Sign In to continue reading the premium content or subscribe to one of our premium plans:

Already a memeber? Manage your profile here!

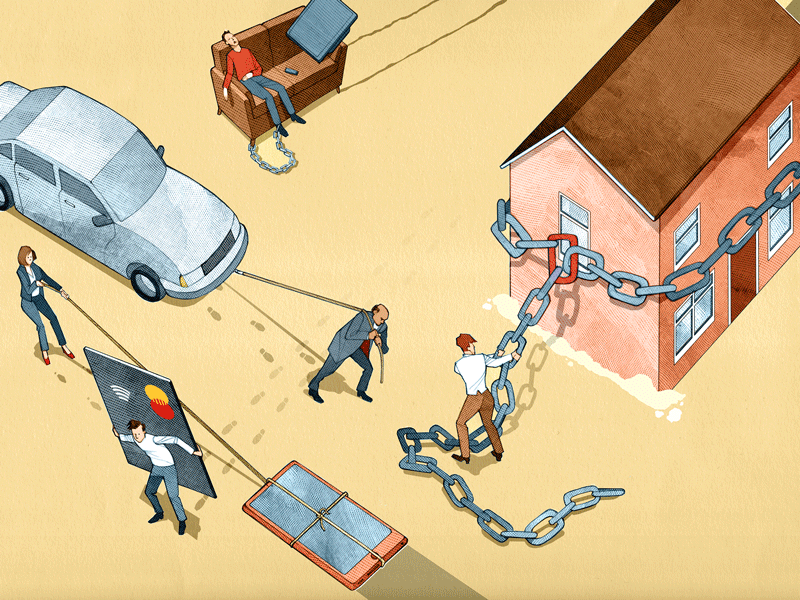

The pace of overall growth in the global economy is increasing. However, this economic expansion also brings a rise in the level of public and private debt, which could pose a serious threat to the long-term health of global markets

Sign In to continue reading the premium content or subscribe to one of our premium plans:

Already a memeber? Manage your profile here!