Harvesting fast economic growth, the GCC region has emerged from vast oil and gas wealth, and years of unspent surplus income. In the last decade the GCC nations have developed, with these rich economies adopting similar structures to the west. These economies are dominated by Sovereign Wealth Funds (SWF) that account for approximately 32.6 percent of the global SWF assets, valued at $6trn. According to the SWF Institute, among the GCC states Saudi Arabia’s Monetary Agency (SAMA) holds the prime position in the volume of assets, with an estimated $675.9bn.

This is followed by the UAE’s Abu Dhabi Investment Authority at $627bn; and subsequently Kuwait’s Investment Authority at $386bn; Qatar’s Investment Authority at $115bn; Bahrain’s Mumtalakat Holding at $11bn; and Oman’s State General Reserve Fund at $8.2bn. It is not surprising that the origins of these funds emanate from oil and gas revenues, and four of the funds are all ranked within the global top 10 by country.

Dream results made a reality

It has been widely reported that both the SWF of Abu Dhabi and Kuwait had made sizeable profits of $30m from their acquirement of shares in the UK’s Royal Mail, after the shares surpassed the issuance price by up to 40 percent in October 2013. The Abu Dhabi Investment Authority (ADIA) and Kuwait Investment Authority (KIA), invested $79m each, giving an immediate return on investment. This is considered an investors’ dream.

It has been widely reported that both the SWF of Abu Dhabi and Kuwait had made sizeable profits of $30m from their acquirement of shares in the UK’s Royal Mail

However, change is on the horizon. The recent instability in western markets, including the downfall in the euro and the US Government Shutdown, have resulted in the GCC shifting its focus of SWF spending to local markets. KPMG reported that this redirection of sovereign wealth would benefit local infrastructure ambitions and accelerate growth and development of local economies. The GCC has initiated mammoth infrastructure development, and it is estimated that by 2020 spending will surpass $142bn on projects in rail, road, sewage and bridge development.

Not only have certain western downfalls contributed to local SWF investment, but the Arab Spring had a very positive impact on three GCC states, as an influx of both local and foreign investors pulled away from affected territories and redirected their investment into other neighbouring states – in particular the UAE, Qatar and Saudi Arabia. This has resulted in property cash buyers in cities such as Dubai creating a rise in property prices, which in turn has resulted in mixed reactions over whether another property boom is imminent or avoidable.

Investing to recoup

Despite speculation that office vacancy rates in Dubai are above 40 percent, Dubai International Financial Centre (DIFC) made headlines as it announced a further AED15bn in expansion over the next 10 years. The attraction of tax free wholly owned entities and being an independent jurisdiction with DIFC laws and regulations written in English and defaulting to English law in the event of ambiguity are all key sellers.

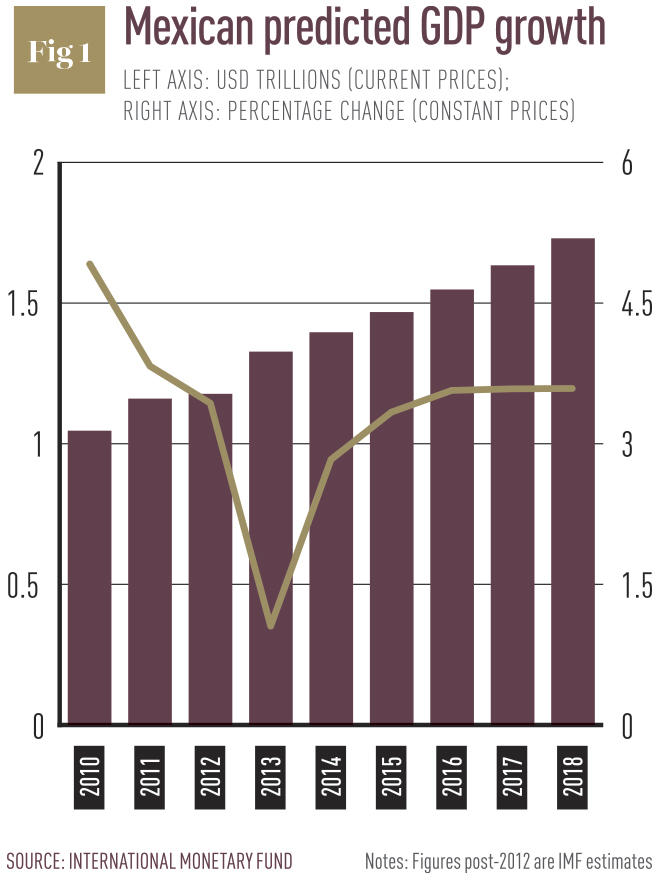

Standard Chartered Bank is one of many to be based in the DIFC area as it moved into a purpose built $140m building. Looking onwards we can expect to see the GCC develop its domestic growth and increase income. Saudi Arabia remains in pole position as the largest Arab exporter, having exported goods and services in the region of $410bn in 2012, accounting for 28 percent of the international total Arab Exports (see Fig. 1).

However, the banking sector raises concerns in regards to short-term stability, as one major issue is the absence of regulated credit agencies. For the last decade both international and local banks have been lending aggressively to consumers without any credit history data.

The UAE proposes to introduce the first credit bureau agent – known as Al Etihad Credit Bureau – by 2015. The UAE Central Bank has been actively working with top banking industry representatives, led by the UAE Banking Federation (UBF) to execute this project.

Once fully operational, it is predicted lending may be at a standstill for up to 12 months, as the banks will be gathering data on the borrowers and their repayment habits. Consumers acquiring up to four credit cards from different lenders, and the absence of credit checks, has historically fuelled a debt driven society.

The use of Post Dated cheques has also caused more moral harm to the economies. Central Banks in the GCC are all actively working to overcome these hurdles. As their economies grow, naturally the banking system requires increased sophistication, however, the west has not given a positive model in regards to banking practices and ethics.

The use of Post Dated cheques has also caused more moral harm to the economies

The rise in domestic lending in Saudi Arabia has been evident in the last few years. In both the first and second quarter of 2012 it added $22.78bn in credit, compared to the whole of 2011, which saw $23.96bn. The local banks have immensely benefited from a retail-spending spree. According to SAMA data, an average of $14.39bn was withdrawn from Saudi ATM’s on a monthly basis over the summer of 2012. The government is determined to heavily develop infrastructure and housing projects.

This will create a national boom for the local financial services sector and the banks will exhibit steady growth in the coming years. With this opportunity, Farazad Investments has the ability to attract institutional lenders to invest into these safe haven economies, as the risk of default is minimal as consumer demand is high.

The UAE has experienced an over saturated banking industry, as more than 50 local and international banks compete in being the best in retail commercial and investment banking to a population of only eight million.

This has impacted negatively on international banks that have cut losses and retreated. In September, Barclays announced plans to sell its retail bank operation in the UAE, as foreign banks cannot compete against cash rich local rivals. The exit of such high profile banks are attractive to local ones, as they are able to increase their retail portfolio – Barclays is not the first UK bank to fall victim. In 2010 the Royal Bank of Scotland retail operations was bought by Abu Dhabi Commercial Bank in a $100m deal. Not only are local lenders on the lookout for buyouts, but international banks such as HSBC Holdings bought Lloyds Banking Group’s onshore retail, corporate and commercial banking operations in the UAE.

Making sacrifices for longevity

Banking worldwide has witnessed bleak times as further job cuts were announced. Unfortunately, these job losses have resulted in major players in Dubai such as Nomura, Deutsche Bank, Credit Suisse and UBS making labour cuts locally. Interestingly, Credit Suisse relocated some of its labour to Qatar, with UBS moving its regional investment banking headquarters to Doha. Morgan Stanley has also moved part of its equities business to Saudi Arabia.

Approximately $3bn of securities were affected in July this year, when Moody’s downgraded 12 GCC banks. The downgrade was necessary to capture the evolving risk of subordinated debt. Within the next few years Basel III will be implemented in all GCC States, and subordinated debt instruments expect to have mandatory loss-absorbing features, triggered by the provision of government support. Moody’s however has noted the government’s in the Gulf have unrivalled support for local banks – in particular State owned – compared to the West, which is not fully supported. In our experience, the best mechanism to provide maximum protection is to combine both subordinated and un-subordinated debt by cushioning the risk rating in the event of a default.

Farazad Investments has introduced a unique in-house formula, which internationally recognised Institutions are in the process of adopting. This formula evolves how traditional funding has been done in the past.

Farazad Investments has introduced a unique in-house formula, which internationally recognised Institutions are in the process of adopting

The possibility of sanctions being lifted on Iran will gravely impact GCC States as oil and gas revenues will deplete. The GCC has profited from the trade embargos on Iran, however, once the veil is lifted it’s every oil state for themselves.

Iran boasts the original location where oil was first discovered in the Middle East, which is now over 100 years old. The Islamic Republic is also the second largest oil producer in the world, and ranked first for largest proven natural gas reserves, with Qatar ranked in third. The UN Conference on Trade and Development (UNCTAD) reported that despite sanctions imposed on Iran, foreign direct investment (FDI) in 2010 exceeded $3.6bn and in 2011 made a new record high of surpassing $4.15bn. The Economist Intelligence Unit (EIU) estimated net FDI would rise by 100 percent by 2014, bearing sanctions in mind. As of 2012, over 400 foreign companies have been reported to have invested in Iran.

These investors include developed nations such as Russia, the UK, Germany, France, South Korea, Norway and even companies from the US – both Pepsi Cola and Coca-Cola have joint ventures with Iranian companies. The UNCTAD positioned Iran in 2010 as the sixth global country to attract foreign investment. Iran has a vision, and by 2025 it aims to attract $1.3trn of foreign investment into the country. Should sanctions be lifted, this vision may become a reality, and Iran’s neighbours will feel the impact.

Many Iranians who have heavily invested in the GCC region have experienced resident visa issues and so those within the GCC States would gladly reinvest back into their motherland. The market in the Middle East in the next few years will undergo a drastic reform – some nations will rise and others may fall. I envisage Saudi Arabia, Qatar and Iran will be among the victors. The change in regime will fuel this positive development and the younger generation will ascend.

For further information email enquiry@farazadinvest.com