Zenith Bank and the new African economy

For decades, Africa’s growth story was framed around potential. Today, it is increasingly about execution, integration and capital. Zenith Bank’s expansion across the continent reflects a broader shift in African finance, as homegrown institutions seek to power trade, investment and economic transformation from within. Dame Dr. Adaora Umeoji, OON, Group Managing Director/CEO at Zenith Bank spoke exclusively with World Finance

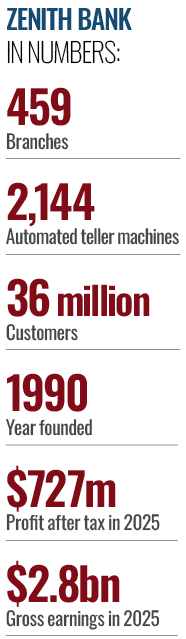

When Jim Ovia, CFR, founded Zenith Bank in May 1990, the unity and prosperity of Africa were among his greatest dreams. For the renowned businessman, banker, and philanthropist who went on to paint the picture of the continent he envisioned in his book, Africa Rise and Shine, one thing was crystal clear: building a formidable financial institution was a potent catalyst for Africa’s transformation.

In three and a half decades, Zenith Bank, his brainchild and the bank in which Ovia CFR previously served as chairman, has been integral in Africa’s remarkable metamorphosis into a continent expected to anchor global growth in the coming decades. Today, the International Monetary Fund’s World Economic Outlook ranks 11 of the world’s 15 fastest-growing economies in Africa, and the continent is among the world’s most resilient regions. In 2026, the African Development Bank’s African Economic Outlook puts Africa’s growth at 4.2 percent, among the highest globally.

For Africa, the journey toward unity, with 54 nations now pursuing shared and common goals, has been fundamental. For instance, the unity of purpose brought about by the African Continental Free Trade Area (AfCFTA) and the push to integrate payments through the Pan-African Payment and Settlement System are clear indications of a continent on the rise. The impacts of AfCFTA are nothing short of phenomenal. The agreement has created the world’s largest free trade area, a single market of over 1.4 billion people with a combined gross domestic product (GDP) of $3.4trn.

Zenith Bank has been central to Africa’s economic ascent. On this, the bank has been deliberate. From its home market in Nigeria, and through a business strategy anchored in people, technology, and service, Zenith Bank has evolved over the years into a top financial institution in Africa with a solid financial foundation. Today, the bank is not only Nigeria’s largest financial institution by Tier-1 capital but also one of Africa’s leading banks, a far cry from its modest beginnings when it commenced operations in July 1990.

While building the requisite financial scale has been critical, ensuring it meets market needs has been another masterstroke. In this regard, Zenith Bank offers a wide array of financial products and services for individual and corporate clients. The solutions span corporate and retail banking, commercial and consumer banking, personal and private banking, and investment banking. These include trade services and foreign exchange, treasury and cash management services, and other non-bank financial services mainly offered through its subsidiaries.

These solutions, supported by massive investments in technology and a deeply entrenched culture of innovation, have driven exponential growth across all metrics. Cumulatively serving 36 million customers, the bank operates an extensive branch and ATM network at home and also has a presence in the UK, France, Sierra Leone, the Gambia, the United Arab Emirates, as well as a representative office in China. In recent months, the bank has also embarked on a Pan-African expansion strategy, entering Côte d’Ivoire and Kenya.

Profitability anchored on execution

For Zenith Bank, one of its outstanding trends has been sustaining a strong culture of profitability through every economic cycle. In 2025, the bank once again lived up to this mantra, posting ₦1.04trn ($727m) in profit after tax. The performance was reinforced by robust capital and liquidity positions, both well above the regulatory minimum, alongside a prudent risk management culture that kept non-performing loans well in check.

Zenith Bank has been central to Africa’s economic ascent

One key metric in which the bank was an exceptional performer was cleaning its bad-loan book. In a policy directive, the Central Bank of Nigeria (CBN) required banks to clean up legacy exposures previously held under regulatory forbearance by June 30, 2025. Zenith Bank used the transition to clean its books, implementing measures such as write-offs and loan recoveries. Owing to decisive actions, the bank managed to reduce its non-performing loan (NPL) ratio substantially from 4.7 percent in 2024 to 3.8 percent in 2025, well clear of industry norms.

The Nigerian banking industry is highly competitive, and Zenith Bank’s impressive results reflect disciplined, focused execution of its strategy. Specifically, the bank has been astute in strengthening its asset quality, optimising its balance sheet and investing in capabilities to propel growth. A key differentiator during the year was the bank’s strong position in international trade and foreign exchange flows.

In recent years, Nigeria has been on a mission to reduce its dependence on the oil sector, which is a major source of forex and government revenues. Data from the Nigerian Export Promotion Council indicate that in 2025, the country’s non-oil exports reached a historical high of $6.1bn, an 11.5 percent increase from $5.4bn in 2024. As a key facilitator of international trade, Zenith Bank played a central role in repatriating over 40 percent of Nigeria’s non-oil export proceeds. Owing to its role, the bank was able to deepen relationships with large corporates and supported transaction-led income. The franchise remains critical for the bank, as trade finance generates recurring business, strengthens customer relationships, and supports foreign currency liquidity.

Apart from the trade sector, Zenith Bank also maintained a disciplined lending approach, which led to gross loans rising to about ₦11trn ($7.9bn). The major focus was on viable sectors such as manufacturing, agriculture, and telecommunications, as well as key value chains that offered more predictable cash flows. Non-interest income from fees, commissions and digital channels also contributed to the impressive performance, supported by a steady push in digital transformation that improved customer experience, increased transaction volumes and lowered operating costs. Also impactful was the high-interest-rate environment, which supported returns from the loan book and from investments in government securities.

For Zenith Bank, the high-interest-rate environment delivered strong returns across lending and investment activity. Through 2025, the Monetary Policy Committee held the policy rate at 27.50 percent at its February, May and July meetings before easing it 50 basis points to 27.00 percent in September. Inflation also moderated through the year, with the National Bureau of Statistics putting the annual 2025 average at 23.01 percent. Average private-sector credit stood at ₦75.6trn ($54.8bn) for the year, up from ₦75.3trn ($54.6bn) in 2024, with well-capitalised banks like Zenith positioned to grow lending as the easing cycle takes hold.

Reform momentum

Nigeria’s broader economy has undergone a transformative period of reform. The removal of fuel subsidies, the unification of exchange rates, and sustained monetary tightening have significantly helped correct long-standing distortions. The reforms have improved price discovery in the foreign exchange market, strengthened fiscal revenues, and restored investor confidence. A key pointer is capital inflows. Government data show that last year, inflows surged by 90 percent, driven by foreign portfolio investment as investors returned to Nigeria. During the year, net capital investments stood at $23.2bn, up from $12.3bn in 2024.

For the Nigerian economy, the reforms’ impacts have been encouraging. Growth has remained resilient, supported by services, higher oil production, stronger non-oil activity and a gradual recovery in external balances. According to the National Bureau of Statistics, real GDP growth in 2025 was 3.87 percent, up from 3.38 percent in 2024. This year, growth is projected to accelerate further to 4.4 percent. The rate of economic expansion is inspiring, and the next step is to ensure it translates into investment, jobs, food security, and stronger household purchasing power.

Nigeria’s economy has undergone a transformative period of reform

This is necessary, given that Nigeria, Africa’s third-largest economy with a rebased 2025 GDP of ₦441.5trn (about $320bn) per the NBS, is well positioned to build on its momentum. Hard work and tough decisions have been instrumental in stabilising the economy. Going forward, the next natural course of action is to ensure that the positive economic momentum translates into better living standards for Nigerians.

The government continues to advance its socio-economic agenda with strong intent. Building on the reform momentum, priority areas include productivity, employment, agricultural security, market access and logistics, all of which are reinforced by sustained delivery of the broader reform programme.

Over the medium term, the focus is shifting to inclusive growth. Agriculture, SMEs, manufacturing, digital enterprise and labour-intensive services are positioned to benefit from financing, infrastructure and policy support that creates jobs. Macroeconomic stability, paired with policies that strengthen household purchasing power, sets the stage for growth to translate into real prosperity.

In your best interest

The government has framed the reforms as the foundation for long-term gains. For the banking sector, the reforms have already brought a retinue of benefits. Among the benefits is the liberalisation of the exchange rate. For banks with strong foreign currency positions, this has led to an increase in foreign exchange trading income and revaluation gains. Besides, the high interest rates have supported net interest margins as asset yields repriced faster than funding costs in the early phase of tightening. Also, higher yields in the fixed-income market have provided attractive risk-adjusted returns on sovereign instruments.

Another benefit has been the recapitalisation of banks, which has built stronger capital buffers to support larger transactions, deeper credit intermediation, and greater financial system resilience. For Zenith Bank, the exercise has been more than a regulatory compliance to meet the raised minimum capital requirement for commercial banks with international authorisation to ₦500bn ($362.6m). Completed ahead of the CBN’s March 2026 deadline, the bank raised over ₦350bn, lifting its capital base to ₦614bn ($445m), comfortably above the threshold. The bank sees its enlarged capital base as a strategic foundation for growth, resilience and deeper real-sector financing. Specifically, the bank now has the balance-sheet strength to finance large and long-tenor projects not only in infrastructure but also across sectors that require patient capital and larger balance sheets.

For two of Zenith Bank’s key market segments, namely retail and SME banking, the importance of the new base is elevated to higher realms. First, it adequately equips the bank to support the two segments at scale. Second, it positions the bank to lead in an industry where consolidation is reshaping the competitive landscape, with well-capitalised institutions like Zenith Bank best placed to capture the opportunity.

Zenith Bank views retail as the engine of its long-term scalability, and the numbers back that up. In 2025, the bank’s total customer deposits stood at about ₦24trn ($17.4bn). Of this, retail deposits accounted for about ₦4.9trn ($3.5bn). Though corporate and commercial credit account for the bulk of the loan book, the bank disbursed nearly 3,000 retail loans valued at about ₦89.5bn ($65m), supporting household and individual financial needs. The segment’s significant contribution makes it central to the bank’s growth, particularly in providing a stable deposit base and deepening financial inclusion.

To grow its retail business, Zenith Bank has been proactive in expanding its digital offerings. For instance, migrating to a new core banking platform has improved speed, usability, and service quality. Also, enhancements to the internet banking solution now offer customers access to a redesigned interface with broader functionalities. These include cross-border intra-African transfers, treasury bill investments and payment of government levies. The bank is also expanding its physical channels, including agency banking aimed at underserved communities. Through this channel, the bank has reached over four million customers.

Another critical market that Zenith Bank is strategically determined to grow is the SME market. CBN data points to a ₦130trn ($94.4bn) MSME financing opportunity in Nigeria, reflecting the segment’s central role in job creation and broader economic activity. The bank is meeting the segment with innovative lending products tailored to its collateral, record-keeping, and credit history. Owing to their importance, Zenith Bank’s determination to support SMEs is anchored in its development priority and as a major commercial opportunity. Part of the bank’s lending solutions include cashflow-based finance, asset and equipment finance, the Z-Woman loan for women-led enterprises, and cooperative lending, among others. The bank has also been keen on building partnerships with multilateral financiers and export credit agencies that provide medium to long-term lines of credit for on-lending. This has been instrumental in reducing risk and widening access to credit for SMEs.

The Pan-African gear

That Zenith Bank has reached several significant milestones, cutting across capital fortification, products and services, and digital innovation, is indisputable. Having reached the pinnacle of becoming a Nigerian banking powerhouse, the bank is now transforming into a pan-African financial institution. Unlike its peers, the bank’s expansion strategy is not just about adding flags to a map. Rather, the ambition is driven by client demands, trade flows and regional economic connectivity, with the ultimate goal of supporting cross-border trade and capital flows for its wide range of multinational customers. Effectively, the bank is deploying a strategy that combines both greenfield and brownfield approaches to enter new markets. The strategy aligns with Founder Jim Ovia’s unequivocal desire to build a truly global brand with a strong presence across Africa and key international markets.

The bank now has the balance-sheet strength to finance large and long-tenor projects

On expansion, Francophone West Africa and Anglophone East Africa are a no-brainer for Zenith Bank. While the former offers access to a large integrated market, particularly through the West African Economic and Monetary Union (WAEMU) bloc, the latter provides a dynamic corridor with strong private-sector activity, capital market depth and advanced digital banking adoption. Notably, Zenith Bank is not going into new markets blindly. The bank is taking time to identify opportunities that it seeks to exploit and capture. These cut across corporate banking, trade finance, remittances, payments and structured transactions. More critically, the bank intends to prioritise countries with strong fundamentals, trade relevance and clear links to its existing client base. In essence, its expansion is a corridor strategy spanning the WAEMU, CEMAC and EAC blocs, not a race for geographic spread.

In April, Zenith Bank launched operations in Côte d’Ivoire and entered Kenya through the acquisition of a 100 percent shareholding of Paramount Bank. In line with the bank’s vision, the two markets are strategic gateways. In November 2024, the bank entered France, which is commercially linked to several Francophone African countries. The fact that Abidjan has grown into a major regional business hub means that Côte d’Ivoire was a natural first-step choice. Using the market as a springboard, the bank intends to support trade finance, payments and corporate banking across the WAEMU bloc, where a shared currency and integrated regulation reduce fragmentation.

Kenya, on its part, is expected to provide an anchor in East Africa. As the region’s top economy with $136bn in GDP, the country is a financial nerve centre with deep capital markets, a sophisticated private sector and booming digital banking innovations. By acquiring Paramount Bank, Zenith Bank has gained immediate market presence through seven branches, an established customer base, experienced local teams, and regulatory standing.

Zenith Bank is building for sustained relevance in its new markets, drawing on its Nigerian playbook while tailoring to each market’s local dynamics. To gain traction, the bank is taking a deliberate and structured approach, riding on local partnerships, talent, strong governance, careful attention to market realities and digital capability. Patience will be cardinal, with growth deliberate, risk-managed and aligned with client needs.

Even as it aspires to become a pan-African financial institution, some core principles will remain embedded in Zenith Bank’s DNA. Top is the bank’s strong corporate governance culture. Across the spectrum of its operations, governance is anchored on an enterprise risk management framework aligned with COSO and ISO 31000, a Three Lines of Defence control model, and independent board committees overseeing risk, audit and compliance.

The bank’s expansion strategy is not just about adding flags to a map

Another deeply entrenched principle is sustainability. On this, the approach is premised on the fact that environmental, social and governance (ESG) issues are financially material, with reporting aligned to the ISSB IFRS S1 and S2 standards. In essence, it means that ESG has a direct effect on credit quality, operational resilience, regulatory readiness, investor confidence and long-term value creation.

Overall, Zenith Bank remains committed to integrating sustainability into risk management, credit processes, and strategic planning. A case in point is in project finance transactions. In 2025, some 94 percent of new and existing transactions were assessed for environmental and social risks. The bank also actively monitored 95 percent of financed projects. For the bank, sustainability is closely intertwined with corporate social responsibility (CSR). On CSR, the bank is conscious of the fact that its success is inextricably linked to the well-being of the communities it serves. For this reason, Zenith Bank has been giving back to society in areas such as security, sports, health, and education.

Three and a half decades after Zenith Bank’s founding, Jim Ovia’s vision of a continent on the rise, as captured in Africa Rise and Shine, has become the daily work of the institution he built. With a deep capital base, an expanding African footprint, and a strategy that reads as patient as it is bold, Zenith Bank is positioned to write the next chapter of the African economy from within.