Top 5

In global finance, the word ‘innovation’ often evokes digital platforms, premium services or algorithmic models. Yet the most transformative advances in banking are not technological in isolation. They are structural: designing products, processes and systems that expand access, resilience and trust.

This has been Banco Azteca’s mission from the start. In Mexico, financial exclusion was once treated as inevitable. By embedding inclusion into its very architecture, the bank has built a model that is both commercially robust and socially relevant. The recognition by World Finance as the ‘Most Innovative Company in the Banking Industry 2025’ reflects not a single app or feature, but a system-wide commitment to innovation as infrastructure.

Banco Azteca’s inclusive product design demonstrates that innovation can extend far beyond technology. Guardadito, the bank’s foundational savings account, remains the first formal financial tool for millions of Mexicans, with more than 24 million active accounts. SOMOS, created by women for women, integrates savings with access to legal, medical and psychological support, now serving over 680,000 women. Guardadito Amigo and Sin Fronteras, tailored for migrants, refugees and their families, have grown to more than 150,000 accounts by mid-2025.

These products are not pilots. They are regulated, permanent and available in every branch nationwide. Their impact shows that innovation also means permanence: turning exclusion into participation by making inclusion part of the core banking system.

Digital at scale, but not alone

Technology plays a critical role, but it is part of a wider ecosystem. Banco Azteca’s app has become one of the largest digital banking platforms in the country, with more than 23 million users. Two-thirds of all transactions and more than half of savings account openings now happen digitally.

The app was designed from the ground up for first-time users: intuitive, hybrid and linked to 2,000 branches that remain open 365 days a year. This hybrid approach means clients can move seamlessly between digital and physical channels. For many, the app is their first interaction with a formal financial institution, yet they know they can still rely on face-to-face support if needed. What makes this digital model innovative is not technology in isolation, but how it complements human-centred infrastructure to scale trust.

Banco Azteca’s app has become one of the largest digital banking platforms in the country

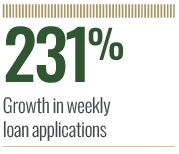

Innovation also extends to how credit is originated and serviced. The Unified Loan Origination Process, launched in the past year, has standardised applications across physical and digital channels. Weekly loan applications have grown 231 percent, with digital origination up 75 percent, and today 68 percent of all loans originate digitally. More than half of repayments are made directly in the app. By simplifying processes, embedding real-time tracking and allowing repayment without cost or travel, the bank has redefined access to credit for millions of households. Here again, innovation is not just technological; it is behavioural, designed around how people actually live and work.

Trust as institutional innovation

Banco Azteca’s Apoyar Nos Toca programme illustrates that innovation is not limited to products or technology. It can also mean rethinking how a bank builds legitimacy and social resonance. By supporting merit-based causes such as Mexico’s Physics Olympiad delegation, rural students in Oaxaca, and outstanding artists, the initiative generated over 50 million organic impacts in 2025. What distinguishes it is not philanthropy, but a new model of reputational strategy, one that transforms selective sponsorships into scalable trust-building infrastructure, linking institutional purpose with national pride.

Banco Azteca’s model suggests a broader lesson for global finance. Innovation is not only defined by apps, nor by short-lived pilots. It is about permanence, replicability and resilience. At Banco Azteca, inclusion is designed as infrastructure: products that last, processes that scale, digital channels that connect, and programmes that build trust.

In an era where technology is reshaping financial services at unprecedented speed, the challenge is to ensure that it empowers rather than excludes. Banco Azteca’s experience shows that innovation is strongest when it combines digital transformation with inclusive product design, resilient processes and trust-building initiatives.

Purpose makes technology meaningful, turning innovation into infrastructure for equity. The most significant innovation in banking, therefore, is not measured by features alone, but by the scale of lives it brings into the financial system.