One of the oldest questions in finance is how to price options – those financial instruments which give you the right, but not the obligation, to purchase an asset in the future at a set price. For example, suppose that you think that the shares of some company, currently priced at $100, are set to go higher. Rather than purchase the shares at that price, a cheaper alternative is to buy a ‘call’ option which gives you the right to buy them at a certain price, known as the strike, in a year’s time.

Let’s say you choose a strike equal to the current price, and after a year the shares have gone up to $120, then the option allows you to buy them for $100 and sell them immediately for $120 to give a quick $20 profit per share. On the other hand if they have gone down, all you lose is the amount you paid for the option.

The problem then is, what should that option price be? And how does it change if we choose a different strike price, like $90, or $105? The answer is important, not just for individual investors, but for the financial system as a whole, which relies on the accurate pricing of this type of risk.

The nervous market

One of the first to have a theoretical stab at this problem was the French mathematician Louis Bachelier. In his 1905 thesis, he argued that the average return of stocks is zero, because they are as likely to go up as go down. The price of an option therefore depended only on the variability of the stock’s price, which he referred to as its ‘nervousness’ though today we call it the volatility. The more nervous the stock, the more expensive the option, because there is a better chance of it ending up ‘in the money.’

Bachelier’s approach had some problems and received little attention at the time, but some 60 years later the economist Paul Samuelson came across a copy and arranged for a translation. As he later told the BBC, he believed that Bachelier’s work held the key to developing “the perfect formula to evaluate and to price options.”

The Black-Scholes model met with immediate success – and helped kick off an explosive growth in options trading

In 1973, this dream formula was achieved in the form of the Black-Scholes model. Its elegant proof relied on the argument that, by constantly buying and selling options and the underlying stock, one can construct a risk-free portfolio. A consequence was that, as with Bachelier, the expected return of the stock dropped out of the equation – all that mattered for the price calculation was the risk-free rate that could be obtained on something like a Treasury bill.

The Black-Scholes model met with immediate success – and helped kick off an explosive growth in options trading. Samuelson wrote that “one of our most elegant and complex sectors of economic analysis – the modern theory of finance – is confirmed daily by millions of statistical observations.” The Nobel Prize Committee – who awarded Black and Scholes their prize in 1997 – agreed that “thousands of traders and investors now use this formula every day to value stock options in markets throughout the world.” The formula has since been described as “the most successful theory not only in finance, but in all of economics” and even as “the most widely used formula, with embedded probabilities, in human history.”

Which is odd, given that the model is actually far from being the perfect formula that Samuelson envisaged.

Is there something funny?

Part of the appeal of the Black-Scholes model was that it seemed to put option pricing onto a rational basis, by eliminating the need for subjective and uncertain estimates of future growth. This changed the perception of options trading from a form of speculation, to a form of risk management, which made it much more acceptable to people like regulators (in fact it is both).

To accomplish this feat, the Nobel-winning proof relied, as mentioned, on the idea that we can constantly buy and sell options and stocks; however this ignores the bid/ask spread, which is the difference between the seller’s ask price, and the buyer’s bid price. And it also assumes that the volatility can be treated as a constant.

There is an easy way to check these assumptions, which is to look at statistical data. First, it is clear that growth rates do matter, because if you buy call options in something that tends to go up, like the S&P 500 index, then you tend to make money. What counts is not the risk-free interest rate, as assumed by the model, but the actual growth rate.

The second problem is that volatility over a certain period is not constant, but is correlated with the price change over the same period. In fact this effect is partially captured by traders, who adjust the volatility depending on the strike price – a phenomenon known as the ‘volatility smile’ because of its parabolic shape.

Of course it’s no surprise that traditional economics, with its exaggerated emphasis on objectivity and rationality, doesn’t get the joke. So how can we improve the Black-Scholes model given these obvious drawbacks? And why are the markets smiling? We return to that in a future Econoclast.

Standing in the middle of Verkor’s headquarters in Grenoble, Olivier Dufour, the firm’s co-founder, delineates his vision for the future of Europe’s green economy. “Batteries replace oil – it is important not to move from one dependence to another,” he exclaims. Founded just three years ago, Verkor has quickly become one of Europe’s leading low-carbon battery producers. The firm recently partnered with Renault to supply the equivalent of 12 GWh of batteries annually. Through its ‘Ecole de la Batterie’ it will train up to 8,000 employees to meet the sector’s ever-growing needs.

Several EU regulatory initiatives aim to turn the bloc into a battery production leader, yet Europe needs to do much more to rediscover its industrial mojo, Dufour says: “The EU needs to reinforce its regulation to enable rapid scaling up all along the battery supply chain, from mining to recycling. It needs to use all the catalysts in its hands: financing, trade mechanisms, training, permitting and energy prices.”

Showing them the money

The race for battery supremacy is part of a broader industrial realignment, fuelled by a mix of environmental, geopolitical and trade interests. Covid brought to the spotlight the vulnerability of global just-in-time supply chains. Trade tensions have slowed globalisation down. Climate change, an emergency that requires global collaboration but local action, is increasingly seen as an opportunity for developed economies to ‘onshore’ industry.

The first shot was fired last summer when the Biden administration passed the Inflation Reduction Act (IRA), pledging to provide $369bn in tax credits, grants, subsidies and loans to boost US clean-tech manufacturing. The plan has sparked a manufacturing boom, says Jonas Nahm, an energy expert at the Johns Hopkins School of Advanced International Studies: “There are an impressive number of plant announcements, particularly in the battery and electric vehicle sector. It’s also accelerating investments in domestic solar manufacturing and other technologies supported by the bill’s tax provisions and local content requirements.”

Widely believed to be a part of the US strategy to weaken China’s dominance in the green economy, the IRA includes over $60bn dedicated to onshoring incentives (see Fig 1). Currently, around 90 percent of clean-tech manufacturing is located in Asia, with China alone accounting for 85 percent of global solar cell production. However, the bill’s domestic production requirements have irked US allies. Only firms that source parts and materials from the US or its trade partners can benefit, excluding the EU and Japan, which do not have a free trade agreement with the US. The Belgian Prime Minister Alexander De Croo has accused the US of trying to poach European investment: “They are calling firms, in a very aggressive way, to say ‘don’t invest in Europe, we have something better.’”

The makeup of the bill has been the product of a polarised political environment. Many Republicans perceive the energy transition as a nuisance that renders competition with China harder. The Biden administration passed the IRA as a ‘reconciliation bill,’ which only deals with spending and revenue, to frame decarbonisation as an economic issue. The bill has also been criticised by industrial groups, such as the National Association of Manufacturers, because of its 15 percent minimum corporate book-tax, aiming to raise revenue for subsidies and tax breaks. Many of the planned facilities are in Republican states, which could boost support for an energetic climate policy, says Nahm. But political division has affected the bill’s remit, he told World Finance. “It doesn’t include investments in many institutions, like vocational training, that would also be helpful in allowing businesses to respond to these incentives and build up a clean-tech manufacturing sector in the US.”

Many experts question whether the IRA goes far enough to tackle climate change. One flaw is that incentives are carbon intensity-based, with a focus on future clean energy and no accountability for existing emissions, says Sanjay Purswani, a senior knowledge analyst specialising in energy at the Boston Consulting Group, adding that they may not be sufficient to achieve cost parity with fossil fuels.

US President Joe Biden

Delays in the bill’s implementation may also dampen its immediate benefits. “The IRA gives the industry a long-term horizon to point to with tax credits, but is also introducing uncertainty with the delays in guidance,” says Cassidy DeLine, CEO of Linea Energy, a US power producer, adding: “You have manufacturers who are planning to build domestic manufacturing facilities, but we don’t have the guidance on what will enable equipment to actually qualify. The more stringent the requirements are, the more likely it is that fewer of the announced domestic factories actually get built.”

Potential costs have also raised concerns, given that its open-ended budget could increase demand for green subsidies. Goldman Sachs estimates that the bill could cost up to $1.2trn, but also spur over $3trn in private investments. However, researchers at the US think-tank Brookings Institution estimate that IRA incentives will be less costly than climate-related damages, while helping the US achieve emissions reductions of up to 42 percent by 2030, up to 11 percent lower than without the bill. US solar and wind power could be the cheapest in the world by 2030, courtesy of the IRA, according to Credit Suisse.

French Prime Minister Emmanuel Macron and ProLogium CEO Vincent Yang

Europe fights back

In a truly European fashion, the EU has taken its time to respond. Its post-Covid recovery fund made available €724bn to member states, a third dedicated to green projects. The French president Emmanuel Macron has been touting his vision for a ‘sovereign’ Europe leading the fourth industrial revolution.

The war in Ukraine highlighted the dangers of dependence on a single energy provider, argues Eleonore Soubeyran, an energy policy analyst at LSE. But it was the IRA that stressed the need for a new industrial policy. This March, the European Commission presented its proposal for the Net Zero Industry Act (NZIA), delineating a plan that will mobilise the bloc’s full firepower to kick-start a European clean-tech revolution. The scheme will enable member states to loosen regulatory constraints to green investment, in some cases even overriding environmental concerns.

Permits for large plants producing net-zero technologies will be granted within just one year. An example of the potential gains came this May when the Swedish start-up Northvolt announced that it will build its third battery factory in Germany instead of the US, after Berlin pledged generous state support. The plan’s goal is to raise domestic clean-tech production to 40 percent by 2030, a major increase from present levels; currently, just 10 percent of solar panels used in Europe are produced locally. “The 40 percent target lacks clarity over what more the EU could do if current measures do not deliver. This is a possible risk, given the ambitious nature of the target,” says Danae Kyriakopoulou, policy fellow at the LSE’s Grantham Research Institute on Climate Change and the Environment.

Growing anxiety in Brussels over the IRA’s impact on European industry has been the main driver behind the plan. According to one insider, it was drafted in less than a month. “It hasn’t gone through the full political cycle and the usual refining necessary to reach consensus in the EU. It’s a rushed, improvised response to the IRA, so it doesn’t amount to anything similar to it,” says Ignacio Velasco, a researcher at 3EG, a climate change think tank. To alleviate tensions, the EU and the US have a taskforce to discuss the thorniest subjects. Negotiations have already borne fruit, including US concessions on electric vehicles (EVs) and critical minerals.

Several European firms have criticised the NZIA, warning that it does not match IRA investment incentives. However, the EU’s approach is constrained by the bloc’s institutional setup. “The EU has limited fiscal capacity, because it doesn’t have a large federal budget. It can’t throw money at the problem, which is what the US has done. Only member states can do that,” says Velasco. The Commission also had to strike a balance between large and smaller economies, with the latter fearing that lax subsidy rules would allow rich countries to favour their companies. In 2022, German and French firms received nearly 80 percent of EU state aid. Forthcoming negotiations about the bloc’s Stability and Growth Pact could change that mindset. Margrethe Vestager, the well-respected competition commissioner, has suggested establishing a ‘collective European fund,’ financed with joint debt, to turbo charge green investment. However, a move towards fiscal federalism will take time, says a source that has been following EU negotiations: “That’s bigger than climate change – it’s about the nature of the EU. It will not happen overnight as a response to US policy.”

Critics also point to a protectionist focus that marks a return to the EU’s Keynesian roots, notably industrial planning. Some warn that the plan could set the green transition back by making it more expensive. “While excessively depending on one exporter is not sustainable, as we saw with Russia and gas, it does not excuse incentivising across-the-board inefficient import substitution,” says the LSE’s Kyriakopoulou.

The first carbon tariff system

Carbon taxes are also becoming a top priority of the global green agenda. Partly pushed by rising carbon prices, the European Commission laid out last December its Carbon Border Adjustment Mechanism (CBAM), effectively the world’s first carbon tariff system, to be put on trial this October. The scheme will replace the ‘free allocation’ component of the EU’s domestic emissions trading system (ETS), which helps producers bid for emission allowances. The CBAM will enable member states to tax carbon-intensive imports, including steel, iron, cement and fertilisers, with importers having to obtain emissions certificates based on EU carbon prices.

Bread and batteries

No other industry is more emblematic of the scramble for green profits than electric vehicle batteries. China currently holds 78 percent of the world’s EV battery manufacturing capacity, with Chinese battery makers CATL and BYD alone accounting for half of the global market. Both the IRA and the NZIA aim to change that.

The IRA requires at least 50 percent of battery components to be manufactured or assembled in North America, increasing to 100 percent by 2029. The plan has delivered results, with Michigan emerging as a new battery powerhouse, courtesy of Ford’s $3.5bn planned battery plant using technology from CATL and another $2.4bn battery plant being built by a subsidiary of Gotion, a Chinese firm. Tesla, Volkswagen and Norway’s Freyr Battery have also recently picked US locations to build battery factories.

In Europe, the NZIA offers regulatory incentives aiming to mitigate energy disruption and improve investment costs for battery projects. Taiwanese battery maker ProLogium has highlighted this shift in European policy as a reason for choosing France to build a €5.2bn plant.

However, many analysts are pessimistic that the programme will make a difference. “It will be very hard, probably impossible, to build something akin to the enormous, synergetic industrial ecosystem China has spent more than a decade building in the battery and EV sectors, at least when it comes to scale, and thus price,” says Nis Grünberg, a Chinese energy policy expert from the think tank MERICS.

Verkor’s Dufour, whose firm has a €1bn gigafactory in Dunkirk in the pipeline, confesses that US states have tried to lure his firm to invest in the country, offering a mix of IRA and local benefits. The EU has set a goal of achieving 90 percent battery self-supply by 2030, based on projected needs of 550 GWh, but this pales compared to US and Chinese plans, he says: “This goal is not ambitious for batteries. The industry foresees a need for 1,000 GWh by 2030, meaning that half of the batteries will have to be imported if the EU target is reached. It should be 100 percent or more, which is achievable if the EU creates the right conditions.”

Through the new system, EU policymakers hope to tackle ‘carbon leakage’ – when manufacturers relocate their production outside Europe to avoid domestic carbon taxes. Another goal is to push third countries to improve their environmental standards, creating a level playing field for European manufacturers. Critics, however, point to a lack of ambition, given that the Commission’s initial proposal was watered down by member states. “The phase-out is so slow and long that it will practically not be effective this decade, and after that it could be too late for the climate,” says Agnese Ruggiero from Carbon Market Watch, a Brussels-based environmental group.

Complexity is another challenge. The EU will need to make tough choices on which goods and sectors the CBAM will cover and grapple with technical challenges around the price adjustment methodology, taking into account other carbon pricing systems, such as that of South Korea. “Theoretically, CBAM is a better solution because it offers better environmental efficiency incentives, if designed correctly.

That’s why it hadn’t been implemented in the first place, because it is way more complex,” says Patrick Peichert from Frontier Economics, a consultancy. Loopholes may persist, notably ‘resource shuffling,’ which allows producers to shift products based on the level of each country’s environmental standards. “The result would be that countries implementing a CBAM would lose domestic market share, while global emissions would not change,” says Roberta Pierfederici, a policy analyst at the LSE’s Grantham Research Institute.

EU manufacturers have criticised the scheme for failing to cover exports, leaving them to battle global competition without any support.

One reason for this omission is to make the scheme compliant with WTO rules, which effectively require carbon tariffs to exclude export rebates and have a clear environmental focus. For many developing countries, however, the CBAM constitutes a protectionist measure that will disadvantage their exporters; many have no carbon-measuring systems in place. India is planning to challenge the system at the WTO, while other countries have begun negotiations with Brussels, requesting potential waivers. To alleviate these fears, the EU has committed to provide climate finance to developing countries.

The CBAM is even less popular with Chinese and US policymakers, who have argued that it penalises their producers. The EU has retorted that the scheme just extends rules that already apply within the bloc. “Europe is entitled to its own import rules, just like with food safety standards,” says Carbon Market Watch’s Ruggiero. One way it might gain some acceptance is the adoption of similar policies by other economic superpowers. China is expected to incorporate carbon pricing into its emission trade system, possibly even tracking the full-lifecycle carbon footprint for all traded goods, while politicians and economists have also lobbied the Biden administration to establish a US carbon tariff system.

Lithium battery Industrial Park in China

A WTO crisis

The increasing role of climate concerns in trade disputes has prompted suggestions that, like many other international organisations, the World Trade Organisation (WTO) should have a climate-orientated mandate. “There is a general recognition that WTO rules are not up to the challenge of climate change,” says Soubeyran from LSE. But the overlap of climate and national security makes that more difficult, especially after the US lost a string of cases where it tried to justify erecting trade barriers by invoking national security concerns. Disputes between the US and China on a number of issues, as well as sporadic friction with the EU, have diminished the organisation into a shadow of its former self. Its main dispute settlement mechanism has been paralysed, with the US refusing to appoint new members to the relevant appellate body.

A case in point is the IRA’s clash with WTO trade rules, notably its domestic content provisions. “From an environmental perspective, you can’t justify excluding some members and not others. That is very hard to defend at the WTO,” says a source familiar with the operation of the body. China’s commerce ministry has said that the bill possibly violates WTO rules concerning discriminatory subsidies, while South Korea is considering filing a complaint on the grounds that the law even breaches a bilateral free trade deal. For the US though, that horse has bolted, says the source: “The IRA falls into a wider pattern of US behaviour: it doesn’t care about the WTO anymore. In their internal political and legislative dialogue, it isn’t relevant anymore.”

The emergence of green industrial policies has raised concerns that the global economy is entering a phase of protectionism. Canada has warned that a subsidy race would hurt everybody. In the UK, the Labour party, which is expected to win the general election next year, has made an IRA-like £28bn green investment programme its flagship policy. Emerging economies would pay the price of a global race to the bottom, warns the LSE’s Pierfederici: “US and EU subsidies could decrease green foreign direct investment in developing economies that do not have the same capacity to subsidise their green sectors, exacerbating the North-South divide and resulting in a significant increase in demand for critical minerals, many of which are geographically concentrated in developing countries.”

All eyes are on China, the country accused of starting the protectionist race. Given its green tech lead, the Chinese government is expected to deploy a carrot-and-stick strategy to ensure its producers stay competitive. Ironically, China is getting a taste of its own medicine, but it will not back down, says Alex Wang, an expert on Chinese energy regulation who teaches at UCLA: “It may double-down on support for green industries to maintain the global supply chain dominance it has built over the last two decades. China looks to expand its clean technology business in the global South, as Chinese companies face increased resistance in the US and Europe.”

So far, its response has been meek. One reason, argues Nis Grünberg, an expert on Chinese energy policy from the think tank Mercator Institute for China Studies (MERICS), is that it already has IRA-like state aid measures in place. But a more aggressive stance should be expected, he says, as China could weaponise green tech in its disputes with the US and adopt offensive and defensive trade policy instruments such as export restrictions, localisation requirements, and foreign direct investment screening to retaliate. A first warning was given last February when Chinese authorities published a draft law suggesting that the country could impose strict export controls on solar manufacturing technology.

In search of a new balance

In April 2022, a report co-authored by the WTO, the OECD, the IMF and the World Bank warned about the dangers of climate subsidies. But with climate change already serving as a fig leaf for protectionism, the knives are out. Multilateralism is dead when it’s most needed to tackle a global emergency, while state support – ‘green’ Keynesianism – is becoming the new norm. Subsidies incentivising a switch to less efficient producers may be counterproductive, but are also reducing our addiction to fossil fuels, says the LSE’s Kyriakopoulou: “Such measures are partly correcting market failures and implicit inefficient fossil fuel subsidies that already come at a huge cost to taxpayers. The IMF has estimated that fossil fuel subsidies cost almost $6trn in 2020.”

The EU has committed to provide climate finance to developing countries

The original sin, according to Andre Sapir, an economist at the Brussels-based think tank Bruegel, may lie in the Paris Agreement: “It only defined the objectives and left the instruments to reach them unclear, letting countries choose their own policies. It was inevitable that this could create friction in industrial policy.” Currently, no forum exists to ensure international collaboration on the crucial overlap of climate and industrial policy.

Optimists argue that tensions highlight the increasing importance of the green economy, which has finally become a legitimate growth strategy. Oddly enough, protectionism might be bad for the world economy, but good for the planet, says Pierfederici: “In the long-term, competition could lead to a reduction in the cost of green tech, thus contributing to the climate goals.” For the time being, pessimism prevails. “It will get worse before it gets better. Eventually they will realise that protectionism is costly for everyone,” Sapir says. “But it will take time.”

In many ways, 2023 has been a bombshell year for activist investing. In January, US activist short-seller Hindenburg Research sent shockwaves through the business world when it accused India’s Adani Group of a “brazen stock manipulation and accounting fraud scheme” which it labelled the “biggest con in corporate history.” Hindenburg’s campaign against Adani resulted in a whopping $108bn being wiped off the company’s market value in a matter of days. Gautam Adani, the billionaire industrialist who founded the company, denies the allegations, but that didn’t stop him from plunging down Forbes’s real-time billionaires list from the world’s third-richest person to 24th, as of the time of writing.

Campaigns by activist investors, who purchase minority stakes in companies to drive strategic changes, have been on the rise since around 2017. While Adani’s fall grabbed the most headlines so far this year, plenty of other activist campaigns have rocked corporate boardrooms, from HSBC, where activist Ken Lui is calling for a break-up of the bank, to Bayer, where investor Jeff Ubben is reportedly pressuring the business to oust the CEO, to BP, where climate activists filed a resolution urging the company to set tougher emissions targets. In fact, 2022 was a record-breaking year for shareholder activism, and 2023 is expected to see similar levels of boardroom battles.

The activist landscape

The impact of activist shareholders is growing around the world. A tidal wave of campaigns, which began in the US in the age of ‘corporate raiders,’ has gained mainstream attraction in Europe and Asia. On a mission to pursue strong financial returns and strategic accountability, investors are increasingly butting up against company executives they see as underperforming.

It’s Europe that is seeing the lion’s share of new activist campaigns this year

In the first quarter of 2023, 69 new activist campaigns were started globally, which represents the second-highest quarter of activity since 2019, according to data from Lazard’s Capital Markets Advisory team. The increase in activity can be traced back to a new trend in activist investing: ‘swarming.’ This tactic is used when new campaigns are held at companies that had already been targeted by activists recently, and has affected the likes of Salesforce, Disney, Bayer and Japan’s Seven & i. In fact, 36 percent of the campaigns in the first quarter of 2023 were linked to the ‘swarming’ phenomenon, and 13 percent of targets were subject to multiple new campaigns in this quarter alone.

In 2022, activists were buoyed by tumbling markets that gave them clear sights on how companies could be pushed to improve their margins. According to the Shareholder Activism Annual Review by Insightia, 929 companies were publicly targeted by new campaigns in 2022, up six percent from 2021 and mostly driven by the US, Korea and Japan. “The outlook for activism in the US is perhaps the best in years, despite an extended run of defeats in 2022’s marquee campaigns,” the report said.

But despite this, it’s Europe that is seeing the lion’s share of new campaigns this year. According to Lazard’s data, there was a 34 percent decline in campaign activity in the US in the first quarter of the year, breaking an eight-year trend. At the same time, 21 new campaigns were started in Europe, making the first quarter of 2023 the busiest first quarter on record. European campaigns accounted for 30 percent of all global activity, though they were heavily concentrated in the UK and Germany. “What that tells us is that activist funds are looking at Europe as a new frontier,” said George Casey, global managing partner at law firm Shearman & Sterling.

In the US, Be Your Own Activist, a report by Deloitte, highlights that US activist investors have in recent years been looking toward Europe as a more attractive market. Specifically, activists have their sights set on larger companies that offer greater potential for growth and returns. What’s more, Insightia’s annual review noted that “an assertive local activism scene” in Europe was “every bit as exciting as in North America.” While Europe is expected to continue moving towards the US model of activism, which will only make it a more attractive market, there is still a difference in approach. In the US, it is common for new board seats to be won by activists through settlements, whereas in Europe, proxy contests are still popular.

“In the US, the view of both corporates and advisors has evolved over the last 15 years,” Casey said. “Very often in the past, the advice would have been to take a strong stand and fight through a proxy contest, but in the US that has evolved, and the advice now is to listen to shareholders and understand their views. If they would like to advance nominees to the board who are experienced and reputable, these days the advice is to engage and consider.”

Casey continued: “I suspect that in Europe, the trend is a little bit behind. There is still a desire to put on a strong stand. So, I would not be surprised if it arrives towards more engagement and settlements over time.”

Asia-Pacific (APAC) is another growing market for activist investing. Companies based in APAC targeted by activists accounted for 19 percent of campaigns in the first quarter of 2023. Typically, these campaigns have been “overwhelmingly concentrated” in Japan, Lazard’s report noted, but this year has seen a wider range affected, including South Korean and Australian targets. The broadening interest followed a “bumper” year for campaigns in Asia in 2022, Insightia’s report said.

The landscape for activist investors is evolving, but there is another shift taking place in the world of shareholder activism that is just as significant. While many activist campaigns are focused on improving a business from a financial standpoint, another area under increasing scrutiny is a business’s environmental, social and governance (ESG) strategy.

Bringing ESG issues to the boardroom

Broadly, there are two types of activism shareholders are pursuing: operational financial activism and ESG-related activism. The former is made up of activists targeting companies for financial returns by asking for specific operational changes, be that looking at a company’s financial performance and driving change in the way they operate or pushing the company to sell one of its lines of business.

On the other side is a trend for ESG and anti-ESG related activism that has been growing since around 2020 (see Fig 1). “While ESG as such has been increasingly important to investors, corporations and activists for over a decade, in the last four or five years in particular, many corporations have become much more socially active while others have found themselves under pressure to take public positions on environmental and social issues that they would not have previously spoken publicly about,” explained Lara Aryani, partner at Shearman & Sterling.

Indeed, issues like climate change and diversity have seen increasing public pressure, and regulatory changes that have required companies to consider them more fully. “A lot of companies felt that they needed to take a position on these issues of public importance. And so I think companies are more vocal about issues that are social or environmental in nature,” Aryani said.

While boardrooms debate where to declare their position on social and environmental issues, campaigners see shareholder activism as a new option for driving change. “The recent success of a number of ESG activist campaigns coincided with these shifting investor and corporate priorities, and this energised shareholder activism on a range of ESG issues,” Aryani said. “This was particularly the case on climate change activism, which seemed to be seeing some success in corporate action even while congressional reform on these issues seemed to have stalled.” BP faced activist demands in April to set tougher climate targets. Although the resolution was rejected by shareholders, it received more support than it had in 2022.

As ESG demands grow, anti-ESG backlash is also finding its way to the boardroom. With social and environmental issues gaining prominence, there are a growing number of individuals who believe the corporate boardroom is not the place for these discussions. Because of their ties to political issues, many of these campaigns have hit headlines despite the trend still being in its infancy.

“There has been a reaction to the growing popularity of ESG, in the form of ‘anti-ESG’ activism that is comprised of both shareholder activists and certain politicians,” Aryani said. “Though anti-ESG has received a lot of press, it is still somewhat nascent, and so people are watching to see the extent to which those efforts will impact corporate and regulatory action in a meaningful way.”

While businesses may need to take a wait-and-see approach on the anti-ESG trend, it’s important that they consider both sides of the debate when planning their approach to handling activist investors.

In the sight lines

With these two forms of shareholder activism in mind, zeroing in on the trends in both the companies being targeted and the demands being made tells us more about the state of shareholder activism today and what we can expect to see in the years to come.

In 2020, activist campaigns that were focused on mergers and acquisitions (M&A) were the most common, making up 41 percent of the total new campaigns at large companies during the period, according to Lazard’s data, which was in line with levels seen in the previous years.

However, with financial markets having taken a nosedive, Insightia’s report found that activists have “been forced to be more judicious about calls to sell the company in recent years.” Few experts believe that dealmaking will be a prominent trend this year or until markets even out. The decline of the M&A market is to blame for a decrease in the number of campaigns focused on M&A and on capital allocation, the team at law firm White & Case said in a recent report. Instead, established activists and new funds alike are pursuing more campaigns focused on ESG and corporate strategies.

While Lazard’s data backed up the trend of fewer activists calling for industry consolidation or full company sales, M&A-related demands remained popular in Europe, emerging in 57 percent of all campaigns, which was above the historical average. This was driven by a surge in calls for divestitures, the asset management firm said.

With ESG-related campaigns picking up speed, there’s a particular focus on those centred on environmental issues. The rumblings were there in 2020, with new London-based hedge fund Bluebell Capital Partners announcing a ‘One Share ESG Campaign,’ through which it would buy one share of a company in order to challenge its ESG practices. In 2022, the small activist investor took on BlackRock, the world’s largest asset manager, accusing it of greenwashing in its ESG strategy. ESG-focused activist investor Engine No.1 also found success electing three directors to the board of ExxonMobil, which received significant support from institutional investors.

Board representation remains a goal of many activist campaigns

In 2022, there was a “significant increase” in the number of environmental and social (E&S) proposals that were put to a vote, a report by Shearman & Sterling said, but this was likely influenced by a new regulation from the Securities and Exchange Commission (SEC) which made it harder for companies to exclude E&S proposals from proxy statements. While the number of proposals increased year-on-year, the number of approved E&S proposals actually fell from 38 in 2021 to 32 in 2022.

“While the decline in the number of successful E&S proposals seems incongruent with the increasing support by both activists and institutional investors for E&S initiatives, this is likely due to the fact that a significant number of proposals, particularly those relating to climate change, prescribed specific actions to be taken by the company, in contrast with the historically more successful types of proposals – E&S and otherwise – that contained more general recommendations or enhanced disclosure,” the report said.

White & Case also identified greater scrutiny of ESG campaigns as a trend to watch this year. Large institutional shareholders, including BlackRock, began to scrutinise campaigns more carefully, and their success depended largely on whether there was an economic case for them.

Beyond the ESG debate, another trend taking shape is campaigns that target large businesses. “Due in large part to activist campaigns, such as Engine No.1’s successful proxy contest against ExxonMobil in 2021 and Third Point’s successful campaign against Walt Disney in 2022, there will likely be a surge of activist campaigns targeting S&P 500 companies,” White & Case said in their report. “These campaigns have demonstrated that size alone is not a defence to a well-funded, thoughtful activist attack.” Indeed, Lazard’s data shows that this trend is well underway, with global targets with market capitalisations greater than $50bn representing 16 percent of unique companies targeted in the first quarter, the highest share on record. This trend was identified in both the US, which logged its third consecutive quarter of elevated levels of mega-cap focus, and Europe, which also saw a spike.

These strategic trends aside, which sectors are in the firing lines? Technology firms continue to be one of the most frequently targeted sectors by activists, according to White & Case, with software, services and the internet likely to be the targeted subsectors. Industrials will also be in focus, with engineering and construction machinery expected to be in activists’ sight lines.

A changing regulatory environment

Board representation remains a goal of many activist campaigns, but the majority of board seats obtained are now through settlement agreements rather than proxy contests. One reason behind this change is new regulations that are reshaping the shareholder activism landscape. In the US, activist campaigns are facing new universal proxy rules, which are expected to have a significant impact on the industry. Universal proxy rules adopted by the SEC in November 2021 will, experts predict, make it easier for activists to get one or two nominees elected to boards, though it could make it harder to elect a majority. The new rules are also expected to make proxy contests easier and more affordable, which will encourage smaller activists with fewer resources.

These changes, Insightia’s report said, “sent a jolt through the industry as advisers try to model how the greater choice available to investors will influence voting decisions.” According to data from Insightia’s Activism module, settlements have risen compared with last year since the rules came into effect in September. Lazard’s early look at the effects of the universal proxy rule found that activists have demonstrated the same apparent appetite for board changes at US companies, but there has been a “significant shift” to smaller activist slates nominated at US companies. Activists secured 43 board seats in the period from September 2022 to March 2023, 98 percent of which were through settlements.

Technology firms continue to be one of the most frequently targeted sectors by activists

As activist investing spreads around the world, flashy headlines of boardroom battles abound. But the most common advice for executives dealing with shareholder activism is to hear them out. “What often happens, which in the past people did not necessarily pay attention to, is that the activist may be raising the kind of issues that institutional shareholders may be thinking about as well,” Casey warned. “And so if the activist strikes a chord on a particular issue with the concerns that institutional shareholders have, then in a proxy contest, institutions will support the activist.”

“The number one recommendation would be to engage, to listen, understand the positions, see if there is something in what the activist is saying that actually may be useful for the company. And discuss. If you disagree, then it’s better to explain it in a way where you are engaged, as opposed to just rejecting a particular position but without explaining your own point of view,” Casey said.

As shareholder activism campaigns are seen more as an eventuality and investors are open to supporting them, it seems the new era of activism will be less about standing against activists and more about unexpected partnerships.

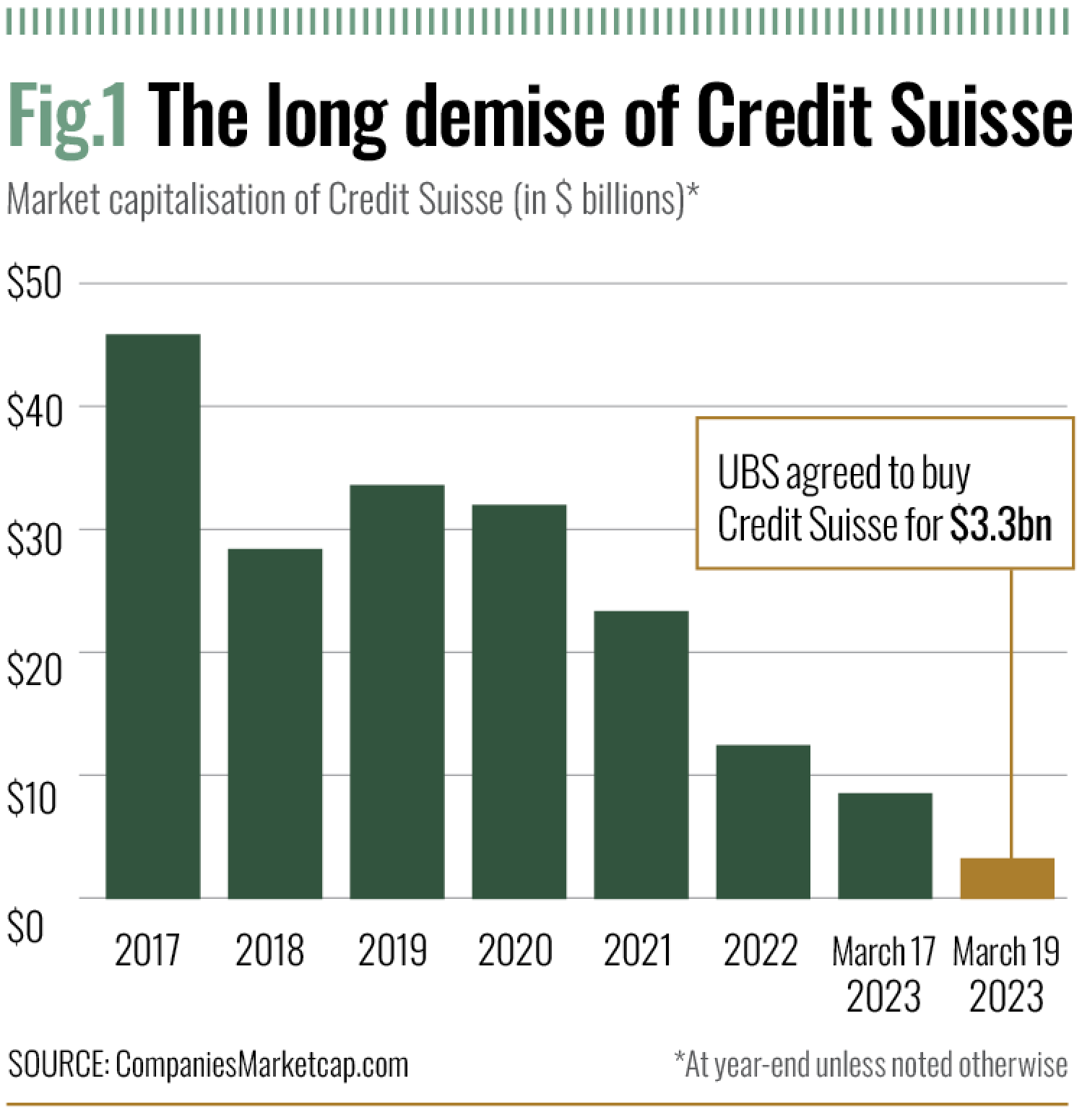

As the evidence has shown in the months since, they are not as safe as we all thought. In the bigger picture the global financial system is under stress and in some regions is in turmoil, partly because of post-Covid inflation.

“Financial stability risks have increased rapidly as the resilience of the global financial system has been tested by higher inflation and fragmentation risks,” warned the International Monetary Fund in its latest Global Financial Stability Report issued in April 2023.

Some of the most vulnerable banks are in the smaller emerging economies where debt is high and the ability to repay is in decline. But overall the IMF sees a more desperate banking environment triggered by rising geo-political risks, unsustainable levels of debt, rising inflation and interest rates, and tighter money. Meantime it was a close-run thing, far closer than anybody was prepared to admit in those fraught few days of March. As Swiss Finance Minister Karin Keller-Sutter conceded in Washington in April, the lightning-quick, forced takeover of Credit Suisse by rival UBS “had helped to avoid a national crisis.”

And that’s just in Switzerland. The president of Switzerland’s central bank, Thomas Jordan, said the takeover had prevented Credit Suisse from becoming “the first domino in a systemic crisis.”

A systemic crisis! The immediate aftermath of the collapse of Credit Suisse and SVB revealed cracks in the system that must be rapidly repaired. As the news of the problems with the two banks broke, tremors ran through the entire finance sectors of Europe, the UK and the US. There were signs of distress through much of the financial sector in America, where two others banks collapsed in a classic example of contagion.

It’s not so much the failure of one bank that worries regulators; it’s the risk of contagion. It may seem unlikely that the failure of a second-tier bank like SVB on the other side of the world would further destabilise Credit Suisse, but that’s exactly what happened. Spooked by events in Silicon Valley, more depositors pulled their funds from the Swiss giant and accelerated its demise.

Although the Swiss authorities get full marks for moving quickly and decisively, their observations are not exactly reassuring given the enormous time and effort invested in the supposed avoidance of another banking crisis like 2008. In the US ordinary depositors were so jittery that the US Fed was clearly worried about other runs. “It appeared that contagion from SVB’s failure could be far-reaching and cause damage to the broader banking system,” the Fed’s Michael Barr, vice-chairman of supervision, told the House of Representatives. “The prospect of uninsured depositors not being able to access their funds could prompt depositors to question the overall safety and soundness of US commercial banks.”

Reckless behaviour?

As we shall see, both banks somehow slipped the leash of responsible risk-averse management that regulators imposed on them in the wake of 2008 but in the meantime the inevitable question is: have the global giants returned to the reckless behaviour that precipitated the financial crisis?

Shortly after the Credit Suisse panic, French and German authorities reportedly raided five giant banks over potential money laundering and tax evasion on behalf of wealthy clients, highly illegal activities that had brought down the wrath of regulators following the post-2008 revelations of egregious behaviour.

The question has special significance because the reforms put in place over the last 15 years were supposed to render banking shocks a thing of the past. With the Bank of International Settlements in Basle drawing up the principles and details of the reforms, national regulators had ordered a whole swathe of measures that among others separated investment from deposit banking, boosted capital ratios and liquidity, sheeted home responsibility onto specific senior executives, eliminated sky-high undeserved bonuses and, above all, ensured a tottering institution could collapse without triggering a house of cards, as happened in 2008. In short, no bank could be allowed to become ‘too big to fail.’

Simultaneously, regulators subjected the giant institutions – the systemically important institutions (G-Sibs) to much closer scrutiny that was, it should be said, often resented by the bankers themselves.

Yet in spite of all this regulation 49-year-old Silicon Valley Bank failed in just 24 hours after what the US Federal Reserve described as “a devastating and unexpected run by its uninsured depositors” while once-mighty Credit Suisse was bundled into USB, its supposed rival, with indecent haste before it failed. It turned out Swiss regulators had been worried about the viability of Credit Suisse for a while. Of these failures, Credit Suisse was by far the most disturbing.

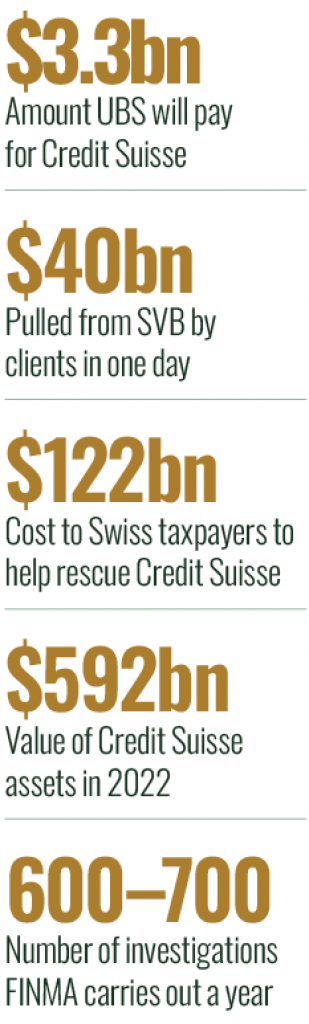

Founded in 1856 to finance Swiss railroads, it could claim 2022 revenues of nearly $17bn and assets of $592bn. It was Switzerland’s second-biggest bank and until about a year ago it had been considered impregnable. Troublesome, but still impregnable. The Swiss banking system has always prided itself on its robustness, reliability and high reputation. The main regulator FINMA is one of the most respected anywhere. Yet the Swiss government had to stump up $122bn in a hurry to underpin the rescue of Credit Suisse. That’s also against the new rules because the failure of even a G-Sib is not supposed to cost taxpayers anything.

Meantime in the US there was no question of a takeover of SVB, even at the point of a gun. The Federal Deposit Insurance Corporation, which is charged with maintaining stability and confidence in the financial system, followed the book or, as central bankers say, the ‘hierarchy.’ The FDIC quickly guaranteed all the insured deposits of SVB and Signature Bank, another federally supervised institution that went under because of a run on deposits in the wake of the general nervousness. Senior management was cleared out overnight, something the US Fed has no compunction about doing, and troubleshooting regulators moved in to sort out the mess.

Most importantly, the Fed headed off the nightmare of further runs on other banks by guaranteeing as much liquidity as they might need for up to a year. Meantime equity and other liability holders in SVB lost their investments, as the post-2008 hierarchy requires.

Speculation and repercussions

The repercussions from these failures, different though they are, are many. In the case of a genuinely global institution like Credit Suisse with activities in the US, Europe, Middle-East and elsewhere, they are of course much greater. In fact, they will run on for years. Already there is speculation about the ability of UBS, with total assets of $1.1trn and revenues of $34.6bn, to absorb its rival, partly because of the dubious nature of the latter’s assets. In theory the takeover creates an institution with $5trn in assets, but nobody is yet sure how much the assets of Credit Suisse will have to be written down.

Vice Chair of the Fed Reserve Michael Barr

The red ink is already spilling. The investments of Credit Suisse shareholders have taken a hit and FINMA will value its tier-one bonds at exactly nothing. Stockholders have taken a bath, also following the post-2008 rules to the letter. UBS will pay $3.3bn for Credit Suisse, a pittance compared with its pre-failure value.

So what happened that wasn’t supposed to happen? To take the US first, reading between the lines the US Fed was surprised by the collapse of Silicon Valley Bank. Called before the House of Representatives’ Committee on Financial Services, Supervisor Barr explained that the bank was fatally wounded because of management’s failure to handle liquidity risk, which is incidentally its biggest responsibility, and that the run did the rest. Subsequent media reports say that management was focused too much on growth rather than stability and that, when internal stress tests revealed problems, they were ignored.

But why the run and why its immediate effect? It’s clear that the Fed is confused and a little shame-faced about it all. “SVB’s failure demands a thorough review of what happened including the Federal Reserve’s oversight of the bank,” said Barr. That review should become compulsory reading in the banking world because it will be a salutary lesson.

But it is already known that SVB had a concentrated business model and that its customers were mainly involved in the technology and venture capital sector, which is potentially immensely profitable but high-risk. Although the bank had been around for more than four decades, it had grown quickly in the last few years, tripling its assets in the three years up to 2022 at a time when the tech sector was booming. That should have triggered concerns. Some of the biggest failures on both sides of the Atlantic before 2008 were institutions that had grown rapidly, like Royal Bank of Scotland.

FINMA Chair Marlene Amstad

And then the pandemic intervened. To boost yield and profits, explains the Fed, SVB invested the proceeds of fast-growing deposits in longer-term securities with better rates, but it did so without having the essential expertise: “The bank did not effectively manage the interest rate risk of those securities or develop effective interest rate risk measurement tools, models, and metrics.”

Nor did the bank manage the risks inherent in its liabilities, the other side of the coin. Here senior executives fell into the classic trap – overseeing a mismatch of liabilities and assets. Or rather, some of them did. Subsequent media reports show there were serious misgivings among some staff about their boss’s decisions. The nub of SVB’s problems was that the technology sector which it served cannot normally rely on robust operating revenues and has to keep cash deposits in the bank to meet payroll and operational expenses. But those cash deposits can also be withdrawn at will and, in fact, often are.

Belatedly SVB realised it wasn’t sufficiently liquid and, on March 8, was forced to announce that it had realised a $1.8bn loss in a sale of securities but that it planned to raise capital the following week. That was a red alert to its clients and some of the smartest people in America took a close look at their bank’s balance sheet. “They did not like what they saw,” said Barr in the kind of candid assessment that is standard practice in the US.

In an alarming example of how precarious the position of a seemingly well-funded bank can be, the clients pulled more than $40bn from SVB in just one day, on March 9. Other depositors immediately followed suit and the very next day SVB failed. Within three days SVB had gone under because of the nightmare of every regulator and banker, an unstoppable run by depositors that recalled the events of the Great Crash of the 1930s when people lined up outside the doors of thousands of institutions to withdraw their cash.

Steady deterioration

While the demise of SVB is a case of incompetent management and, as the US Fed admits in so many words, supervisory failures, the story of Credit Suisse looks very much like an inept management aided and abetted by a regulator hamstrung by politicians. FINMA issued more than 100 red flags to the bank about its various failings during its steady deterioration, although the public knew nothing about them because the regulator is not permitted to release them, unlike in the US and UK.

In a textbook example of how a munificently rewarded C-suite made one blunder after another, Credit Suisse was on the way down as early as 2021, largely because of $10bn in losses of client funds that had been invested in the massively indebted British supply chain financer, Greensill Capital, and $5.5bn invested in US hedge fund Archegos Capital Management.

Both failed in 2021 in an illustration of how interconnected the global finance sector is. Although several other lenders lost heavily in these collapses, Credit Suisse had taken the biggest plunge and suffered the most. These mistakes were “unacceptable,” confessed the bank’s former CEO Thomas Gottstein at the time. At the time of writing it was considered unlikely that Credit Suisse would recover much of its capital in Greensill and probably none in Archegos.

These catastrophes followed several years in which Credit Suisse plunged recklessly into investment banking, a notoriously fickle activity that had brought down US institutions in 2008 such as Lehman Brothers. Wealthy clients took fright at these huge write-downs and fled with their money, the share price declined and the bank’s credibility, surely any institution’s prime asset, collapsed. “The finger of blame points to the bank’s leadership,” concludes an analysis in Swiss Info, a publication of the Swiss Broadcasting Corporation.

Events rapidly took a turn for the worse. Swiss authorities moved in a new management team in October 2022 and tried to steady the ship, principally by tidying up the troublesome investment bank business. “The bank will build on its leading wealth management and Swiss Bank franchises,” it promised in a return to its roots. FINMA approved of this spring clean – “a step in the right direction towards risk reduction,” said the chairwoman of the board, Marlene Amstead, at the time.

But it was too little much too late. In the same month the bank experienced a run on client funds of unprecedented proportions even by world standards. In the fourth quarter outflows hit the gigantic sum of nearly $155bn and, although Credit Suisse managed to scrape through once again, the writing was on the wall (see Fig 1).

Going or gone

The two events have brought to the fore the issue of ‘too big to fail’ that concerns systemically important institutions. One of the most important consequences of the reforms following the financial crisis, it’s an international standard with two parts. Either the bank is a ‘going concern’ and can be somehow rescued or it’s a ‘gone concern’ and is heading for a decent burial. Adopted around the world, the standard defines a ‘going’ bank as one that has sufficient capital to cover losses from current business while a ‘gone’ bank requires it to have sufficient capital that allows it to be restructured or liquidated.

In terms of the viability of the giant, global institutions the takeover of Credit Suisse is the first real-life test of the ‘gone’ part of ‘too big to fail.’ It is a case study that has aroused intense interest around the world and there is not a single banking authority anywhere that is not following it. So far FINMA’s Amstead believes Switzerland did the right thing in what was a collective solution involving taxpayer’s money, government, regulators and central bank, and the acquiescence of UBS.

Having helped Credit Suisse ride through earlier crises, FINMA was now faced with the even more difficult issue of how to shut it down. There were four options, she explained. The bank could be allowed to fail in what is known as ‘resolution,’ a declaration of bankruptcy with what would have been interminable legal and other issues, a temporary takeover by the state that would hopefully lead to reforms and an eventual buyer, and the forced takeover that was finally adopted.

But ultimately, there’s no escaping from the fact that Credit Suisse was not allowed to fail because of the high risk that it might trigger a financial crisis. So does that mean that the entire architecture of ‘too big to fail’ will have to be rebuilt in the light of the debacle?

Regulatory failures

Regulators always have to share some of the blame in a bank failure and, to be fair, they are usually willing to acknowledge their responsibility. In the run-up to the Great Financial Crisis, for instance, the Bank of England pursued a policy of trust in management dubbed ‘regulation-lite’ that was rapidly abandoned in the ensuing carnage.

In the case of SVB, its supervision had been moved to a new team after the bank was classified as a higher-risk ‘large and foreign banking organisation,’ a category reserved for institutions with assets of $100bn–$250bn. That’s still a few steps below the most heavily supervised category of a G-Sib, but any institution with up to a quarter trillion dollars of assets must be regarded as significant.

Almost immediately the new team became worried about the competence of management and issued a rating of ‘deficient-1’ for its enterprise-wide governance and controls. As late as November 2022, supervisors sat down with the management and warned them about emerging risks, particularly in terms of interest rates and liquidity, in which lurk some of the most recognised dangers for a bank’s overall integrity. They also expressed their concerns about the impact of rising interest rates on the financial condition of SVB as well as other banks.

But the supervisors certainly did not expect it to fail, or so fast. The relationship between banks and regulators can be a tense one. While it is important to remember that most banks abide by the rules and are anxious to comply with supervisors’ recommendations, some have to be brought to judgement. In most instances of recalcitrant banks the regulators get their way because they can unleash their big weapon – enforcement through court procedures. In Switzerland, FINMA conducts an average 40 enforcement proceedings a year, most of which never see the light of day. Apart from actual enforcement, FINMA carries out 600–700 investigations a year, which require its investigators to knock on doors the equivalent of two or three times a day “to clarify possible violations,” as FINMA puts it. Faced with the evidence, in nine out of 10 cases the bank takes corrective measures, but the big problem arises when they refuse to do so, as did Credit Suisse.

As FINMA makes clear, it is rare for institutions to defy, ignore or otherwise fail to respond to investigations and multiple rulings. Thus the case of Credit Suisse has raised an issue which Swiss authorities are debating behind closed doors. Clearly, no country can tolerate an institution that rides roughshod over the regulator and here Switzerland was unusually weak. The Bank of England, US Fed and many other central bankers have more freedom to tell it like it is, for instance by naming names. “As the events surrounding Credit Suisse show, our instruments reach their limits in extreme cases,” explains Amstead, who clearly wants to be handed more powers. “It is therefore worth considering an extension.”

But of course that’s up to the politicians and they have traditionally resisted handing FINMA the authority it needs. The authority cannot even impose a fine, something that happens routinely in France, UK and the US, among other countries. As we see, Switzerland’s politicians have shot themselves in the foot. Astonishingly, even after Credit Suisse had been tied into UBS, the country’s parliament voted after a long debate that, in so many words, it was the wrong thing to do.

Fit for purpose

On the bright side lessons are being learned. The Fed is in the middle of much soul-searching about the effectiveness and power of supervisors. Essentially, in a wide-ranging internal review it is asking whether the regulatory regime is fit for purpose. “Once risks are identified, can supervisors distinguish risks that pose a material threat to a bank’s safety and soundness? Do supervisors have the tools to mitigate threats to safety and soundness?” asks Supervisor Barr, who told the House of Representatives that “the failure of SVB illustrates the need to move forward with our work to improve the resilience of the banking system.”

In short, perhaps supervisors must get tough before it’s too late. Meantime though, the US Fed wants to apply the Basel III reforms to smaller banks like SVB, the idea being they have a bigger cushion for absorbing losses rather like the G-Sibs. And in another move that will be closely watched by the entire financial sector, the Fed plans a whole new panoply of stress tests that capture a much wider range of risks and uncovers channels for contagion. In itself, that is an admission that the current stress-testing technologies just don’t cut it.

The fear about contagion is that it is often irrational – in the modern banking system insured depositors get their money out – but fear spreads without reason. One little-known weakness in the post-2008 global banking system is the rise of fintech, the upstart sector that is determined to eat the big boys’ lunch. Nimbler, cheaper and often more customer-friendly, they have weakened the giants’ hold on the financial landscape. One result is that there are fewer banks in the US, to take just one jurisdiction. As US Fed governor Michelle Bowman explained recently, “de novo [new] bank formation has essentially stagnated for the past decade during a time when financial services have rapidly evolved.”

This matters because new banks are by definition smaller, more conservative and, surprisingly, often safer. The smallest banks often sail through a crisis while their bigger rivals struggle, explains Governor Bowman: “As we have seen over time, they often outperform larger banks during periods of stress like the pandemic and during the 2008 financial crisis.”

Also, they look after their customers better, notably small business, during hard times. If nothing else, that may precipitate a flight by depositors away from the giants. Looking ahead, current levels of bank capital probably won’t be seen as sufficient. They certainly weren’t in the run-up to the Great Financial Crisis, as regulators acknowledge, and the latest scare is prompting a rethink.

The consequences of inadequately capitalised banks run deep. For instance, the 2008 crisis with its banking failures triggered the deepest and longest recession since the Great Depression of the 1930s. In America, the world’s wealthiest – and most banked – country, employment collapsed and took six years to recover; six million individuals and families lost their homes to foreclosures; and over 10 million people fell into poverty. The effects are still being felt today, as the research shows.

Although the return of the much-feared run on deposits is causing central banks concerns, on the bright side nobody is saying that the global banking sector is about to implode. “We’re in a very different place and I really don’t see this as the beginnings of a systemic financial crisis,” Bank of England governor Andrew Bailey said in a post-Credit Suisse debate.

No central banker would of course ever say anything different, but there’s no doubt that the tremors caused by the collapse of SVB and Credit Suisse have exposed cracks in the system that must now be repaired.

Taking to the stage at the Chinese Communist Party Congress in October 2022, President Xi Jinping was met by rapturous applause. The week-long event ushered in a new era for both Xi and for China, handing the veteran politician a further five years as head of the ruling party. With the removal of the two-term limit on presidency, Xi is set to become modern China’s longest-serving leader – and the nation’s most powerful ruler of the post-Mao age.

While Xi has tightened his grip on power, he now faces myriad challenges as he moves into his second decade in charge. After years of almost unfathomable economic growth, China is showing signs of a slowdown. The pandemic has left deep scars on the world’s second-largest economy. Strict ‘zero-Covid’ lockdowns have wreaked havoc on every aspect of business in China over the past three years, and in 2022, the Chinese economy grew at the slowest rate in three decades, falling behind the rest of Asia for the first time since the early 1990s. Despite rallying somewhat following the abrupt end to ‘zero-Covid,’ the nation’s nascent economic recovery remains uneven and uncertain.

Elsewhere, geopolitical tensions with the West, skyrocketing youth unemployment and an ongoing housing market slump all pose a problem for China in the near term. But the nation also faces significant long-term threats to its economic health. Its population is ageing rapidly, with 400 million people expected to be aged over 60 by 2035. What’s more, China is thought to be one of the countries most exposed to climate change, with rising sea levels, extreme flooding and food insecurity among the challenges caused by a warming climate. And, all the while, an increasingly insular political regime threatens to derail the country’s global economic ambitions.

The days of double-digit growth may well be over. It’s clear that the Chinese economy stands at something of a crossroads, with a host of challenges looming large on the horizon. Will Xi’s China be able to adapt and overcome – or is this 21st-century success story now one for the history books?

The great slowdown

Since coming to power in 2013, President Xi has overseen immense economic growth. Average income has doubled since 2012, and GDP has grown by over 100 percent in the same timeframe. For many, living standards have significantly improved, with the President declaring “complete victory” in eradicating absolute poverty among his 1.4 billion Chinese citizens.

Semiconductor prohibitions suggest a significant escalation in the Sino-US tech arms race

Impressive results, certainly. But now China finds itself butting up against that age-old developmental issue – how to sustain growth in the long term. Double-digit growth can’t be maintained forever, and China’s rapid rise is now steadily slowing. Since the turn of the century, the nation’s growth rate has been roughly halving every decade, falling to just three percent in 2022 as ‘zero-Covid’ took its toll on the economy. While by no means catastrophic, this represented the Chinese economy’s weakest performance since 1976 – the last year of President Mao Zedong’s rule.

However, despite some gloomy economic forecasts, the nation managed to defy expectations and show some early signs of recovery in the first quarter of this year. According to China’s National Bureau of Statistics, the economy grew by 4.5 percent in the first three months of 2023, boosted largely by an unexpected rise in retail sales. If it can maintain this momentum, the country may well be on track to exceed its own modest growth target of five percent for 2023. But a rapid recovery is by no means guaranteed. As countries around the globe grapple with their own economic woes, the demand for exports remains subdued – which is bad news for the ‘world’s factory,’ as China is commonly dubbed (see Fig 1).

Output from the nation’s factories continues to miss forecasts, and other Asian nations including Vietnam, Malaysia and Bangladesh are beginning to snap at China’s heels in the manufacturing and export markets.

Elsewhere, the ongoing property market crisis continues to weigh down the Chinese economy. Commentators have called it a ‘slow-motion financial crisis,’ with economists drawing gloomy comparisons with the Lehman Brothers scandal. The once-booming property sector has been hit by a liquidity crisis. An ever-growing number of real estate companies are beginning to struggle with their enormous debt piles and are defaulting on repayments, with property firms putting the brakes on their construction plans as they look to manage their troubled finances. As apartments in China are typically sold ‘off-plan,’ or before completion, property developers are failing to build homes that have already been purchased.

Across China, thousands of unfinished homes sit vacant and unoccupied, while disgruntled homebuyers refuse to pay their mortgages on apartments that were never completed. Despite recent attempts by Beijing to prop up the ailing sector, the housing market remains a weak spot in the Chinese economy, with house prices and sales stuck in a prolonged slump. This is a far-reaching crisis with no quick fix, and without government intervention, threatens to drag the economy down at a time when it needs to be firing up.

Youth discontent

There is little doubt that the impact of China’s ‘zero-Covid’ lockdowns has been disproportionately felt by the nation’s youth. Layoffs, hiring freezes and a widespread jobs drought have combined to create a jobs crisis for young people, with one in five Chinese youths now classed as unemployed.

China has become increasingly isolated on the international stage

While the pandemic has pushed youth unemployment to near record highs, it is certainly not the cause of China’s graduate woes. Before the arrival of Covid-19, joblessness among young Chinese people hovered around 13 percent in urban areas – already high when compared with other international cities. Despite recent shifts towards establishing a consumption and service-driven economy, manufacturing remains essential to Chinese growth. Indeed, the manufacturing sector has the highest shortage of workers of all industries in China – and yet these physically demanding manual jobs are unlikely to appeal to the 10.76 million university graduates that finished their studies last year.

To make matters worse, the job opportunities that Chinese graduates have begun to depend on – in the thriving and well-established tech sector, for example – have been badly hit by a new wave of government scrutiny. In late 2020, the Chinese government launched a regulatory crackdown on big tech, wiping off more than $1trn in value from some of the country’s biggest companies. Concerned that some of the nation’s businesses were simply becoming too powerful, the government looked to rein in private enterprise through a series of stringent regulations – taking aim at the tech giants first and foremost.

Under this enhanced government scrutiny, many of China’s best-known tech companies have undergone a radical restructuring and downsizing since 2020, making mass layoffs along the way. Online retailer Alibaba, social media site Weibo and entertainment giant Tencent were among the tech firms making job cuts in 2022, contributing to a large-scale jobs crisis in one of China’s most promising sectors.

Corporate crackdown

Tech isn’t the only sector haemorrhaging jobs, however. The government’s clampdown on big business has targeted a range of powerful industries, from real estate to the $150bn private tutoring industry. In the summer of 2021, China’s State Council officially banned all for-profit tutoring companies from teaching core curriculum subjects, including Maths, English and Chinese. It also banned all private firms from offering after-school studies, as well as weekend and holiday classes, and demanded that all existing tutoring companies register as non-profits. This sudden, severe curtailing of the private tutoring sector was intended to reduce the financial burden on parents and academic pressures on children – many of whom have been attending additional classes since preschool age.

Whether the measures will succeed in reshaping China’s famously competitive education system remains to be seen – but the impact on jobs is undeniable. Tutoring opportunities began to dry up dramatically in the wake of the crackdown, with education industry job postings dropping 49 percent in Beijing in the month following the move. Up to three million tutoring positions may be affected by the new policy, aggravating the race for jobs among young, educated university leavers.

And it’s a similar story in the beleaguered real estate industry. In an attempt to curb excessive borrowing by property developers, the government has piled on regulatory pressure. New restrictions on debt growth and borrowing have sought to bring the troubled industry back under control – and have toppled a number of struggling property firms along the way.

Evergrande Group, China’s second largest property developer, only narrowly avoided collapse after the government stepped in to help restructure its colossal $300bn debt pile. But others haven’t been quite so lucky. Losses and layoffs have been inevitable as firms grapple with their dire finances. One company, based in the south-western city of Chengdu, was reportedly forced to lay off 90 percent of its workforce in 2021, while the largest property developer in Henan province has also cut 7,000 of its staff. Despite Beijing’s recent efforts to ease the liquidity crisis, these interventions won’t be enough to save every firm from going under. And fewer firms mean fewer opportunities for graduates entering the jobs market – and certainly won’t help to bring down China’s stubborn youth unemployment rate.

Frosty relations

Domestic issues aren’t the only thing holding back China’s economy. Beijing’s relationship with the West has soured in recent years, with human rights concerns, differing approaches to Covid-19 and a growing Sino-Russian alliance all contributing to a widening ideological gap between China and the rest of the world.

Indeed, aside from its partnership with Russia, China has become increasingly isolated on the international stage. Upon his reappointment as head of the Chinese Communist Party, President Xi Jinping took an unambiguous swipe at the West in a speech made to delegates at the ruling party’s annual congress.

“Western countries led by the United States have implemented all-round containment, encirclement and suppression of China, which has brought unprecedented severe challenges to our country’s development,” the Chinese leader is reported to have said. The comments have done little to ease the tensions between Beijing and Washington, which have been steadily worsening since the Trump-era trade war that was launched in 2018.

While President Joe Biden has taken a somewhat softer stance on China than his predecessor, tensions between the two nations remain fraught. Now in its fifth year, the trade war between the US and China shows little sign of abating, with President Biden imposing fresh restrictions on US exports to China – specifically on the sale of US-made semiconductors. Given China’s dependency on foreign microchips – spending more on semiconductor imports each year than it does on oil – the stringent restrictions threaten to throttle China’s thriving microchip sector. Although President Biden has stressed that he seeks “competition, not conflict” with China, the sweeping semiconductor prohibitions suggest a significant escalation in the Sino-US tech arms race.

In Europe, meanwhile, relations remain equally strained. China’s continued support for Russia throughout the ongoing war in Ukraine has undoubtedly damaged its diplomatic ties with the EU. At a recent speech in Brussels, the president of the European Commission, Ursula von der Leyen, stressed that Europe needed to urgently reassess its relations with China, in light of the nation’s “policies of disinformation and economic and trade coercion.”

Despite the decidedly frosty atmosphere between the two sides, however, neither can risk any damage to their trade relationship. Trade between China and the EU is worth an extraordinary $1.9bn per day, with the continent increasingly reliant on China for the critical raw materials it requires for its green transition. As Von der Leyen noted in her speech at Brussels, it is simply not in Europe’s economic interest to “decouple” from China, but it may need to “de-risk” its trade with the superpower in future.

“Our relationship is unbalanced and increasingly affected by distortions created by China’s state capitalist system,” the EU chief said. “We need to rebalance this relationship on the basis of transparency, predictability and reciprocity.”

Diplomatic ties between the two sides are most certainly frayed, with little indication of a rapprochement. Unless it can urgently repair its relations with the EU, Beijing may find itself distinctly isolated on the world stage.

The grey wave

From strained international relations to a looming youth unemployment crisis, China is grappling with a number of threats to its economic health in the near term. But look to the long term, however, and it is clear that the nation faces far greater challenges in the decades to come.