordanislamicbank.com

Leaders of the pack

The year ahead is shaping up to be a challenging one for businesses, regardless of size. Banking groups will need to be open, transparent and well-led in order to thrive in this environmentAll is not well in the banking sector. Low interest rates have hit banks’ profit margins hard, and there is every indication that they are here to stay for the foreseeable future. At the same time, financial institutions have had to grapple with changing regulations and heightened competition across the board.

While banking groups generally operate on a large scale and have sizable income streams, this does not mean they are immune to the challenges affecting the finance sector: they may also have larger outgoings than smaller financial entities and can more easily succumb to complacency. Several of the world’s best-known banking groups have histories stretching back over a century – unsurprisingly, some of them have begun to feel untouchable.

But despite its longevity, the banking sector is not monolithic. In recent times, it has been disrupted by artificial intelligence, mobile apps, fintech companies and neobanks. Regulatory changes have also encouraged customers that may once have stayed loyal to a tried-and-trusted brand to move their money elsewhere. For banking groups that lack agility, this has added to their woes.

Not all banking groups are mired in inertia, though. The organisations singled out for praise by this year’s World Finance Banking Group Awards are among the industry’s most innovative players.

Open for business One of the biggest changes that banking groups have had to get to grips with is open banking. While this concept originally came into force in early 2018, it has yet to truly take off – there is hope that 2020 will be the year it finally reaches its potential. In its simplest terms, open banking is a series of reforms that affect how banks hold financial information. Under the new rules, banks must share customer financial data, such as how and when they spend their money, with other authorised financial service providers (providing the customer gives their consent). These other providers may include budgeting apps and, indeed, other banks. In this more open environment, it is hoped that new products and services can be produced, leading to a better banking sector for all stakeholders.

Getting prepared for the world of open banking has come easier to some institutions than others, however. According to open banking platform Tink, only 41 percent of European banks managed to meet the March 2019 deadline to establish a sandbox environment for third-party access. Many have also struggled to make their application programming interfaces available.

Although banks have, for good reason, usually encouraged a risk-averse culture, this has allowed fintech firms and neobanks to outflank them, offering cheaper and more convenient services to consumers. The best banking groups understand that consumer tastes are changing. Customers have long expected digital innovation in industries like retail, healthcare and hospitality – now, they expect it from their bank too.

Crucially, banking groups that view open banking as an opportunity rather than a challenge are faring best. The ability to share information with third parties provides a fantastic chance to launch new products, and is likely to inspire new feats of collaboration. Banking groups need not fear third parties gaining access to their customer data: as long as they have the appropriate security protocols in place, open banking can lead to a brighter future for established banks, new players and customers alike.

Moving forward With such large financial rewards on offer, the banking sector has always been open to abuse from disreputable players. For banking groups, even when blame can easily be attributed to a particular actor, reputational damage to the entire organisation can be hard to shift. Often, large-scale changes are required.

At Swedbank, new CEO Jens Henriksson believes that his firm is only now coming to the “beginning of the end” of a scandal that first came to light more than a year ago. To regain trust, Henriksson has been blunt about the bank’s failings, accepting responsibility on behalf of the entire group for the missteps that allowed money laundering to take place on a mass scale. Other banking groups can surely learn from the way Swedbank and other organisations have responded to their troubles.

The first thing to do is conduct a proper assessment when an incident occurs. This ensures a full apology can be issued and reduces the likelihood of any nasty surprises coming to light while the fallout is taking place. The next steps involve publicly acknowledging the problem, formulating a strategic response and implementing response tactics.

Of course, prevention is always preferable to a cure, so banking groups should ensure they adhere to current regulations. The regulatory outlook for banking in 2020 will likely see a renewed focus on banks’ resilience, particularly as multiple markets attempt to recover from economic distress.

One route to greater financial security is through the adoption of new technologies, but these come with their own compliance issues. Aside from data security challenges, many institutions choose to implement new defence protocols at the same time that they overhaul their technology infrastructure. The ‘three lines of defence’ framework has proved popular: this approach involves safeguarding the business itself, then looking at independent risk functions and, finally, conducting an internal review.

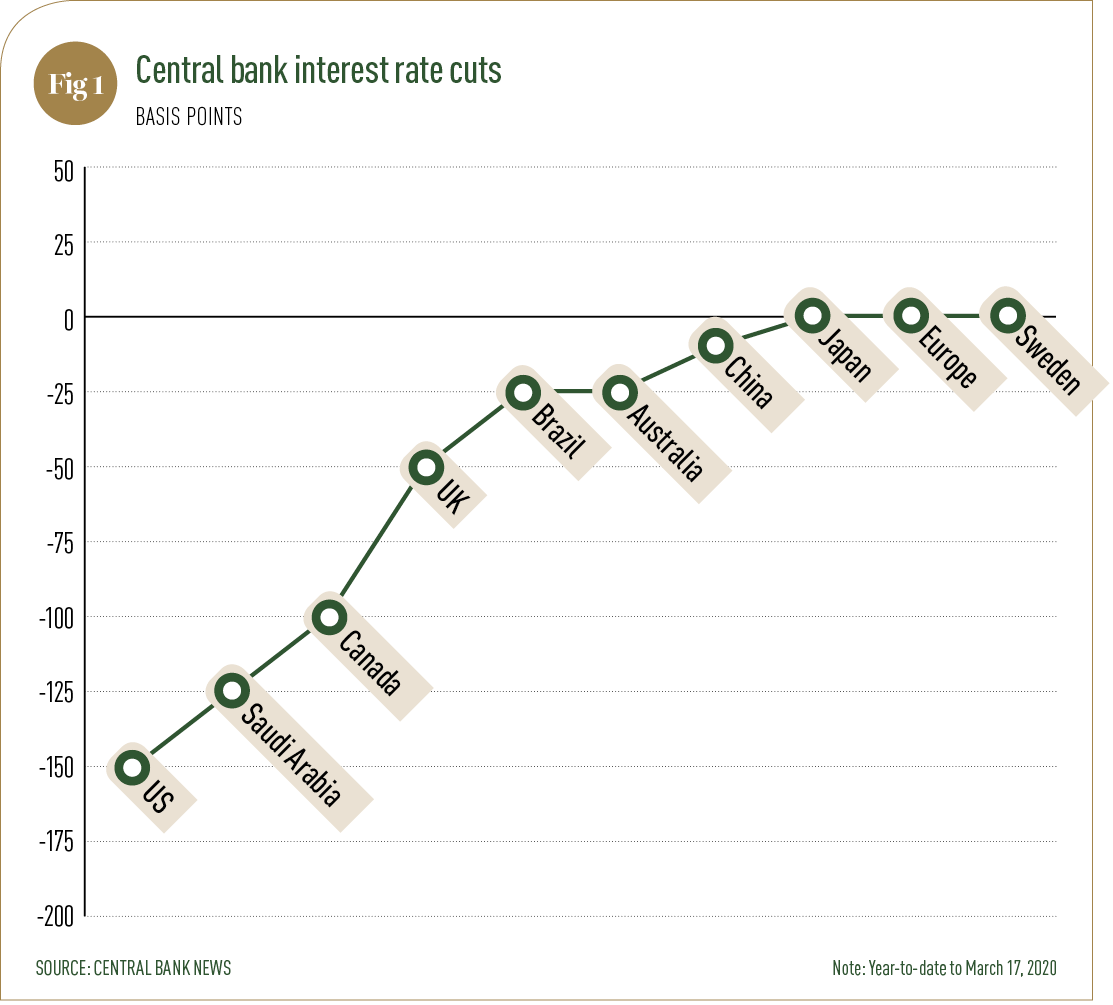

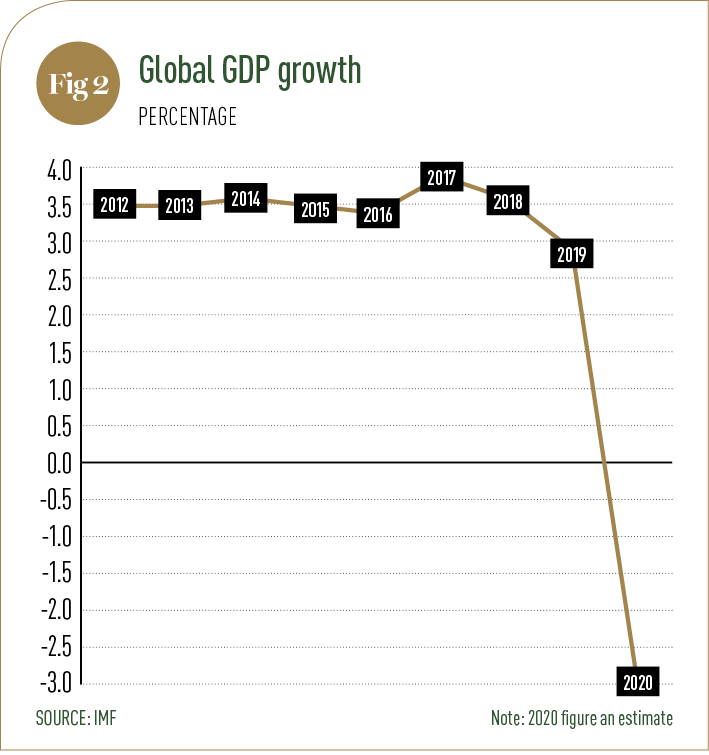

It is no surprise that Swedbank felt the need to change its CEO in order to move beyond its recent difficulties. Strong leadership is vital in the banking sector, and never more so than during a crisis. With 2020 expected to be a difficult year for many markets – the April World Economic Outlook predicts global growth will fall to minus three percent this year – there will inevitably be a knock-on effect for banking groups. Having the right members of staff in leadership positions will provide some stability in these troubling times.

As banking groups navigate a changing and uncertain world throughout 2020, their survival and success will rest on their staff as much as it will their technological innovations. The top banking groups in this year’s World Finance Banking Awards strike the perfect balance between human and digital excellence.