Introduction

If one were forced to sum up banking today with a single word, ‘disruption’ would be a real contender. Perhaps more so than at any other time in the past 100 years, the sector is facing rapid change, and will continue to do so for the foreseeable future.

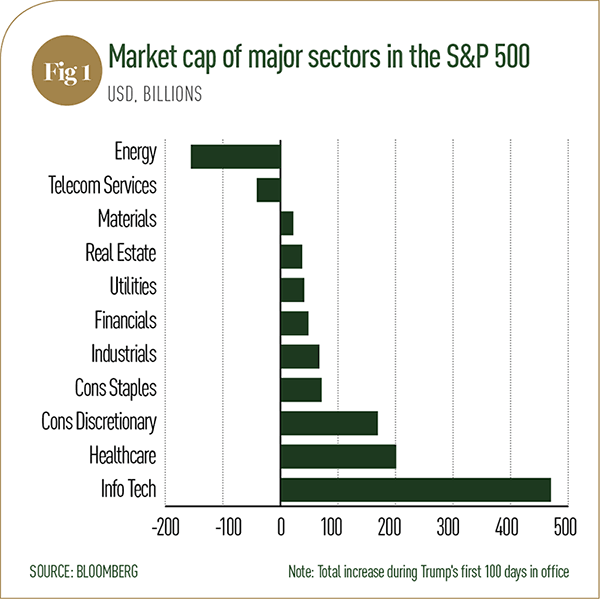

Many change-enforcing incidents have crept up on a largely unsuspecting global market, with the accompanying levels of shock contributing to the impact they have had. The obvious two events, of course, were the UK’s unexpected decision to leave the EU, and the once-unthinkable election of reality TV star and business mogul Donald Trump to the US presidency. The ripple effects of both events continue to surprise. Trump’s election, for example, saw the steepest rally of stock markets since the election of John Fitzgerald Kennedy in 1961, with many of the US’ biggest companies buying into Trump’s ‘make America great again’ campaign (see Fig 1). And across the pond in the UK, the uncertainty surrounding the Brexit deal deepened when Prime Minister Theresa May called a snap election, despite previously vowing to do no such thing, imbuing the whole affair with an unwelcome sense of chaos.

The unknown While major political developments are a natural part of a system that is deeply intertwined with the global economy, what makes the aforementioned events all the more disconcerting is the level of doubt and ambiguity that accompany them. In Trump, we have a US president who is known for brash decisions and extreme reactions. Put simply, with Trump, anything could happen. A visa ban for Muslim countries and a withdrawal from the long-awaited Trans-Pacific Partnership are just two examples of his hasty style of presidency – a style from which markets have rapidly recoiled. Meanwhile, the UK’s general election in June caused another unforeseen problem – a hung parliament, which has made the process of negotiating Brexit all the more difficult. What’s more, the unexpected outcome could well result in a yet another trip to the polls in the coming year and, potentially, a new prime minister at the helm. This would only delay negotiations further, adding even greater uncertainty to an already precarious landscape.

Tech disruptors Set against this backdrop of uncertainty, there also happens to be a revolution taking place in the global banking sector. In this case, however, the biggest disruptor over the past year has not been the lingering consequences of Brexit, nor the chaos of the Trump regime – it has been innovation. New technology is changing the way people bank, how banks are perceived and even the very nature of financial institutions. Though brewing for a few years, 2017 has seen more of these changes take effect than any other time this decade. Gone are the days when great client service was a matter of meeting face-to-face in high street branches, banks getting away with offering one-size-fits-all products, and neglecting fairness in the workplace. Nowadays, customers demand bespoke service and offerings, with ever-increasing convenience treated as a given. Customers also expect banks to incorporate social responsibility, good corporate governance and environmental awareness into their business models. Thanks to the internet and the nature of online news, institutions must act honourably and be seen to do so. Any disrespect for staff, customers or the environment spreads like wildfire, and a damaged reputation is harder than ever to recover, especially given the intensity of competition in the modern marketplace.

Adapt and improve Of course, technology has not just affected traditional banks; non-bank financial institutions are now popping up everywhere. These tech start-ups don’t look or sound like banks, and many of them don’t even have branches to speak of. But they are tapping into the rapidly changing needs of customers – they incorporate blockchain technology, offer cutting-edge cybersecurity, and provide a highly personalised service based on data insights. With their inherent agility and tech prowess, these new players are giving traditional banks a run for their money. Long-standing institutions, in response, now urgently need to either invest in tech or look to partner up. Indeed, partnerships are now all the rage; notable examples include JP Morgan Chase’s deal with OnDeck Capital to offer small business loans, and Rabobank’s partnership with Tradle for software that checks client identities using distributed ledger technology. These partnerships are emblematic of banking’s changing landscape. Indeed, they represent a shift in strategy, which has seen banks strike alliances with small start-ups, changing the latter from a threat to a means by which they can offer a better experience to their customers.

Bright horizon As well as the technological side of things, banking’s regulatory environment has also entered a state of flux. After years of slow growth, advanced economies are now seeing tough regulations being scaled back as central banks look to kick-start a more rapid recovery. Of course, while such a change is welcome relief for some, it has set alarm bells ringing for others. In the US, President Trump has signalled his intention to crack down on the Dodd–Frank Act, raising fears of a return to the wild risk-taking that caused the 2008 financial crisis. In Europe, on the other hand, the Basel Committee on Banking Supervision is finally close to concluding its Basel III reforms, which are expected to enforce recovery and resolution planning at large institutions, together with a shift towards central clearing and higher transparency standards.

Clearly, regulatory frameworks still need to be ironed out and institutions need to get used to them. However, as onerous as they may be, the banking industry in 2017 is still rife with opportunities for growth. Partnerships with start-ups, mobile banking, biometric security, greater optimism from businesses and slowly rising interest rates have contributed to a year that has been surprisingly positive, particularly in comparison to the recent past.

Trump and Brexit may have added a grave sense of uncertainty to the market environment, but these elements do not form the complete story of 2017 in banking. The opportunities available for banks that embrace innovation and change have perhaps never been greater; it’s during such periods of flux that the market leaders of tomorrow can first assert their dominance, toppling established hierarchies to lead the industry into the future. The time is ripe to connect with Millennials by developing strong environmental, social and governance policies, promoting fairness, and embracing technology. The 2017 World Finance Banking Awards look to recognise and reward these qualities, picking out the firms that have ridden out the storm successfully, set the industry’s tone for the future, and contributed to a more open industry. Congratulations to all our winners.