Top 5

Jamaica, a vibrant and culturally diverse Caribbean country, is known for its reggae music, stunning white sand beaches and warm hospitality. However, beneath the surface of this paradise exists a significant issue that is seemingly going unnoticed: low economic protection for people over 65 years old.

Research in 2022 by the International Labour Organisation (ILO) Regional Office for Latin America and the Caribbean uncovered that more than a third of retirees face a grim reality. The ILO report, Overview of Social Protection in Latin America and the Caribbean states, “The proportion of older people without labour income or pension increased from 31.9 percent in 2019 to 34.6 percent in 2020 and 34.5 percent in 2021. This coverage gap is the highest since 2012.”

This alarming statistic represents a disturbing trend and is further exacerbated by the economic challenges Jamaicans currently face coupled with the traditionally limited access to socio-economic protection nets over the years.

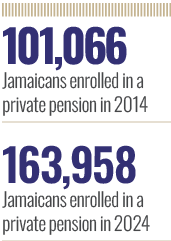

According to the Private Pension Industry Quarterly Statistics published by the Financial Services Commission (FSC) in 2014, Jamaicans enrolled in a private pension arrangement totalled 101,066. Ten years later, the total enrolments stood at 163,958 – a 62 percent increase in enrolments over the period. When one considers that the total working population in Jamaica is approximately 1.3 million, it means that only 12.4 percent of adult Jamaicans have a pension plan. This low adoption is an ominous indicator of Jamaica’s socio-economic well-being.

This reality begs the question, what are the systemic barriers to the broader adoption of pension saving in Jamaica? How can institutions with the ability and capacity work to shift this deep-seated and concerning reality so that there can be more involvement in retirement planning? As part of NCB Financial Group, Jamaica’s largest financial institution (by asset base), NCB Insurance Agency and Fund Managers (NCBIA) plays a vital role in the nation’s financial landscape. This position gives NCBIA unique insight into the economic challenges Jamaicans face. The company is cognisant of some of the nuances that shape the financial behaviour of Jamaicans across savings, investments, insurance, payments, and pensions. From our vantage point in the industry, many of the barriers have been cultural and economic in nature and are at the heart of the slow adoption of pension schemes. Institutions must therefore work intentionally to change this reality as quickly as possible.

Cultural significance of family structure

Jamaicans place a high value on the extended family, where children often provide financial support to their parents in their old age. This cultural norm has been deeply ingrained for generations and has played a significant role in the deprioritising of investments in formal pension schemes. Many Jamaicans believe their children will care for them in their old age, making them less inclined to save for retirement.

While that reality might have held true in times past, many millennials and younger generations now face significant financial obligations of their own such as student loan debt, the cost of housing (either rent or mortgage), and the cost of their own living expenses. This situation creates a conundrum for the older parent and the young adult. In most cases, both prioritise immediate needs over future savings, leaving pension planning as another ‘nice-to-do’ activity.

Reliance on informal economy

Jamaica’s economy has a substantial segment of workers in roles like hairdressing, barbering, vending, carpentry, masonry, plumbing, small-scale agriculture and other independent or casual labour. Participants in this informal economy oftentimes do not participate in formal pension schemes. The reality is that, traditionally, access to such schemes was non-existent outside of being formally employed, leaving individuals to fend for themselves when saving for retirement. This is seen in the behaviour of the Jamaican populace, who rely on less formal financial structures such as ‘throwing a partner’ – a collective non-interest-bearing saving activity.

The reliance on informal ways to save for one’s retirement is further magnified by the fact that, historically, access to a pension scheme was limited to those Jamaicans who were employed by an institution that positioned pensions as an employment benefit. Given this positioning, and despite the advent of approved private retirement schemes, where people in the informal section can set up and benefit from a formal pension arrangement, individuals have still viewed formal pension plans as an option that is either too complicated to understand or something meant for blue-collar employed people or wealthier individuals.

Mistrust of financial institutions

A general mistrust of financial institutions is another cultural barrier to pensions in Jamaica. This distrust is fuelled by various historical and socio-economic factors. The infamous financial meltdown in the 1990s, which resulted in significant losses for investors, left a lasting impression on many Jamaicans. The mistrust has been further magnified by recent and repeated incidents of fraud in the financial sector. Unfortunately, this mistrust has carried over to formal pension planning, as people harbour scepticism about entrusting their hard-earned retirement savings to these institutions. With the deep-seated barriers to wider adoption of pension planning in Jamaica, institutions such as NCB Insurance Agency and Fund Managers have had to implement strategies aimed at making it easier to access pension funds and serve as advocates for the average Jamaican as they seek wider participation in this aspect of financial planning.

Education and awareness

The first step in overcoming cultural barriers is to continue to educate the population about the importance of pensions and long-term financial planning. Public awareness campaigns, workshops, and seminars can help dispel myths and misconceptions about pensions and build trust in the formal financial sector. NCBIA has recently launched a robust public education campaign to help position pension planning as a critical component of one wealth preservation plan. The ‘Retire like a Boss’ initiative seeks to go to the hearts and minds of members of the informal economy, by tapping into their inherent nature to survive in their current lives and using that appeal to encourage them to also thrive after retirement.

This low adoption is an ominous indicator of Jamaica’s socio-economic well-being

Similarly, increased awareness needs to be had around the performance of pension funds and how this augurs well for investors and recipients of pensions. Oftentimes, news of financial and economic challenges highlights the negative performance of invested pension funds.

As the players in the industry advocate for increased participation among Jamaicans, more should be said to highlight the positive performances of said funds. In this vein, NCBIA is proud to boast an enviable performance of its pension funds, delivering a 10-year average composite yield of 11.4 percent as of the end of 2023.

Cultural sensitivity

Policymakers and financial institutions should be culturally sensitive in their approach to promoting pensions. By understanding the strong family bonds in Jamaica, they can emphasise how pension savings can complement, rather than replace, family support in retirement. Similarly, understanding and engaging the new workforce will require financial institutions to rethink how pension planning is positioned. The imagery of the ‘rich old person’ on a beach somewhere, while the desired reality, has not been the experienced reality of many millennials and Gen Zs and their retired parents. As such, creating a vision of the ‘real’ future has to be reimagined by players in the industry and reflected in their efforts to increase the take up of private pension plans.

Ease of access

Pension providers must provide online platforms to allow tech-savvy millennials and Gen Z access to these services without needing to visit a physical location. In addition, customers who engage with financial institutions at physical locations should be introduced to pension planning at all points of onboarding or servicing, given the positive impact a pension arrangement will have on their financial futures. NCBIA is proud to be one of the forerunners in Jamaica in providing a fully digital application process for its clients. Our NCB pensions portal allows clients to select the funds they want their savings to be invested in and select how their savings should be allocated across different funds. Once enrolled, clients can also track their pension fund performance via the portal. Solutions such as this should see a shift in the number of active pension plans in the society sooner rather than later.

The government

Finally, the role of government in creating an enabling environment for pension planning is imperative. In Jamaica, significant work has to be done to make the industry more amenable to modern realities. However, given the threat to the socio-economic fabric of society brought on by a financially unstable and ageing society, it is imperative that the government seriously considers making pension participation mandatory for all persons earning an income in Jamaica. This is a necessary step in rapidly improving the retirement fortunes of hundreds of thousands of Jamaicans. Organisations such as the Pensions Industry Association of Jamaica, of which NCBIA is a part, continue to lobby for the adoption of automatic pension enrolments, and this forms a key pillar in our advocacy strategy for the well-being of Jamaicans. In fact, the Jamaican government has already taken positive steps through the creation of the Tourism Workers Pension Scheme, which is a positive step in the right direction. NCBIA is of the view that this approach, applied nationally, will usher in a better day for so many hard-working Jamaicans.

In conclusion, Jamaica’s cultural and economic barriers to pension planning adoption are deeply rooted and multifaceted, making them challenging to address. However, with the right mix of education, innovation, and government support, these barriers are gradually being overcome. Pensions are not just for the office worker, the well-to-do, or the sophisticated investor. Living one’s best life after retirement should be an expectation for all Jamaicans, and this is the mantra that continues to drive us at NCBIA as we play our part in building a better Jamaica.